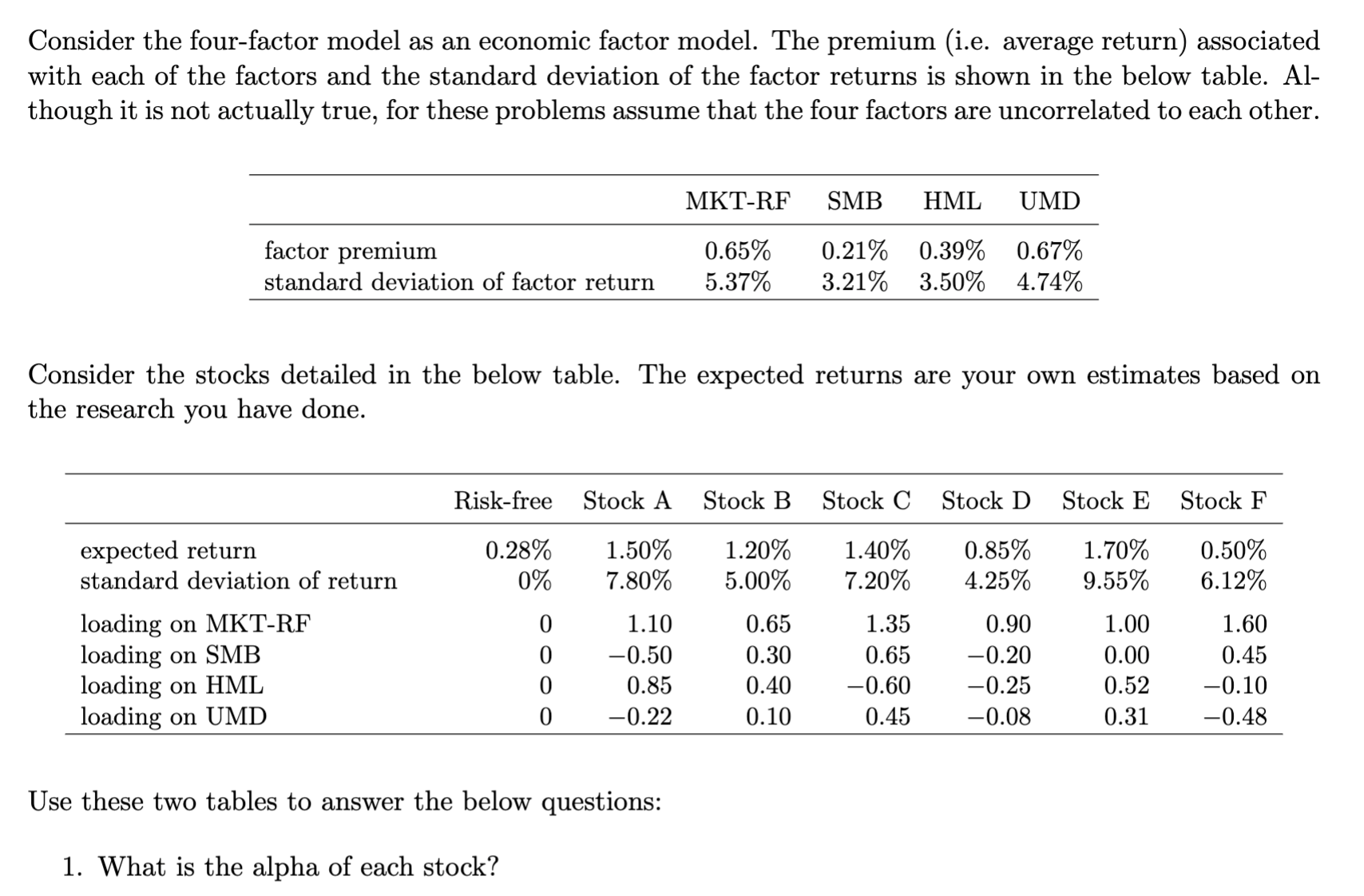

Question: Consider the four-factor model as an economic factor model. The premium (i.e. average return) associated with each of the factors and the standard deviation of

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts