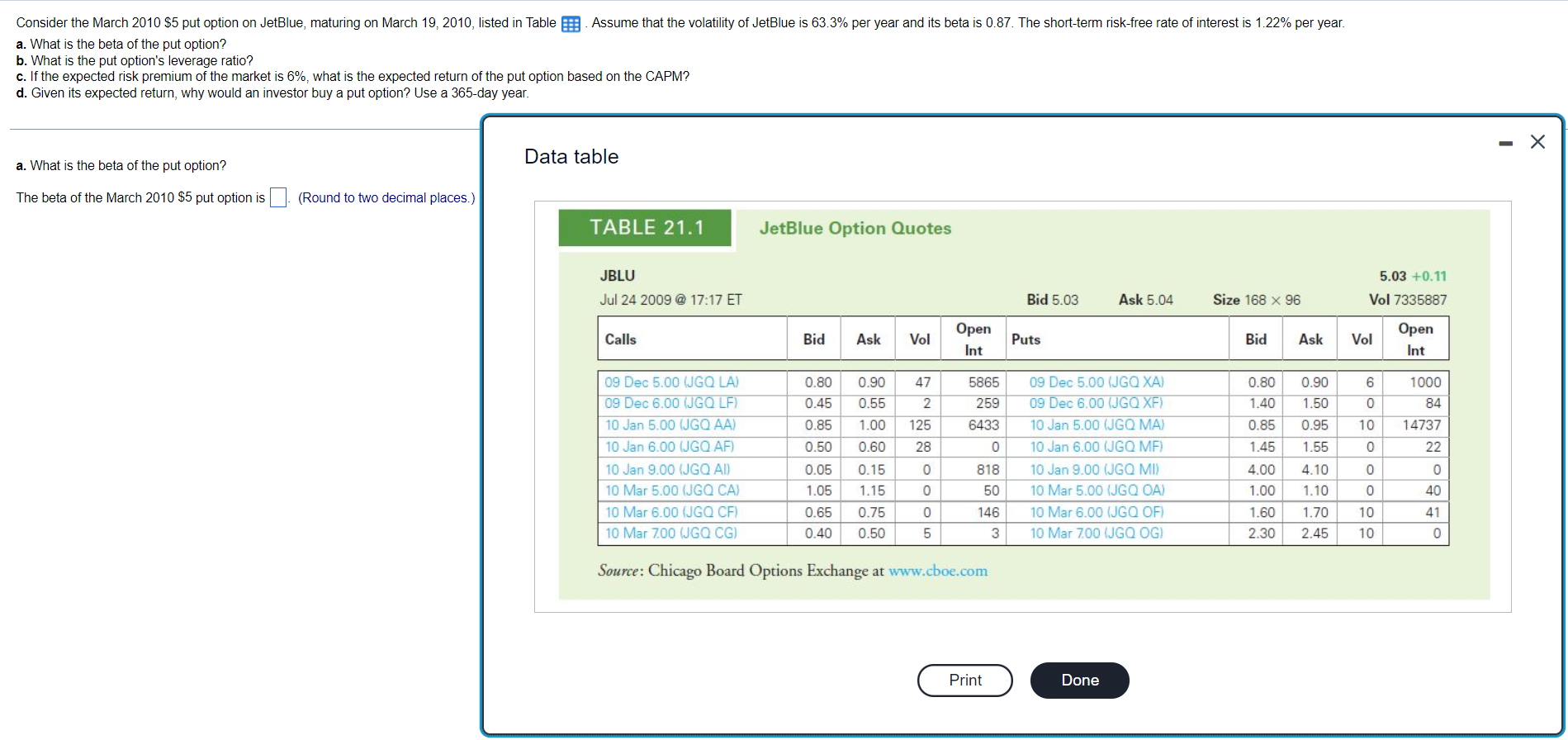

Question: Consider the March 2010$5put option on JetBlue, maturing on March 19, 2010, listed in Table .Assume that the volatility of JetBlue is 63.3%per year and

Consider the March 2010$5put option on JetBlue, maturing on March 19, 2010, listed in Table .Assume that the volatility of JetBlue is 63.3%per year and its beta is 0.87. The short-term risk-free rate of interest is 1.22% per year.

a. What is the beta of the put option?

b. What is the put option's leverage ratio?

c. If the expected risk premium of the market is 6%, what is the expected return of the put option based on the CAPM?

d. Given its expected return, why would an investor buy a put option? Use a 365-day year.

Consider the March 2010 $5 put option on JetBlue, maturing on March 19, 2010, listed in Table Assume that the volatility of JetBlue is 63.3% per year and its beta is 0.87. The short-term risk-free rate of interest is 1.22% per year. a. What is the beta of the put option? b. What is the put option's leverage ratio? c. If the expected risk premium of the market is 6%, what is the expected return of the put option based on the CAPM? d. Given its expected return, why would an investor buy a put option? Use a 365-day year. - X Data table a. What is the beta of the put option? The beta of the March 2010 $5 put option is (Round to two decimal places.) TABLE 21.1 JetBlue Option Quotes JBLU 5.03 +0.11 Jul 24 2009 @ 17:17 ET Bid 5.03 Ask 5.04 Size 168 x 96 Vol 7335887 Calls Bid Ask Vol Open Int Puts Bid Ask Vol Open Int 47 0.90 0.55 2 000 84 14737 22 1.00 125 10 28 09 Dec 5.00 (JGQ LA) 09 Dec 6.00 (JGOLF) 10 Jan 5.00 (JGO AA) 10 Jan 6.00 (JGO AF) 10 Jan 9.00 (JGO AI 10 Mar 5.00 (JGQ CA) 10 Mar 6.00 (JGO CF) 10 Mar 7.00 (JGQ CG) 0.80 0.45 0.85 0.50 0.05 1.05 0.65 0.40 5865 259 6433 0 818 50 146 3 Dec 5.00 (JGQ XA) 09 Dec 6.00 (JGQ XF) 10 Jan 5.00 (JGQ MA 10 Jan 6.00 (JGQ MF) 10 Jan 9.00 (JGO MI) 10 Mar 5.00 (JGQ OA) 10 Mar 6.00 (JGQ OF) 10 Mar 7.00 (JGQ OG) 0.60 0.15 1.15 0.75 0.50 0.80 1.40 0.85 1.45 4.00 1.00 1.60 2.30 0.90 1.50 0.95 1.55 4.10 1.10 1.70 2.45 6 O OOOOOO 0 0 0 40 10 41 0 5 10 0 Source: Chicago Board Options Exchange at www.cboe.com Print Done Consider the March 2010 $5 put option on JetBlue, maturing on March 19, 2010, listed in Table Assume that the volatility of JetBlue is 63.3% per year and its beta is 0.87. The short-term risk-free rate of interest is 1.22% per year. a. What is the beta of the put option? b. What is the put option's leverage ratio? c. If the expected risk premium of the market is 6%, what is the expected return of the put option based on the CAPM? d. Given its expected return, why would an investor buy a put option? Use a 365-day year. - X Data table a. What is the beta of the put option? The beta of the March 2010 $5 put option is (Round to two decimal places.) TABLE 21.1 JetBlue Option Quotes JBLU 5.03 +0.11 Jul 24 2009 @ 17:17 ET Bid 5.03 Ask 5.04 Size 168 x 96 Vol 7335887 Calls Bid Ask Vol Open Int Puts Bid Ask Vol Open Int 47 0.90 0.55 2 000 84 14737 22 1.00 125 10 28 09 Dec 5.00 (JGQ LA) 09 Dec 6.00 (JGOLF) 10 Jan 5.00 (JGO AA) 10 Jan 6.00 (JGO AF) 10 Jan 9.00 (JGO AI 10 Mar 5.00 (JGQ CA) 10 Mar 6.00 (JGO CF) 10 Mar 7.00 (JGQ CG) 0.80 0.45 0.85 0.50 0.05 1.05 0.65 0.40 5865 259 6433 0 818 50 146 3 Dec 5.00 (JGQ XA) 09 Dec 6.00 (JGQ XF) 10 Jan 5.00 (JGQ MA 10 Jan 6.00 (JGQ MF) 10 Jan 9.00 (JGO MI) 10 Mar 5.00 (JGQ OA) 10 Mar 6.00 (JGQ OF) 10 Mar 7.00 (JGQ OG) 0.60 0.15 1.15 0.75 0.50 0.80 1.40 0.85 1.45 4.00 1.00 1.60 2.30 0.90 1.50 0.95 1.55 4.10 1.10 1.70 2.45 6 O OOOOOO 0 0 0 40 10 41 0 5 10 0 Source: Chicago Board Options Exchange at www.cboe.com Print Done

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts