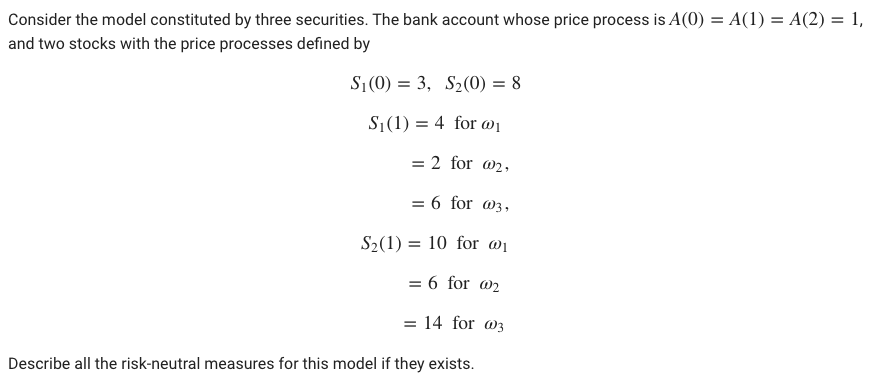

Question: Consider the model constituted by three securities. The bank account whose price process is AO) = A(1) = A(2) = 1, and two stocks with

Consider the model constituted by three securities. The bank account whose price process is AO) = A(1) = A(2) = 1, and two stocks with the price processes defined by Si(0) = 3, S2(0) = 8 Si(1) = 4 for 1 = 2 for 02, = 6 for 03 S2(1) = 10 for 01 = 6 for 02 = 14 for 03 Describe all the risk-neutral measures for this model if they exists. Consider the model constituted by three securities. The bank account whose price process is AO) = A(1) = A(2) = 1, and two stocks with the price processes defined by Si(0) = 3, S2(0) = 8 Si(1) = 4 for 1 = 2 for 02, = 6 for 03 S2(1) = 10 for 01 = 6 for 02 = 14 for 03 Describe all the risk-neutral measures for this model if they exists

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts