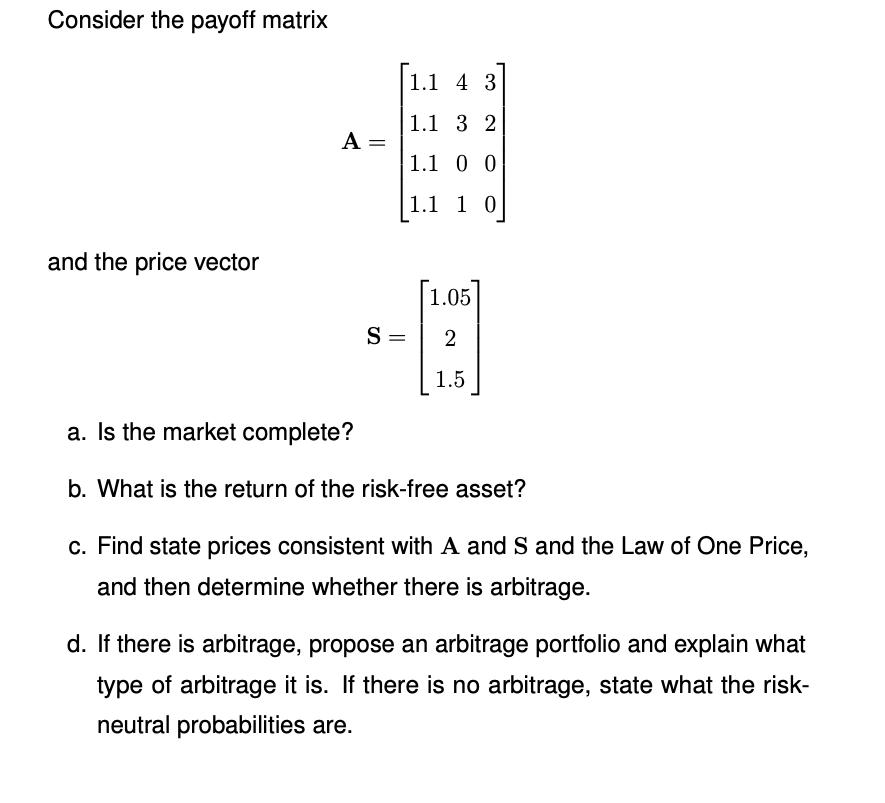

Question: Consider the payoff matrix and the price vector A = S= = 1.1 4 3 1.1 3 2 1.1 0 0 1.1 1 0

Consider the payoff matrix and the price vector A = S= = 1.1 4 3 1.1 3 2 1.1 0 0 1.1 1 0 [1.05 2 1.5 a. Is the market complete? b. What is the return of the risk-free asset? c. Find state prices consistent with A and S and the Law of One Price, and then determine whether there is arbitrage. d. If there is arbitrage, propose an arbitrage portfolio and explain what type of arbitrage it is. If there is no arbitrage, state what the risk- neutral probabilities are.

Step by Step Solution

★★★★★

3.45 Rating (148 Votes )

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock