Question: Consider the time series Y = 0.7 +0.4Y{_1+0.12Y-2+ where e is a white noise process with variance . (i) Identify the model as an

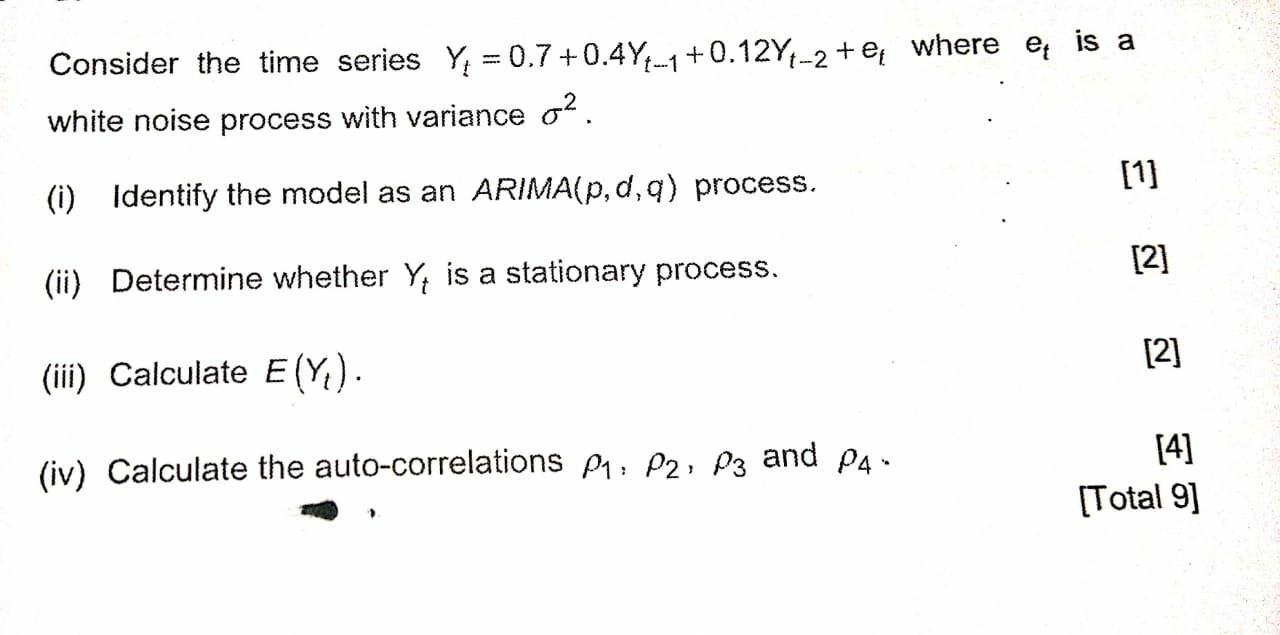

Consider the time series Y = 0.7 +0.4Y{_1+0.12Y-2+ where e is a white noise process with variance . (i) Identify the model as an ARIMA(p,d,q) process. (ii) Determine whether Y is a stationary process. (iii) Calculate E(Y). (iv) Calculate the auto-correlations P1, P2, P3 and P4- [1] [2] [2] [4] [Total 9]

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock