Question: Consider the single-period market model M=(B, S, S) with three states of nature N = {W, W2, W3}. Let the interest rate be r

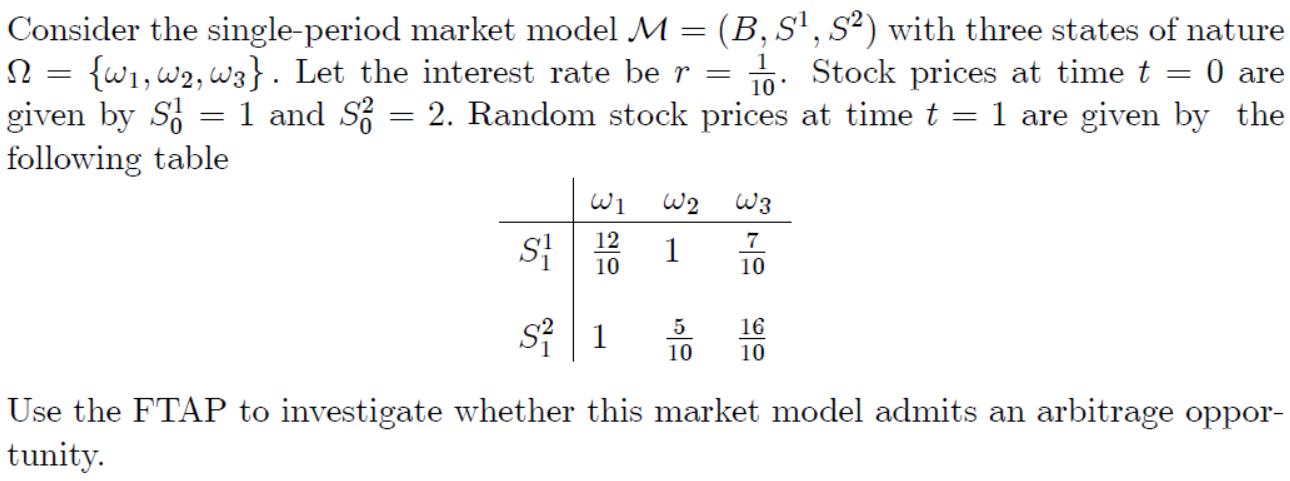

Consider the single-period market model M=(B, S, S) with three states of nature N = {W, W2, W3}. Let the interest rate be r = Stock prices at time t = 0 are = = 1 are given by the given by S 1 and S2 = 2. Random stock prices at time t following table S W1 W2 W3 12 7 1 10 10 5 16 S1 10 10 Use the FTAP to investigate whether this market model admits an arbitrage oppor- tunity.

Step by Step Solution

3.55 Rating (155 Votes )

There are 3 Steps involved in it

To investigate whether the given singleperiod market model admits an arbitrage opportunity we can use the Fundamental Theorem of Asset Pricing FTAP wh... View full answer

Get step-by-step solutions from verified subject matter experts