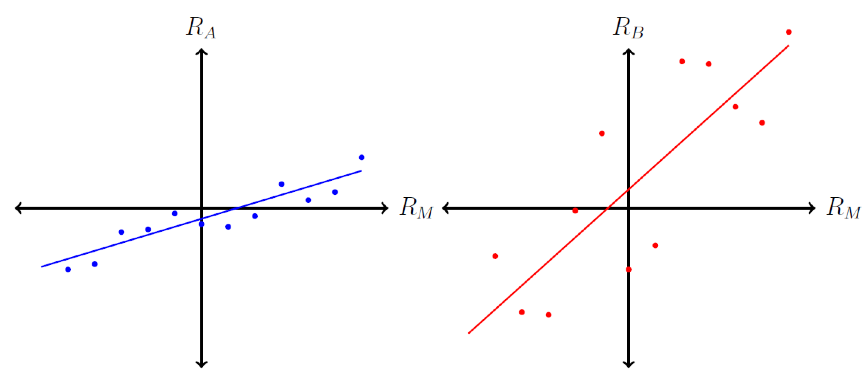

Consider the following two security characteristic lines (SCL) for stock A and Stock B with R A

Fantastic news! We've Found the answer you've been seeking!

Question:

Consider the following two security characteristic lines (SCL) for stock A and Stock B with RA, RB, and RM representing the excess returns of stock A, stock B, and the market index M, respectively:

1. Which stock has a higher firm-specific variance?

2. Which stock has a higher systematic variance?

3. Which stock has a higher R-squared in the regression?

4. Which stock has a higher alpha?

5. Which stock has a higher correlation with the market index?

Expert Answer:

Posted Date: