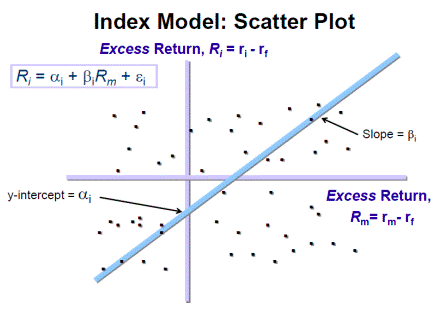

Question: Consider the scatter plot from the single index model: Which of the following statements must be true? [I] If the systematic component of the individual

Consider the scatter plot from the single index model: Which of the following statements must be true?

[I] If the systematic component of the individual stocks excess return is positive, the total excess return of the individual stock (Ri) may be negative.

[II] If the total excess return of the individual stock (Ri) is positive, then the idiosyncratic return component must be positive.

[III] If the idiosyncratic component and total excess return of the individual stock (Ri) is negative, the systematic return component must be negative.

Y-axis represents returns for Stock i while X-axis represents market returns.

Index Model: Scatter Plot Excess Return, Ri = ri-r slope-p y-intercept = Excess Return

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts