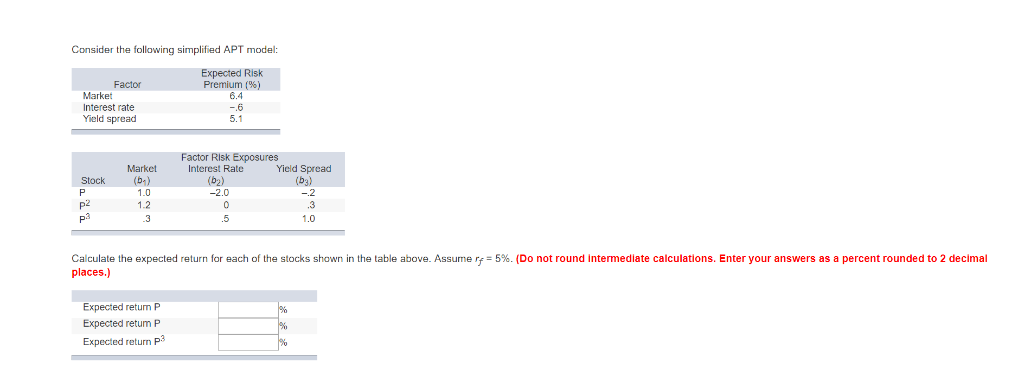

Question: Consider the following simplified APT model: Expected Risk Premium (%) 6.4 Factor Market Interest rate Yield spread Factor Risk Exposures Market Interest Rate (b2) -2.0

Consider the following simplified APT model: Expected Risk Premium (%) 6.4 Factor Market Interest rate Yield spread Factor Risk Exposures Market Interest Rate (b2) -2.0 Yield Spread Stock (b) (b3) 1.0 p2 Pa .3 1.0 .3 .5 Calculate the expected return for each of the stocks shown in the table above. Assume rf-5%.(Do not round intemediate calculations. Enter your answers as a percent rounded to 2 decimal places.) Expected retum P Expected retum P Expected return P3

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock