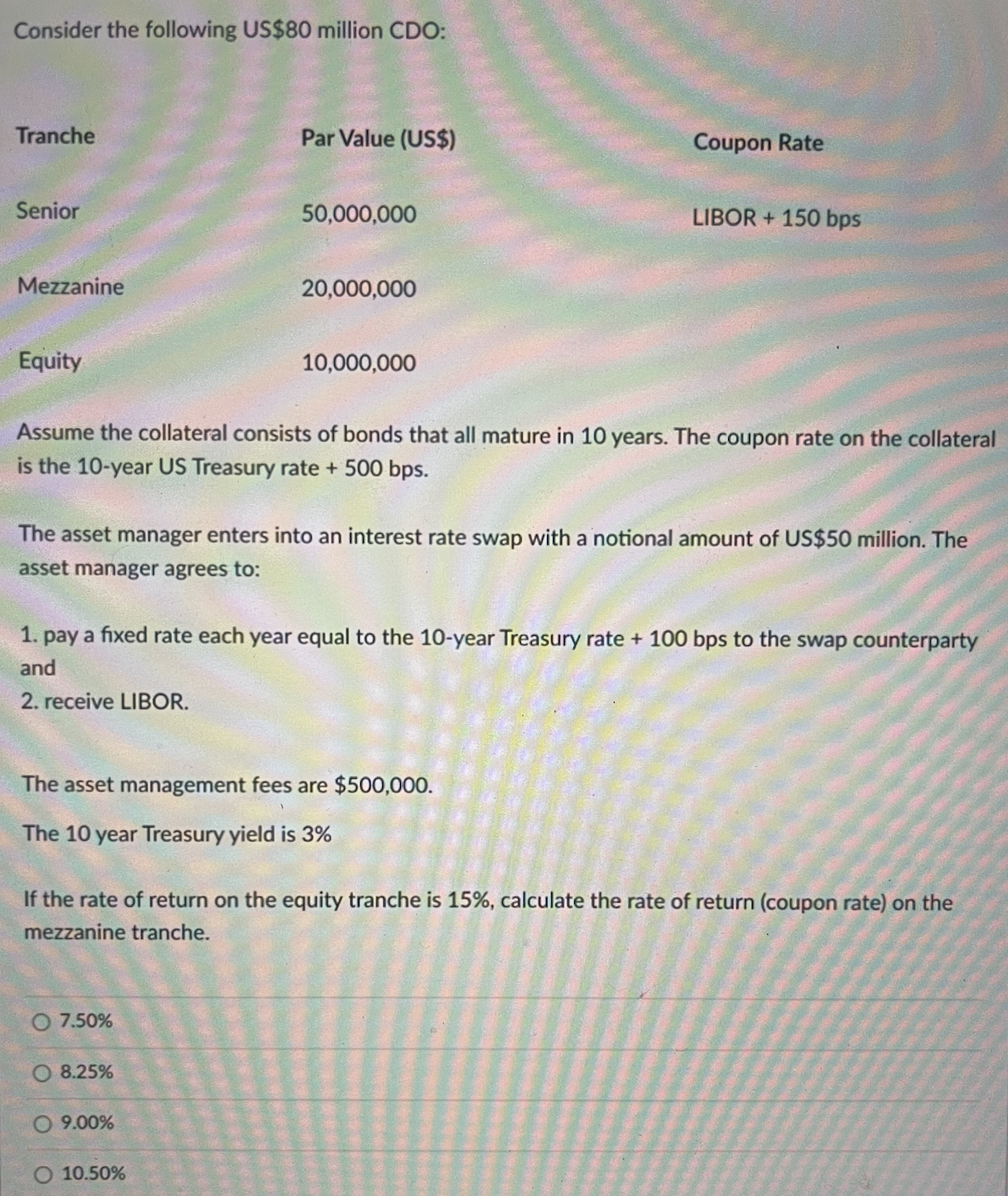

Question: Consider the following US$80 million CDO: Tranche Par Value (US$) Coupon Rate Senior 50,000,000 LIBOR + 150 bps Mezzanine 20,000,000 Equity 10,000,000 Assume the collateral

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock