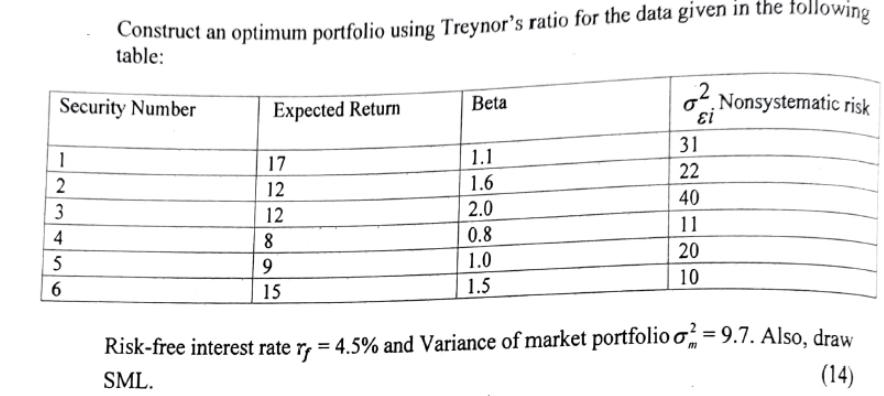

Question: Construct an optimum portfolio using Treynor's ratio for the data given in the following table: Security Number 1 2 3 4 5 6 Expected

Construct an optimum portfolio using Treynor's ratio for the data given in the following table: Security Number 1 2 3 4 5 6 Expected Return 17 12 12 8 9 15 Beta 1.1 1.6 2.0 0.8 1.0 1.5 31 22 40 11 20 10 Nonsystematic risk Risk-free interest rate r = 4.5% and Variance of market portfolio 2 =9.7. Also, draw (14) SML. Construct an optimum portfolio using Treynor's ratio for the data given in the following table: Security Number 1 2 3 4 5 6 Expected Return 17 12 12 8 9 15 Beta 1.1 1.6 2.0 0.8 1.0 1.5 31 22 40 11 20 10 Nonsystematic risk Risk-free interest rate r = 4.5% and Variance of market portfolio 2=9.7. Also, draw (14) SML.

Step by Step Solution

There are 3 Steps involved in it

To construct an optimum portfolio using Treynors ratio we need to calculate the Treynor ratio for ... View full answer

Get step-by-step solutions from verified subject matter experts