Question: (d) How would you hedge a long position in the note against relatively large parallel shifts in the yield curve using the two following bonds

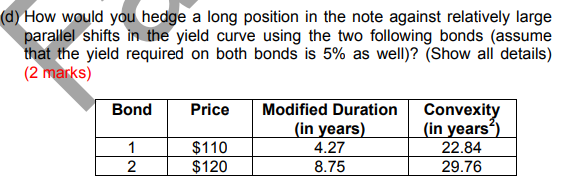

(d) How would you hedge a long position in the note against relatively large parallel shifts in the yield curve using the two following bonds (assume that the yield required on both bonds is 5% as well)? (Show all details) (2 marks) Bond Price Modified Duration Convexity (in years) (in years 1 $110 4.27 22.84 2 $120 8.75 29.76

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock