Question: Could you please provide the answer with formula and step-by-step processThanks a lot Consider a European call option on a non-dividend paying stock. The current

Could you please provide the answer with formula and step-by-step processThanks a lot

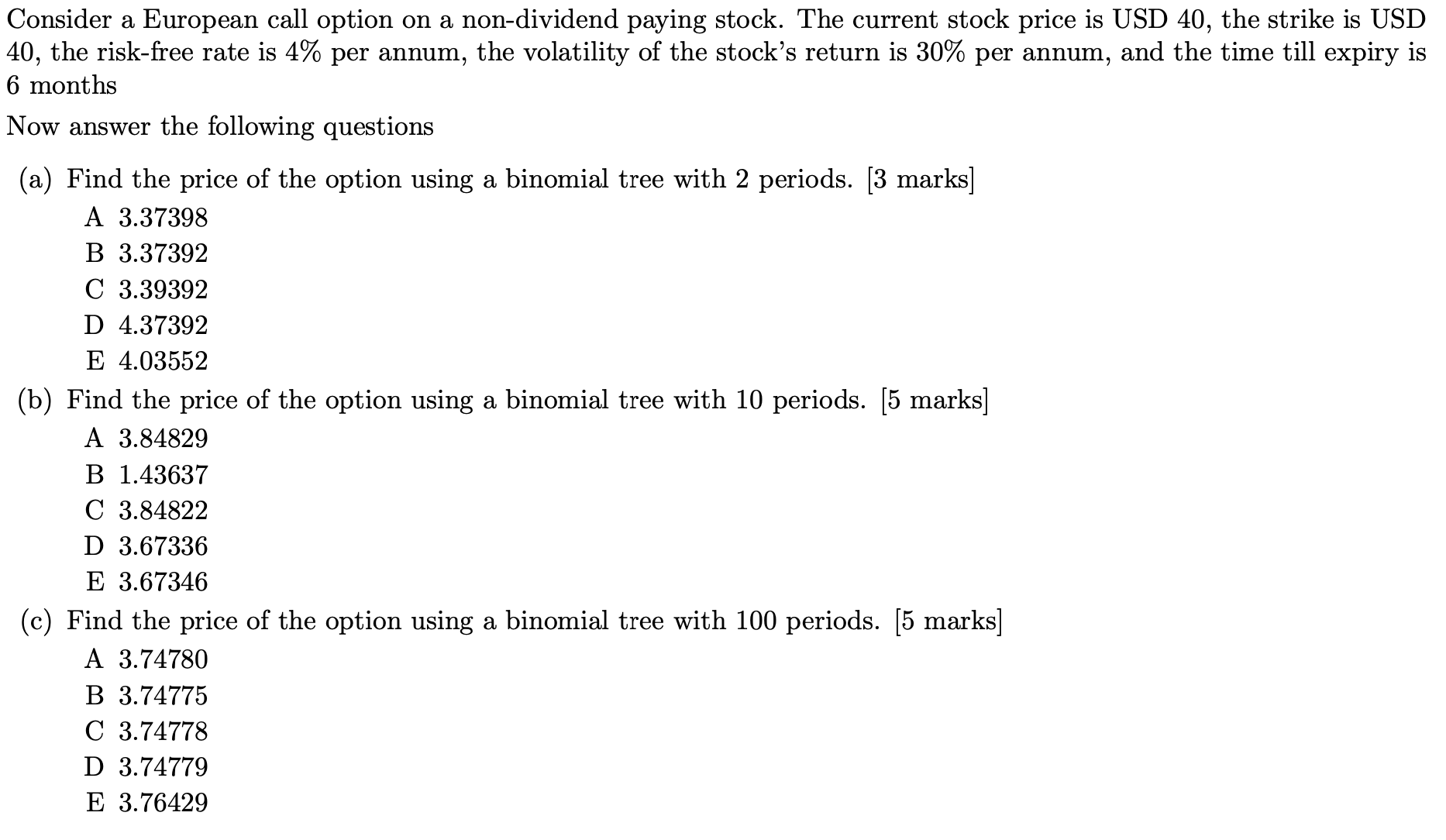

Consider a European call option on a non-dividend paying stock. The current stock price is USD 40 , the strike is USD 40 , the risk-free rate is 4% per annum, the volatility of the stock's return is 30% per annum, and the time till expiry is 6 months Now answer the following questions (a) Find the price of the option using a binomial tree with 2 periods. [3 marks] A 3.37398 B 3.37392 C 3.39392 D 4.37392 E 4.03552 (b) Find the price of the option using a binomial tree with 10 periods. [5 marks] A 3.84829 B 1.43637 C 3.84822 D 3.67336 E 3.67346 (c) Find the price of the option using a binomial tree with 100 periods. [5 marks] A 3.74780 B 3.74775 C 3.74778 D 3.74779 E 3.76429

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts