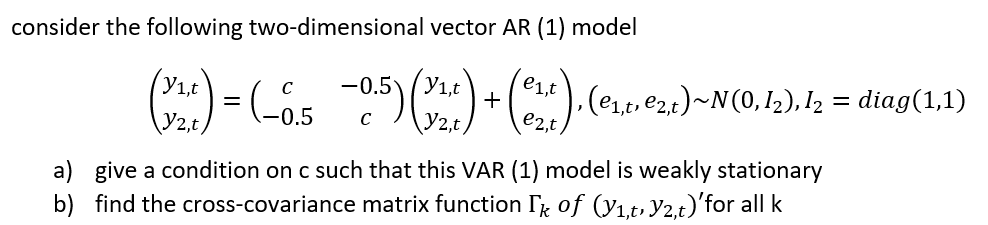

Question: consider the following two-dimensional vector AR (1) model (4):) = (-45 -0.5) (1):) + (83%). (09.02.)-N(0.1).la = diag(1.1) a) give a condition on c such

consider the following two-dimensional vector AR (1) model (4):) = (-45 -0.5) (1):) + (83%). (09.02.)-N(0.1).la = diag(1.1) a) give a condition on c such that this VAR (1) model is weakly stationary b) find the cross-covariance matrix function Ik of (71,t, Y2,t)'for all k consider the following two-dimensional vector AR (1) model (4):) = (-45 -0.5) (1):) + (83%). (09.02.)-N(0.1).la = diag(1.1) a) give a condition on c such that this VAR (1) model is weakly stationary b) find the cross-covariance matrix function Ik of (71,t, Y2,t)'for all k

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock