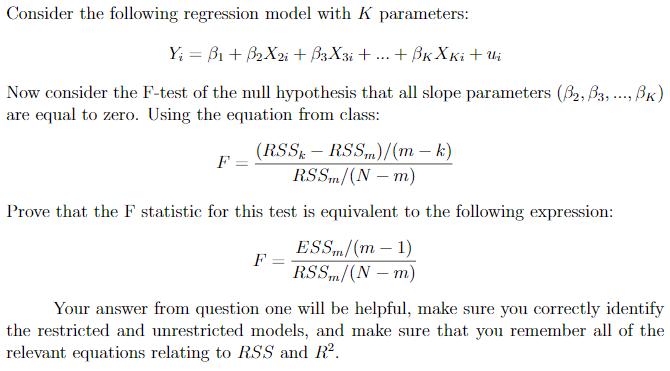

Question: Consider the following regression model with K parameters: Y; = B1 + B2X2: + B3 X3i +. + i + ; Now consider the

Consider the following regression model with K parameters: Y; = B1 + B2X2: + B3 X3i +. + i + ; Now consider the F-test of the mull hypothesis that all slope parameters (B2, B3, ., BK) are equal to zero. Using the equation from class: (RSS - RSSm)/(m-k) RSSm/(N - m) Prove that the F statistic for this test is equivalent to the following expression: ESS/(m 1) F : RSSm/(N m) Your answer from question one will be helpful, make sure you correctly identify the restricted and unrestricted models, and make sure that you remember all of the relevant equations relating to RSS and R2.

Step by Step Solution

3.39 Rating (155 Votes )

There are 3 Steps involved in it

To prove that the F statistic given in the problem is equivalent to the other expression lets break ... View full answer

Get step-by-step solutions from verified subject matter experts