Question: Corresponding journal entries: Below is the excel document. The two go together side-by-side (It was too grainy when I tried to screenshot it as one).

Corresponding journal entries:

Corresponding journal entries:

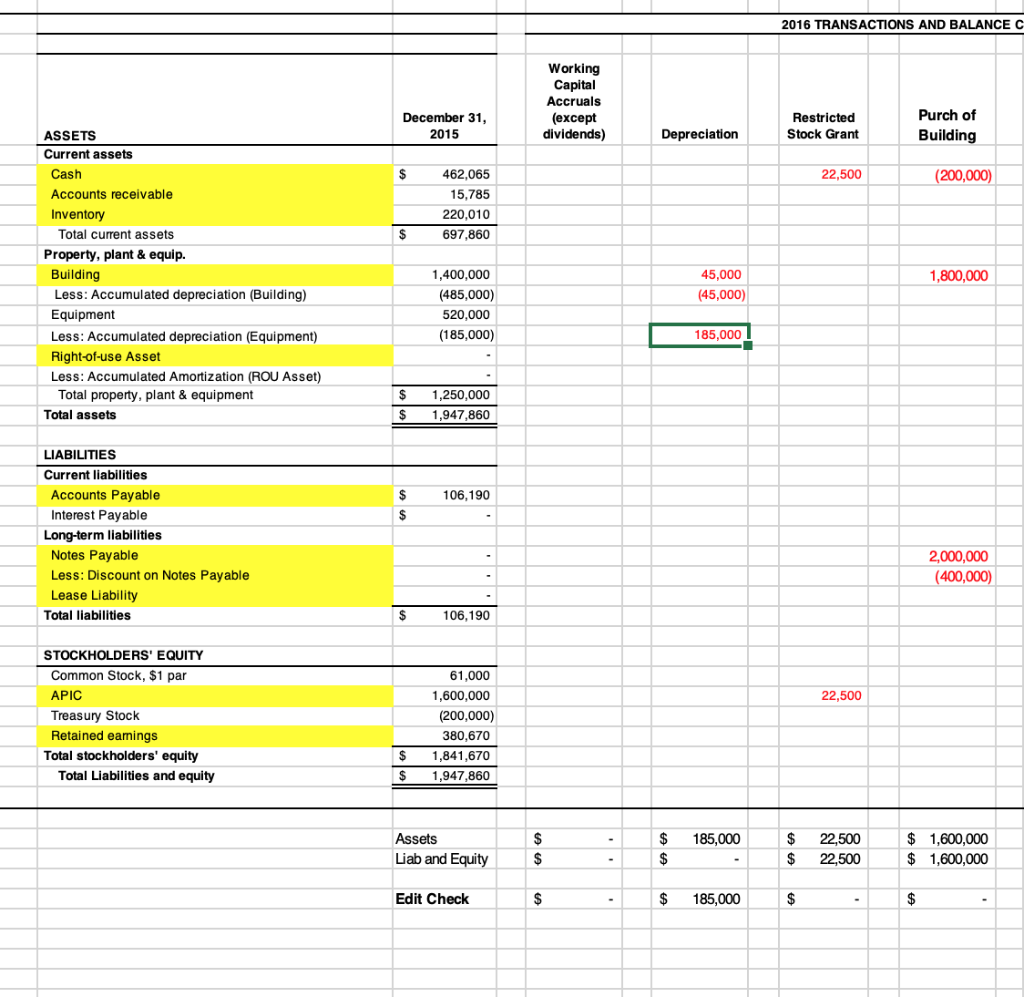

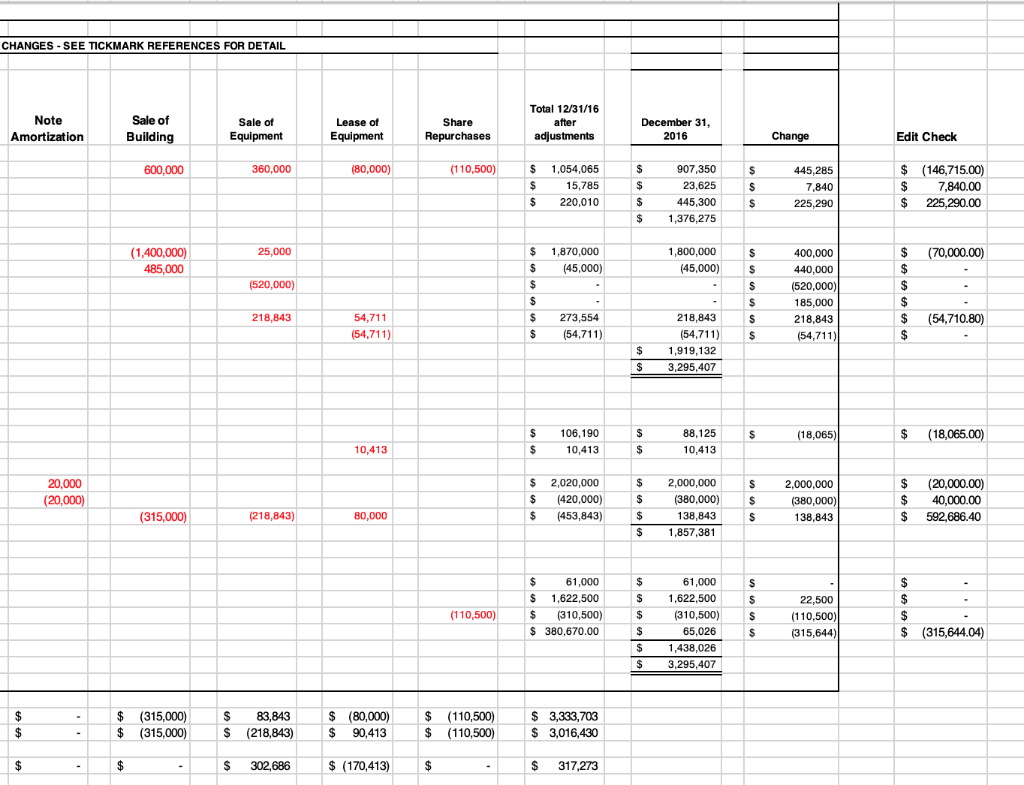

Below is the excel document. The two go together side-by-side (It was too grainy when I tried to screenshot it as one). The red numbers are my own work and I am trying to get the bottom "edit check" to equal 0 along with the far right column "edit check", but can't seem to figure it out! Let me know if you have any other questions- I tried to make it as clear as possible:

Below is the excel document. The two go together side-by-side (It was too grainy when I tried to screenshot it as one). The red numbers are my own work and I am trying to get the bottom "edit check" to equal 0 along with the far right column "edit check", but can't seem to figure it out! Let me know if you have any other questions- I tried to make it as clear as possible:

3. Utilize the empty columns in the comparative balance sheet to enter the effects of each transaction as an adjustment to the balance sheet during the year 2016. You should use links to bring the information from tab D to the columns in tab A. NOTE: Carefully consider which signs the numbers should be (aka positive or negative) when entering them to adjust each account. You may have to switch the signs when you link the numbers. Notice there are Edit Checks to ensure completeness across the bottom and far right side of the spreadsheet in Tab A. If you have made the correct adjustments, the Edit Checks will zero out. After completing all the relevant columns in the Balance Sheet, the numbers in the column "Total 12/31/16 after adjustments" should equal the numbers in the "December 31, 2016" column. The following income statement items were available for the year 2016: Sales COGS Other Operating Expenses* 605,750 304,450 174,320 *Besides depreciation, amortization, incentive compensation or interest expenses Note: Both purchases of inventory and other operating expenses are paid through Accounts Payable 2. Wildcat depreciates its fixed assets using the straight-line method with no salvage value based on the following useful lives: Buildings Equipment 20 years 8 years 3. Wildcat made the following share repurchases during the year: October November December 5000 shares@$8 per share 7500 shares@ $7 per share 3000 shares@$6 per share 2016: FULL YEAR Treasury Stock 110,500 Cash 110,500 4. On September 30, 2016, Wildcat granted incentive compensation to executives in the form of 10,000 shares of Restricted Stock with a fair value of $9 per share. The restricted stock is scheduled to vest on September 30, 2017 22,500 SEPT. 20, 2016 Incentlve Comp expense APIC-options 22,500 5. On July 1, 2016, Wildcat purchased a new, larger building for its primary operations by making a cash down payment of $200,000 and financing the remainder by issuing a $2,000,000 zero-interest bearing note from its revolving line of credit. Based on the interest rate implicit in its line of credit, the present value of the note payable at the time of issuance was $1,600,000. The note carries a 10 year maturity, coming due on July 1, 2026 JULY1,2016 Building-New 1,800,000 400,000 Discount on Notes Payable Notes Payable Cash 2,000,000 200,000 45,000 DEC 31st, 2016 Depreciation Expense Accumulated Depreciation-new building 45,000 Interest Expense- N/P 20,000 Discount on N/P 20,000 6 6. August 31, 2016, Wildcat completed the sale of its old building for $600,000 in cash. AUGUST 31st, 20 Cash 600,000 485,000 315,000 Accumulated Depreciation-Old Building Loss on Sale Building-Old 1,400,000 7. On March 31, 2016, Wildcat sold all ofits equipment based on a decision to rent the equipment rather than own it. The equipment was sold for $360,000 in cash. On the same date, Wildcat entered into an agreement with Sun Company to lease equipment for $80,000 per year over a 3 year lease term. At the time of the lease agreement, the estimated fair value of the equipment was $360,000 and the expected useful life was 8 years. Lease payments are due annually at the beginning of the lease term with the first payment made on March 31, 2016. Wildcat's technical accountants have determined that the terms of the lease constitute atransfer ofthe rights and rewards of ownership to wildcat, wildcat's incremental borrowing rate is 10%. 360,000 185,000 MARCH 31st, 201 Cash Accumulated Depreciation-Equipment 520,000 Equipment Gain on Sale of Equipment 25,000 218,843 80,000 54,711 10,413 Right of Use Asset Lease Liability Amortization Expense Interest Expense-Lease 218,843 80,000 54,711 10,413 Lease Liability Cash ROU Asset Interest Payable-Lease 2016 TRANSACTIONS AND BALANCE C Working Capital Accruals (except dividends) Purch of Building December 31, 2015 Restricted Stock Grant Depreciation ASSETS Current assets Cash Accounts receivable Inventory $ 462,065 15,785 220,010 697,860 22,500 200 Total current assets Property, plant &equip. Building Less: Accumulated depreciation (Building) Equipment Less: Accumulated depreciation (Equipment) Right-of-use Asset Less: Accumulated Amortization (ROU Asset) 45,000 (45,000) 1,400,000 (485,000) 520,000 (185,000) 1,800,000 185,000 Total property, plant & equipment Total assets $ 1,250,000 $ 1,947,860 LIABILITIES Current liabilities Accounts Payable Interest Payable 106,190 Long-term liabilities Notes Payable Less: Discount on Notes Payable Lease Liability 2,000,000 Total liabilities 106,190 STOCKHOLDERS' EQUITY Common Stock, $1 par APIC Treasury Stock Retained eamings 61,000 1,600,000 (200,000) 380,670 $ 1,841,670 $ 1,947,860 22,500 Total stockholders' equity Total Liabilities and equity $185,000 $ 22,500 $ 22,500 Assets Liab and Equity$ Edit Check $ 1,600,000 $ 1,600,000 $185,000 CHANGES -SEE TICKMARK REFERENCES FOR DETAIL Total 12/31/16 after adjustments Sale of Building Note Amortization Sale of Equipment Lease of Equipment Share Repurchases December 31 2016 Change Edit Check 445,285 7,840 225,290 $ (146,715.00) $7,840.00 $225,290.00 600,000 360,000 (80,000) (110,500) $ 1,054,065 907,350 23,625 445,300 $ 1,376,275 15,785 S 220,010 $ 1,870,000 $ (45,000) 1,800,000 45,000) S 1,400,000) 485,000 25,000 400,000 440,000 520,000) 185,000 218,843 (520,000) 54,711 (54,711) $(54,710.80) 218,843 $273,554 (54,711) 218,843 (54,711) $ 1,919,132 3,295,407 $ 106,190 10,413 $(18,065.00) 88,125 10,413 (18,065) 10,413 $ 2,020,000 $(20,000.00) $40,000.00 $592,686.40 20,000 20 $2,000,000 S 2,000,000 $ 420,000) $ (380,000)S 138,843 $ 1,857,38 (380,000) 138,843 315, $ (453,843) (218,843) 80,000 $ 61,000 S 1,622,500 $(310,500) S 380,670.00 61,000 $ 1,622,500 (310,500S 65,026 $ 1,438,026 $ 3,295,407 22,500 (110,500) (315,644) (110,500) $ (315,644.04) $(315,000 83,843 (80,000(110,500)S 3,333,703 $(315,000 (218,843)S 90,413(110,500)S 3,016,430 $ 302, 686 (170,413) $ 317,273 3. Utilize the empty columns in the comparative balance sheet to enter the effects of each transaction as an adjustment to the balance sheet during the year 2016. You should use links to bring the information from tab D to the columns in tab A. NOTE: Carefully consider which signs the numbers should be (aka positive or negative) when entering them to adjust each account. You may have to switch the signs when you link the numbers. Notice there are Edit Checks to ensure completeness across the bottom and far right side of the spreadsheet in Tab A. If you have made the correct adjustments, the Edit Checks will zero out. After completing all the relevant columns in the Balance Sheet, the numbers in the column "Total 12/31/16 after adjustments" should equal the numbers in the "December 31, 2016" column. The following income statement items were available for the year 2016: Sales COGS Other Operating Expenses* 605,750 304,450 174,320 *Besides depreciation, amortization, incentive compensation or interest expenses Note: Both purchases of inventory and other operating expenses are paid through Accounts Payable 2. Wildcat depreciates its fixed assets using the straight-line method with no salvage value based on the following useful lives: Buildings Equipment 20 years 8 years 3. Wildcat made the following share repurchases during the year: October November December 5000 shares@$8 per share 7500 shares@ $7 per share 3000 shares@$6 per share 2016: FULL YEAR Treasury Stock 110,500 Cash 110,500 4. On September 30, 2016, Wildcat granted incentive compensation to executives in the form of 10,000 shares of Restricted Stock with a fair value of $9 per share. The restricted stock is scheduled to vest on September 30, 2017 22,500 SEPT. 20, 2016 Incentlve Comp expense APIC-options 22,500 5. On July 1, 2016, Wildcat purchased a new, larger building for its primary operations by making a cash down payment of $200,000 and financing the remainder by issuing a $2,000,000 zero-interest bearing note from its revolving line of credit. Based on the interest rate implicit in its line of credit, the present value of the note payable at the time of issuance was $1,600,000. The note carries a 10 year maturity, coming due on July 1, 2026 JULY1,2016 Building-New 1,800,000 400,000 Discount on Notes Payable Notes Payable Cash 2,000,000 200,000 45,000 DEC 31st, 2016 Depreciation Expense Accumulated Depreciation-new building 45,000 Interest Expense- N/P 20,000 Discount on N/P 20,000 6 6. August 31, 2016, Wildcat completed the sale of its old building for $600,000 in cash. AUGUST 31st, 20 Cash 600,000 485,000 315,000 Accumulated Depreciation-Old Building Loss on Sale Building-Old 1,400,000 7. On March 31, 2016, Wildcat sold all ofits equipment based on a decision to rent the equipment rather than own it. The equipment was sold for $360,000 in cash. On the same date, Wildcat entered into an agreement with Sun Company to lease equipment for $80,000 per year over a 3 year lease term. At the time of the lease agreement, the estimated fair value of the equipment was $360,000 and the expected useful life was 8 years. Lease payments are due annually at the beginning of the lease term with the first payment made on March 31, 2016. Wildcat's technical accountants have determined that the terms of the lease constitute atransfer ofthe rights and rewards of ownership to wildcat, wildcat's incremental borrowing rate is 10%. 360,000 185,000 MARCH 31st, 201 Cash Accumulated Depreciation-Equipment 520,000 Equipment Gain on Sale of Equipment 25,000 218,843 80,000 54,711 10,413 Right of Use Asset Lease Liability Amortization Expense Interest Expense-Lease 218,843 80,000 54,711 10,413 Lease Liability Cash ROU Asset Interest Payable-Lease 2016 TRANSACTIONS AND BALANCE C Working Capital Accruals (except dividends) Purch of Building December 31, 2015 Restricted Stock Grant Depreciation ASSETS Current assets Cash Accounts receivable Inventory $ 462,065 15,785 220,010 697,860 22,500 200 Total current assets Property, plant &equip. Building Less: Accumulated depreciation (Building) Equipment Less: Accumulated depreciation (Equipment) Right-of-use Asset Less: Accumulated Amortization (ROU Asset) 45,000 (45,000) 1,400,000 (485,000) 520,000 (185,000) 1,800,000 185,000 Total property, plant & equipment Total assets $ 1,250,000 $ 1,947,860 LIABILITIES Current liabilities Accounts Payable Interest Payable 106,190 Long-term liabilities Notes Payable Less: Discount on Notes Payable Lease Liability 2,000,000 Total liabilities 106,190 STOCKHOLDERS' EQUITY Common Stock, $1 par APIC Treasury Stock Retained eamings 61,000 1,600,000 (200,000) 380,670 $ 1,841,670 $ 1,947,860 22,500 Total stockholders' equity Total Liabilities and equity $185,000 $ 22,500 $ 22,500 Assets Liab and Equity$ Edit Check $ 1,600,000 $ 1,600,000 $185,000 CHANGES -SEE TICKMARK REFERENCES FOR DETAIL Total 12/31/16 after adjustments Sale of Building Note Amortization Sale of Equipment Lease of Equipment Share Repurchases December 31 2016 Change Edit Check 445,285 7,840 225,290 $ (146,715.00) $7,840.00 $225,290.00 600,000 360,000 (80,000) (110,500) $ 1,054,065 907,350 23,625 445,300 $ 1,376,275 15,785 S 220,010 $ 1,870,000 $ (45,000) 1,800,000 45,000) S 1,400,000) 485,000 25,000 400,000 440,000 520,000) 185,000 218,843 (520,000) 54,711 (54,711) $(54,710.80) 218,843 $273,554 (54,711) 218,843 (54,711) $ 1,919,132 3,295,407 $ 106,190 10,413 $(18,065.00) 88,125 10,413 (18,065) 10,413 $ 2,020,000 $(20,000.00) $40,000.00 $592,686.40 20,000 20 $2,000,000 S 2,000,000 $ 420,000) $ (380,000)S 138,843 $ 1,857,38 (380,000) 138,843 315, $ (453,843) (218,843) 80,000 $ 61,000 S 1,622,500 $(310,500) S 380,670.00 61,000 $ 1,622,500 (310,500S 65,026 $ 1,438,026 $ 3,295,407 22,500 (110,500) (315,644) (110,500) $ (315,644.04) $(315,000 83,843 (80,000(110,500)S 3,333,703 $(315,000 (218,843)S 90,413(110,500)S 3,016,430 $ 302, 686 (170,413) $ 317,273

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts