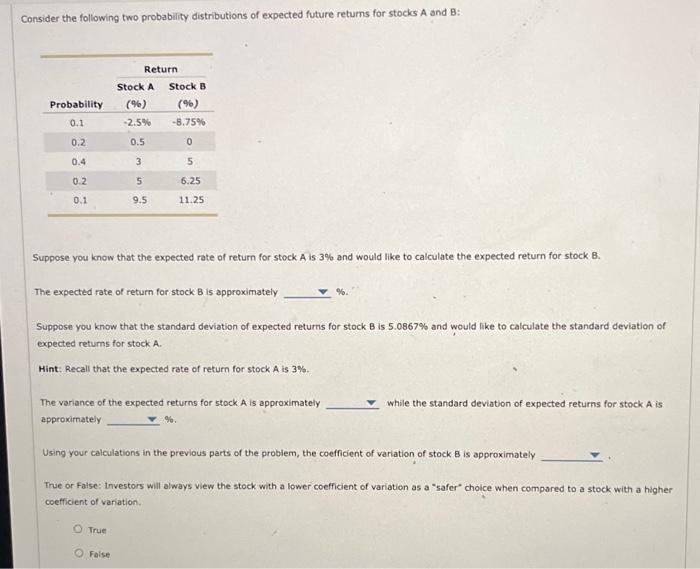

Question: Consider the following two probability distributions of expected future returns for stocks A and B: Suppose you know that the expected rate of return for

Consider the following two probability distributions of expected future returns for stocks A and B: Suppose you know that the expected rate of return for stock A is 3% and would like to calculate the expected return for stock B. The expected rate of return for stock B is approximately \%. Suppose you know that the standard deviation of expected returns for stock B is 5.0867% and would like to calculate the standard deviation of expected returns for stock A. Hint: Recall that the expected rate of return for stock A is 3%. The vanance of the expected returns for stock A is approximately While the standard deviation of expected returns for stock A is approximately %. Using your calculations in the previous parts of the problem, the coefficient of variation of stock 8 is approximately True or False: investors will always view the stock with a lower coefficient of variation as a "safer" choice when compared to a stock with a higher coefficient of variation. True raise

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts