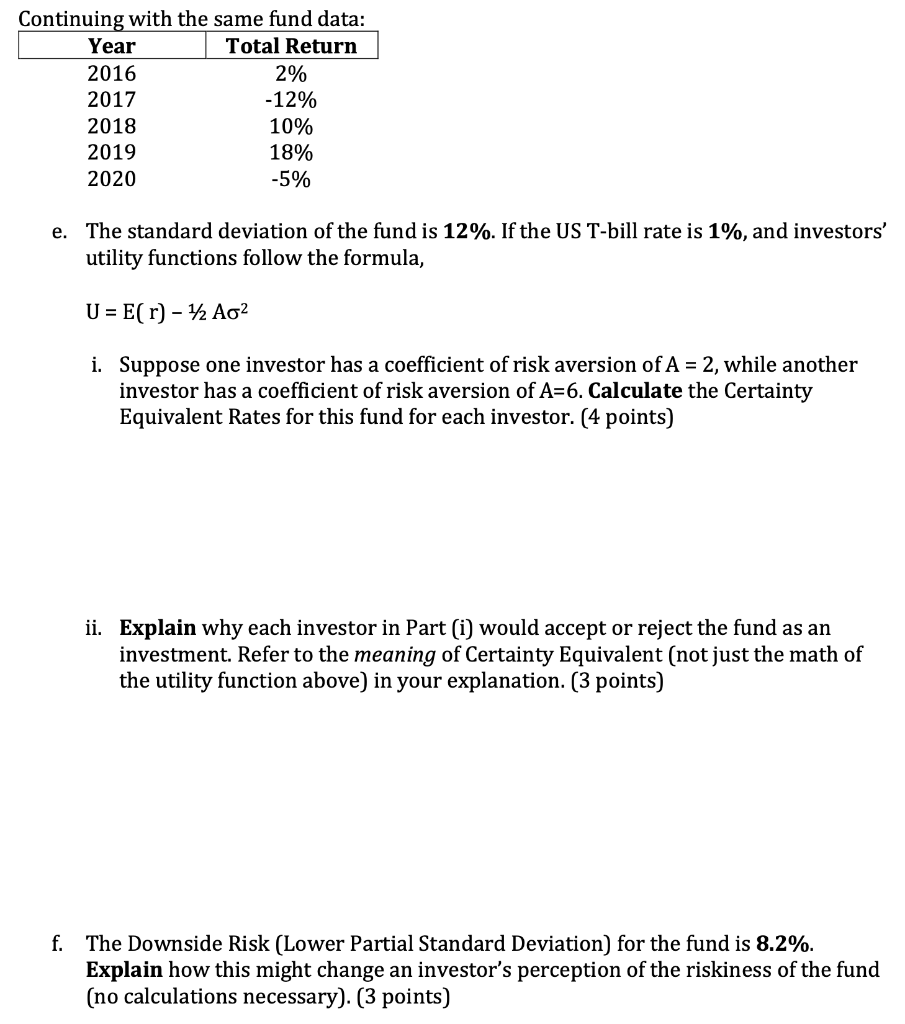

Question: Continuing with the same fund data: Year Total Return 2016 2% 2017 -12% 2018 10% 2019 18% 2020 -5% e. The standard deviation of the

Continuing with the same fund data: Year Total Return 2016 2% 2017 -12% 2018 10% 2019 18% 2020 -5% e. The standard deviation of the fund is 12%. If the US T-bill rate is 1%, and investors' utility functions follow the formula, U = E( r) - 12 Ag2 i. Suppose one investor has a coefficient of risk aversion of A = 2, while another investor has a coefficient of risk aversion of A=6. Calculate the Certainty Equivalent Rates for this fund for each investor. (4 points) ii. Explain why each investor in Part (i) would accept or reject the fund as an investment. Refer to the meaning of Certainty Equivalent (not just the math of the utility function above) in your explanation. (3 points) f. The Downside Risk (Lower Partial Standard Deviation) for the fund is 8.2%. Explain how this might change an investor's perception of the riskiness of the fund (no calculations necessary). (3 points) Continuing with the same fund data: Year Total Return 2016 2% 2017 -12% 2018 10% 2019 18% 2020 -5% e. The standard deviation of the fund is 12%. If the US T-bill rate is 1%, and investors' utility functions follow the formula, U = E( r) - 12 Ag2 i. Suppose one investor has a coefficient of risk aversion of A = 2, while another investor has a coefficient of risk aversion of A=6. Calculate the Certainty Equivalent Rates for this fund for each investor. (4 points) ii. Explain why each investor in Part (i) would accept or reject the fund as an investment. Refer to the meaning of Certainty Equivalent (not just the math of the utility function above) in your explanation. (3 points) f. The Downside Risk (Lower Partial Standard Deviation) for the fund is 8.2%. Explain how this might change an investor's perception of the riskiness of the fund (no calculations necessary). (3 points)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts