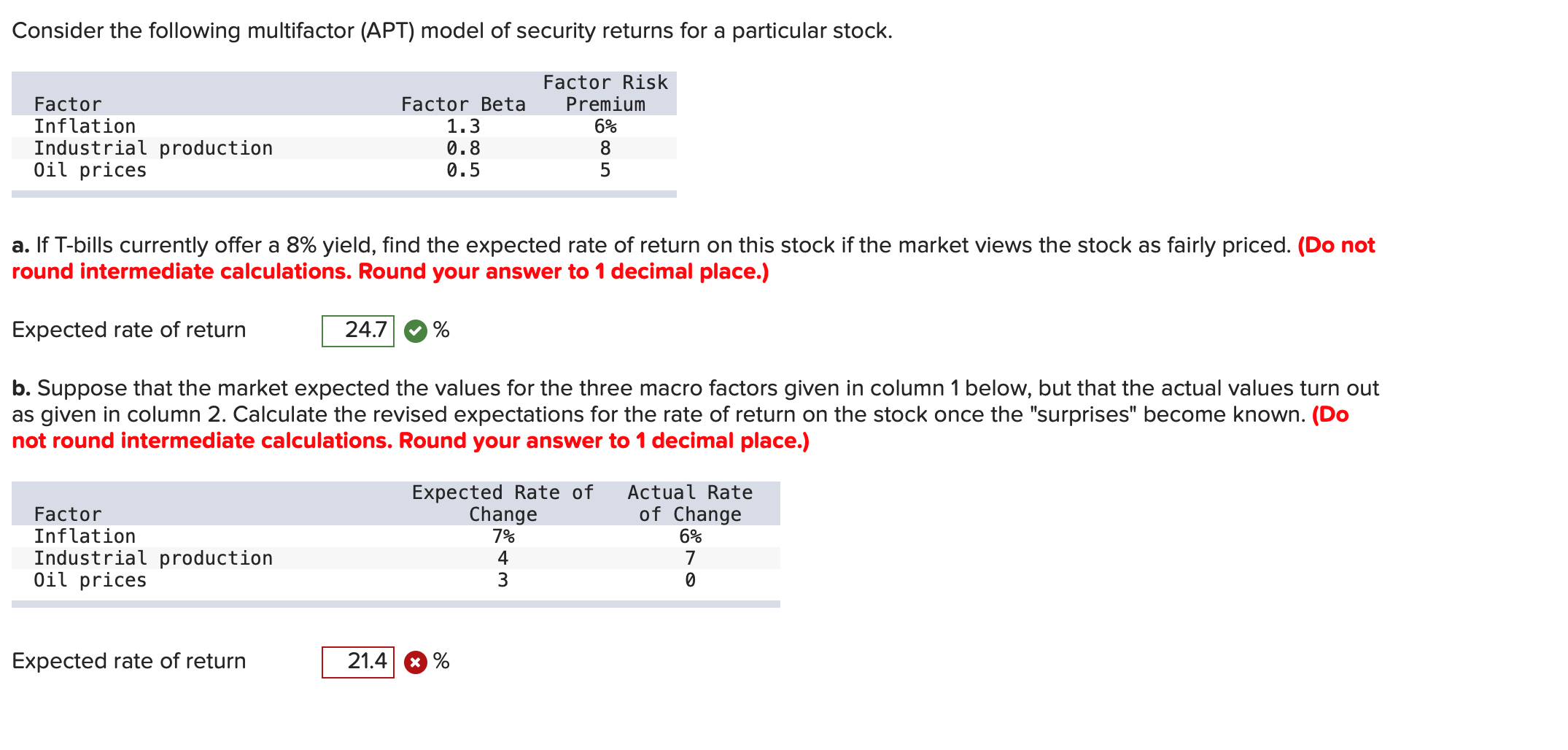

Question: Consider the following multifactor (APT) model of security returns for a particular stock. Facto r Risk Factor Factor Beta Premium Inflation 1.3 696 Industrial production

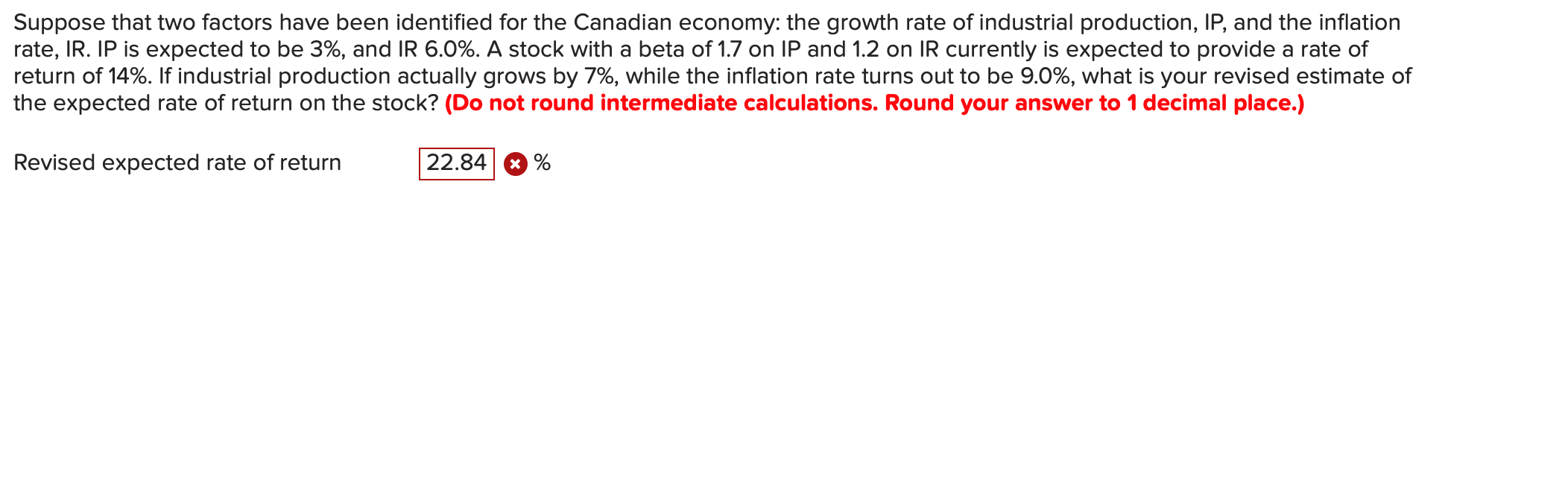

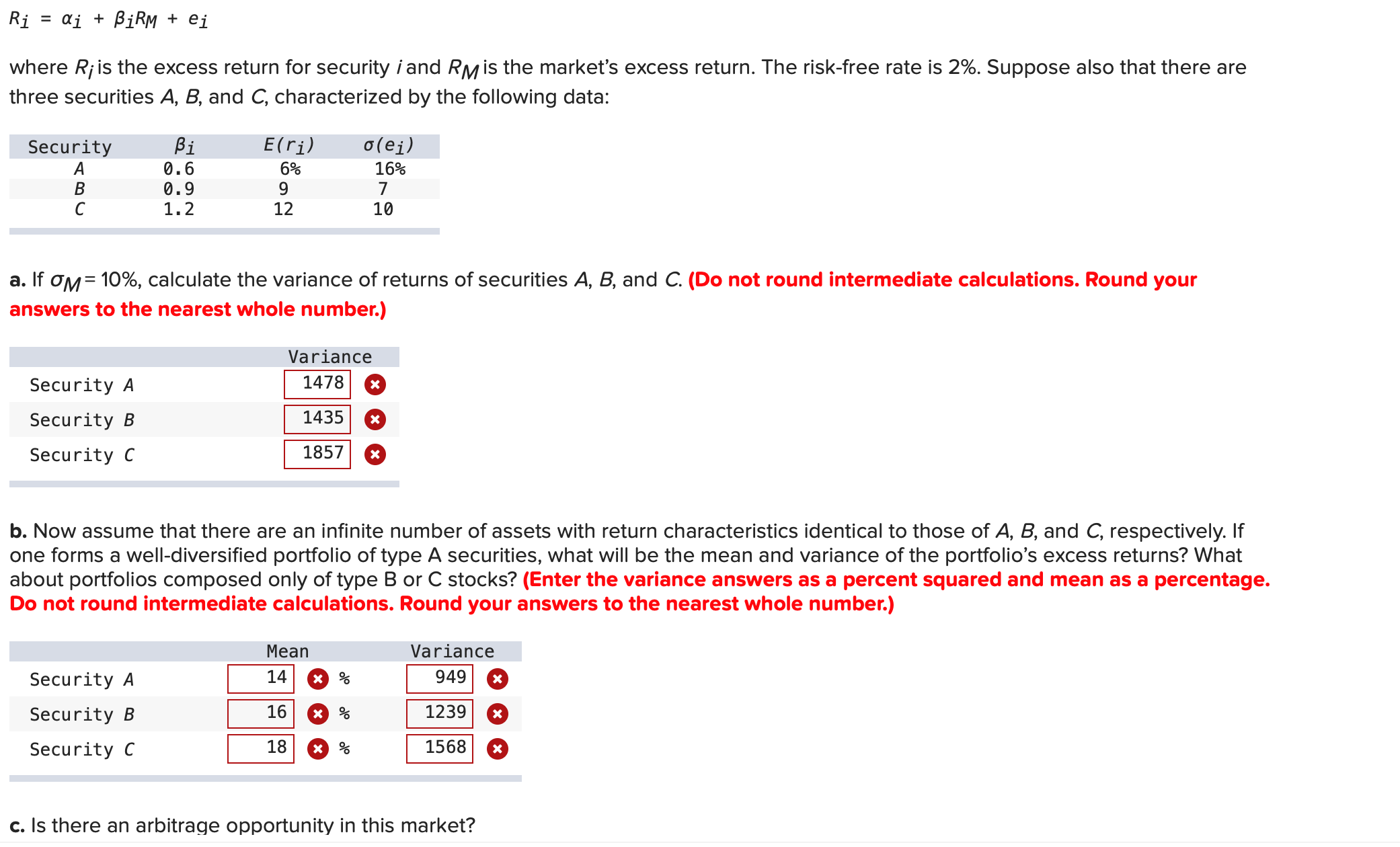

Consider the following multifactor (APT) model of security returns for a particular stock. Facto r Risk Factor Factor Beta Premium Inflation 1.3 696 Industrial production 0.8 8 Oil prices 0.5 5 a. If T-bills currently offer a 8% yield, nd the expected rate of return on this stock if the market views the stock as fairly priced. (Do not round intermediate calculations. Round your answer to 1 decimal place.) Expected rate of return 24.7 o % b. Suppose that the market expected the values for the three macro factors given in column 1 below, but that the actual values turn out as given in column 2. Calculate the revised expectations for the rate of return on the stock once the "surprises" become known. (Do not round intermediate calculations. Round your answer to 1 decimal place.) Expected Rate of Actual. Rate Factor Change of Change Inflation 795 695 Industrial production 4 7 Oil prices 3 0 Expected rate of return 21.4 o % Suppose that two factors have been identified for the Canadian economy: the growth rate of industrial production, IP, and the inflation rate, IR. IP is expected to be 3%, and IR 6.0%. A stock with a beta OH] on IP and 1.2 on IR currently is expected to provide a rate of return of 14%. If industrial production actually grows by 7%, while the inflation rate turns out to be 9.0%, what is your revised estimate of the expected rate of return on the stock? (Do not round intermediate calculations. Round your answer to 1 decimal place.) Revised expected rate of return 22.84 0 % R1 = 0:1- + BIRM+ el' where R,- is the excess return for security iand RM is the market's excess return. The risk-free rate is 2%. Suppose also that there are three securities A, B, and C, characterized by the following data: Security 31' EU'i) C(61) A 0.6 696 1696 B 0.9 9 7 C 1. 2 12 10 a. If 0M: 10%, calculate the variance of returns of securities A, B, and C. (Do not round intermediate calculations. Round your answers to the nearest whole number.) Variance Security A 1478 0 Security B 1435 0 Security C 1857 o b. Now assume that there are an innite number of assets with return characteristics identical to those of A, B, and C, respectively. If one forms a well-diversied portfolio of type A securities, what will be the mean and variance of the portfolio's excess returns? What about portfolios composed only of type B or C stocks? (Enter the variance answers as a percent squared and mean as a percentage. Do not round intermediate calculations. Round your answers to the nearest whole number.) Mean Variance Security A 14 o 9s 949 Q Security B 16 o 95 1239 0 Security C 18 o 95 1568 o c. Is there an arbitrage opportunity in this market

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock

Students Have Also Explored These Related Accounting Questions!