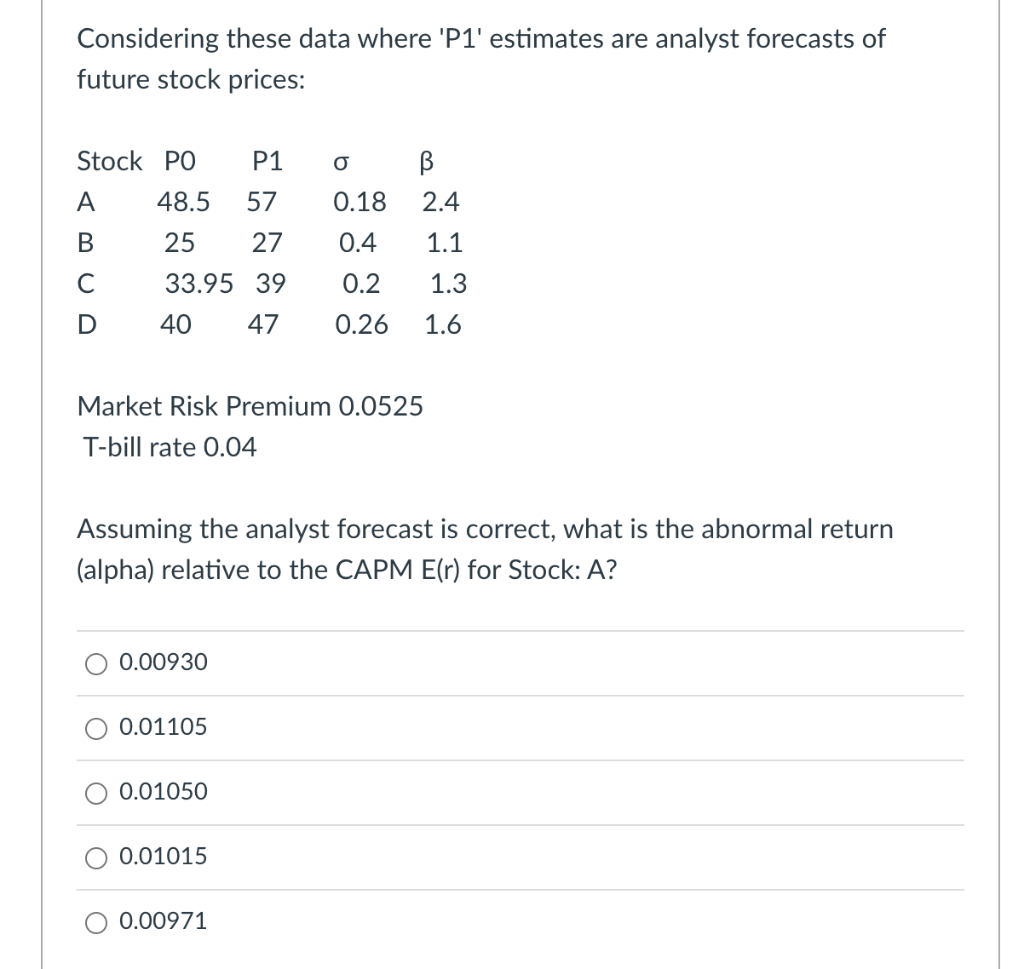

Question: Considering these data where 'Pl' estimates are analyst forecasts of future stock prices: P1 0 Stock PO A 48.5 B 2.4 57 0.18 B 25

Considering these data where 'Pl' estimates are analyst forecasts of future stock prices: P1 0 Stock PO A 48.5 B 2.4 57 0.18 B 25 27 0.4 1.1 C 0.2 1.3 33.95 39 40 47 D 0.26 1.6 Market Risk Premium 0.0525 T-bill rate 0.04 Assuming the analyst forecast is correct, what is the abnormal return (alpha) relative to the CAPM E(r) for Stock: A? 0.00930 0.01105 0.01050 0.01015 O 0.00971

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock