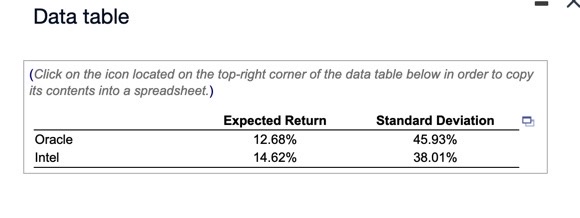

Question: Data table (Click on the icon located on the top-right corner of the data table below in order to copy its contents into a spreadsheet.)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts