Question: Could someone please check my work? Let C (K, t ) be The cost of a call opplor To purchase one shore of stock

Could someone please check my work?

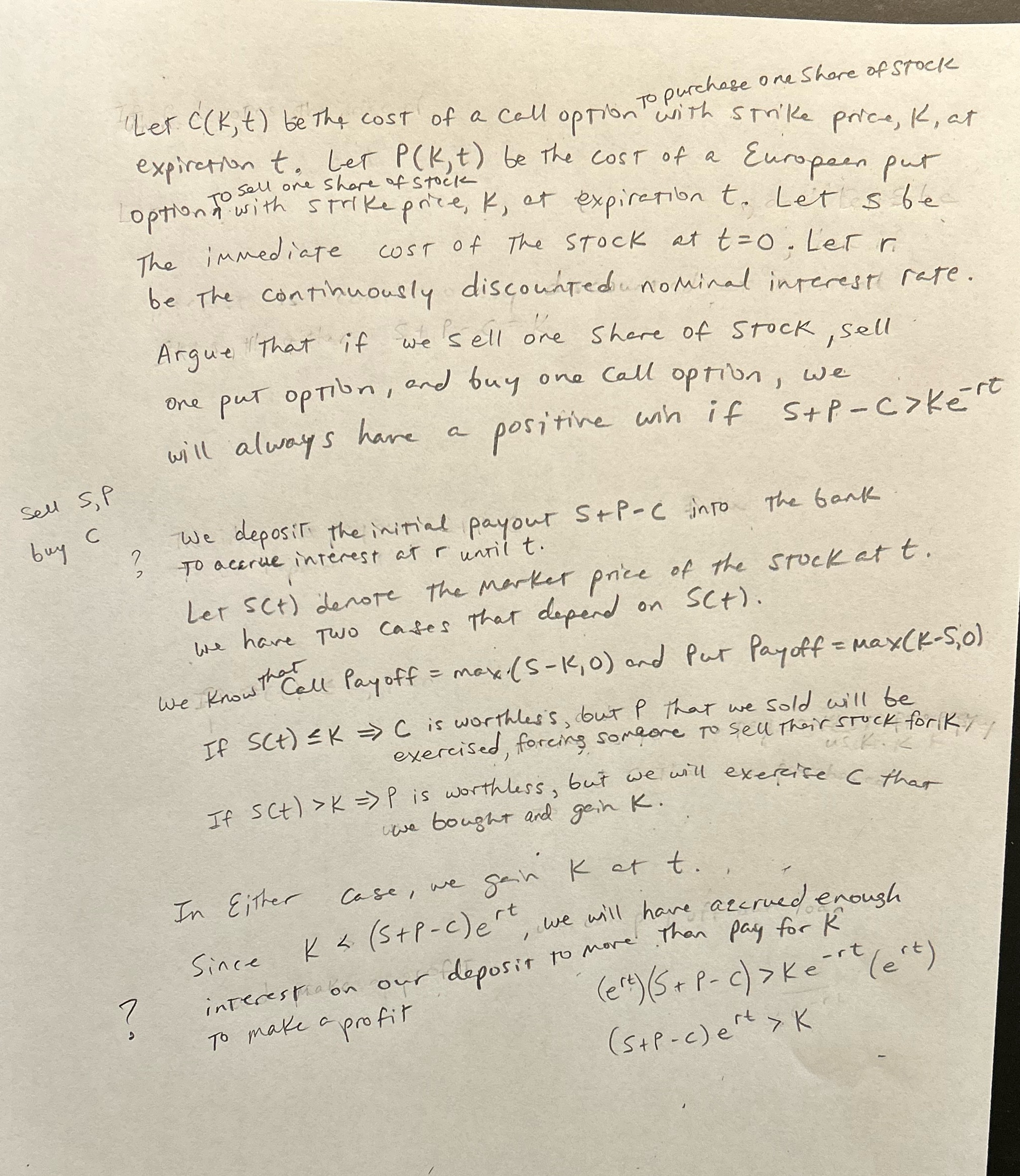

Let C (K, t ) be The cost of a call opplor To purchase one shore of stock " with strike price , K , at expiration to Let P (K, t ) be The cost of a European put option To sell one share of stock a with strike price, K, at expiration t. Let's te The immediate cost of The stock at t= 0. LeFri be The continuously discounted nominal interest rate. Argue That if we sell one share of Stock, sell one put option , and buy one call option, we will always have a positive win if s+p- coker sell S , P buy C We deposit the initial payout STP-C into The bank To accrue interest at r until t. Ler SCt) denote the market price of the stock at t. we have Two cases that depend on SCT) . We Know ? Call Payoff = max (S-k, 0) and Put Payoff = Max (K-S,o) If SCt ) = K => C is worthles's, but P that we sold will be exercised, forcing someone to sell their stuck forlky USK . If SCt ) > K = > P is worthless, but we will exercise ( that iwe bought and gein K . In Either case, we gain K at t. Since K ke -" (ert ) To make a profit ( S+ p - c ) ert > k

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts