Question: Consider the following raw returns for Security J, Security K, and the market: Year J's Return K's Return Market Return 1 10% 10% 6% 2

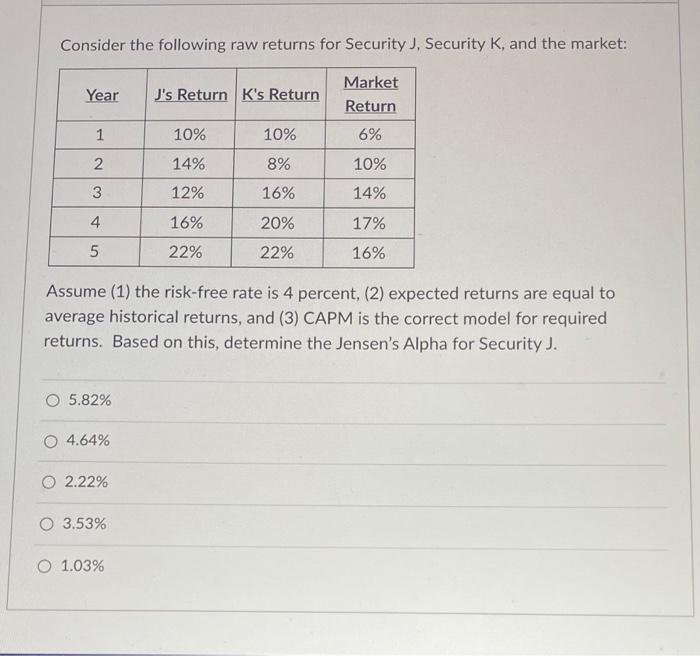

Consider the following raw returns for Security J, Security K, and the market: Year J's Return K's Return Market Return 1 10% 10% 6% 2 14% 8% 10% 3 12% 16% 14% 4 16% 20% 17% 5 22% 22% 16% Assume (1) the risk-free rate is 4 percent, (2) expected returns are equal to average historical returns, and (3) CAPM is the correct model for required returns. Based on this, determine the Jensen's Alpha for Security J. O 5.82% O 4.64% 0 2.22% O 3.53% O 1.03%

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock