Question: Dear Tutor, Please answer the following question. In relation to transactions in a public company, whether it is about the redemption of preference shares, reduction

Dear Tutor,

Please answer the following question.

In relation to transactions in a public company, whether it is about the redemption of preference shares, reduction of share capital, financial assistance, or share buyback, the company is required to satisfy its solvency test.

Discuss TWO (2) provisions of the Companies Act 2016 which provide conditions of the solvency test. (40 marks)

The answer should be from Malaysia's Companies Act 2016 and the section has been given as per below. The link given as per below

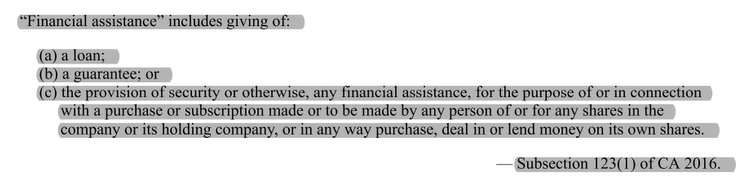

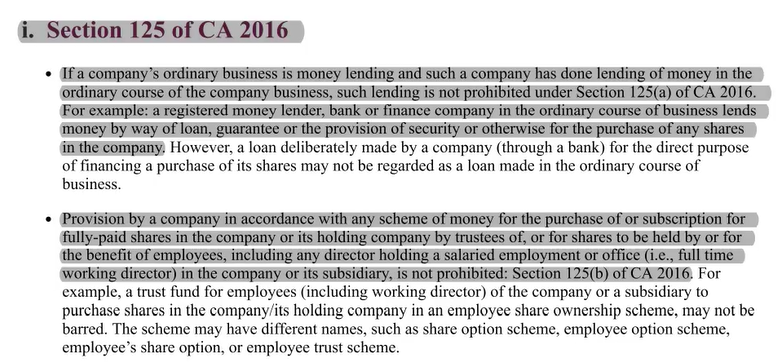

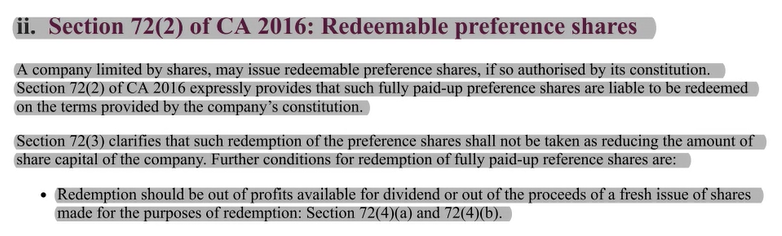

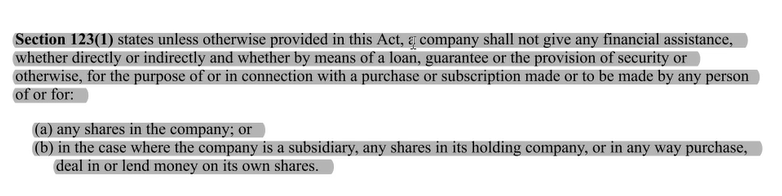

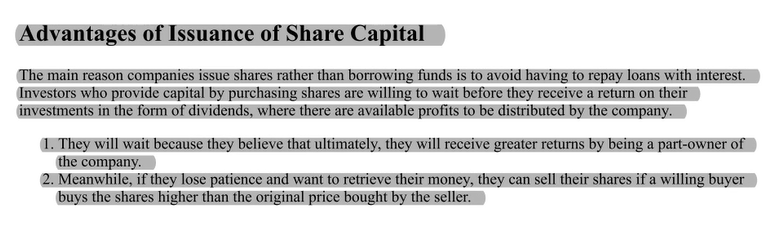

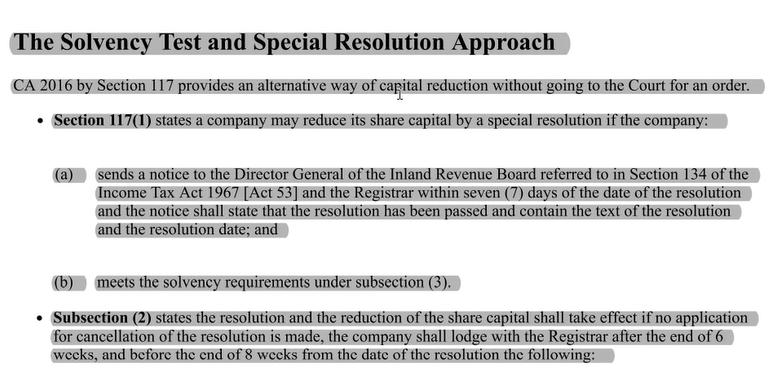

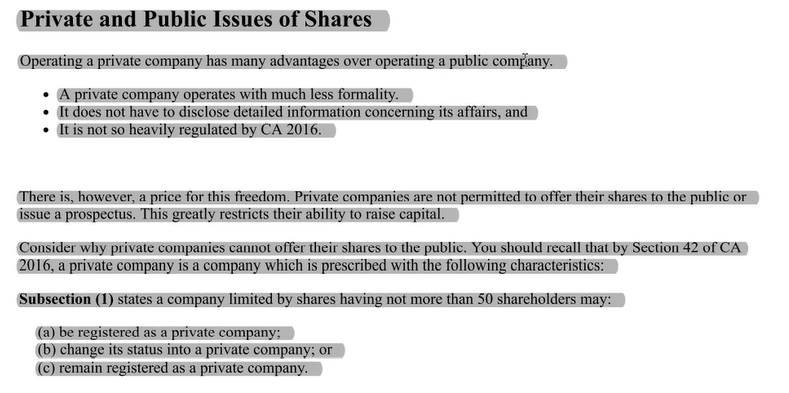

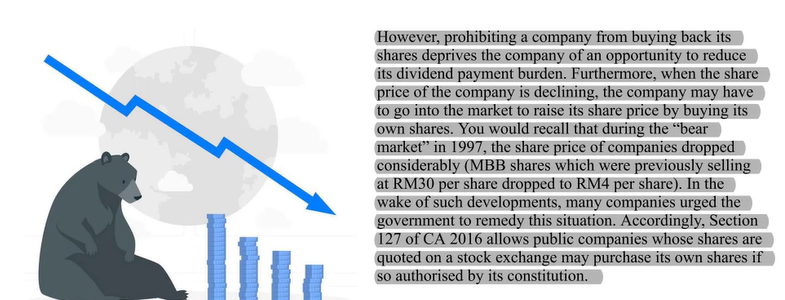

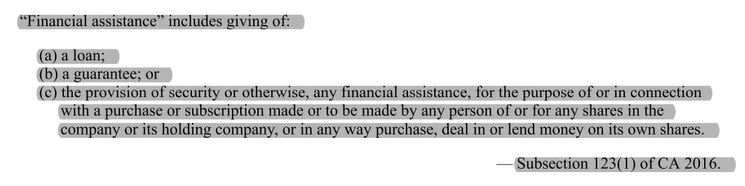

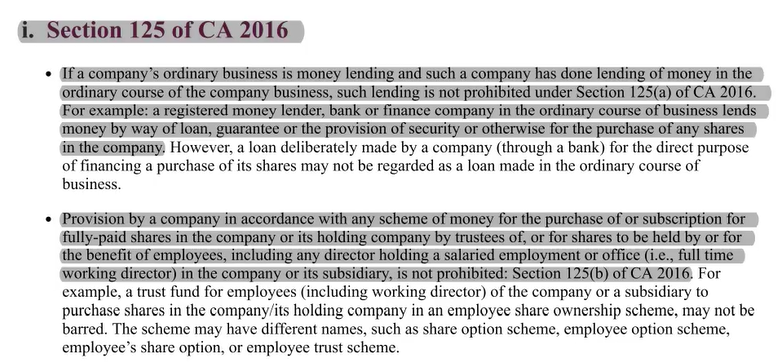

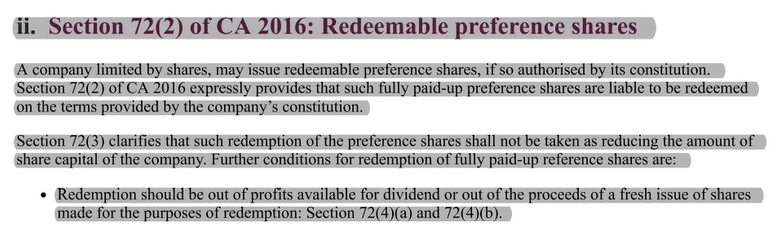

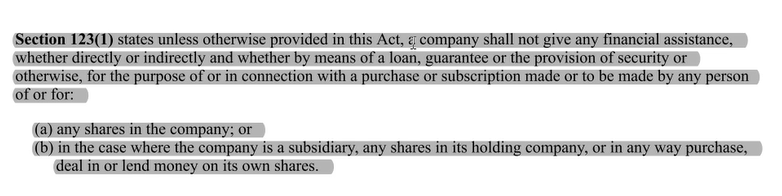

Advantages of Issuance of Share Capital The main reason companies issue shares rather than borrowing funds is to avoid having to repay loans with interest. Investors who provide capital by purchasing shares are willing to wait before they receive a return on their investments in the form of dividends, where there are available profits to be distributed by the company. 1. They will wait because they believe that ultimately, they will receive greater returns by being a part-owner of the company. 2. Meanwhile, if they lose patience and want to retrieve their money, they can sell their shares if a willing buyer buys the shares higher than the original price bought by the seller.The Solvency Test and Special Resolution Approach CA 2016 by Section 117 provides an alternative way of capital reduction without going to the Court for an order. . Section 117(1) states a company may reduce its share capital by a special resolution if the company: (a) sends a notice to the Director General of the Inland Revenue Board referred to in Section 134 of the Income Tax Act 1967 [Act 53] and the Registrar within seven (7) days of the date of the resolution and the notice shall state that the resolution has been passed and contain the text of the resolution and the resolution date; and (b) meets the solvency requirements under subsection (3). . Subsection (2) states the resolution and the reduction of the share capital shall take effect if no application for cancellation of the resolution is made, the company shall lodge with the Registrar after the end of 6 weeks, and before the end of 8 weeks from the date of the resolution the following:Private and Public Issues of Shares Operating a private company has many advantages over operating a public company. . A private company operates with much less formality. . It does not have to disclose detailed information concerning its affairs, and . It is not so heavily regulated by CA 2016. There is, however, a price for this freedom. Private companies are not permitted to offer their shares to the public or issue a prospectus. This greatly restricts their ability to raise capital. Consider why private companies cannot offer their shares to the public. You should recall that by Section 42 of CA 2016, a private company is a company which is prescribed with the following characteristics: Subsection (1) states a company limited by shares having not more than 50 shareholders may: (a) be registered as a private company; (b) change its status into a private company; or (c) remain registered as a private company.Purchase of Own Shares (Share buyback) for Listed Companies You read that the law does provide for the reduction of capital in a few circumstances. The law also prohibits a company from purchasing its own shares (also known as buyback of shares). The law prohibits the buyback of shares as this may amount to a reduction of capital. Although the general rule is that a company is prohibited from purchasing its own shares because it amounts to a reduction of capital in the company. However, by the time you have read this section, you will be able to describe how a company can buy back its own shares, if it is made in good faith and in the interests of the company.Self-purchase of Shares Companies limited by shares are prohibited from buying their own shares or to finance such share purchases. The reason is that, if a company is allowed to buy back its own shares, then this may amount to a reduction of capital without the court's consent. Nor may the company do it indirectly by providing any financial assistance, whether directly or indirectly to any person to purchase or subscribe for any shares in the company or shares of its holding company (if any): Section 123 of CA 2016. Contravention of this provision is an offence and shall, on conviction, be liable to a fine not exceeding RM3.0 million or imprisonment for a term not exceeding 5 years or both.However, prohibiting a company from buying back its shares deprives the company of an opportunity to reduce its dividend payment burden. Furthermore, when the share price of the company is declining, the company may have to go into the market to raise its share price by buying its own shares. You would recall that during the "bear market" in 1997, the share price of companies dropped considerably (MBB shares which were previously selling at RM30 per share dropped to RM4 per share). In the wake of such developments, many companies urged the government to remedy this situation. Accordingly, Section 127 of CA 2016 allows public companies whose shares are quoted on a stock exchange may purchase its own shares if so authorised by its constitution."Financial assistance" includes giving of: (a) a loan; (b) a guarantee; or (c) the provision of security or otherwise, any financial assistance, for the purpose of or in connection with a purchase or subscription made or to be made by any person of or for any shares in the company or its holding company, or in any way purchase, deal in or lend money on its own shares. Subsection 123(1) of CA 2016.i. Section 125 of CA 2016 . If a company's ordinary business is money lending and such a company has done lending of money in the ordinary course of the company business, such lending is not prohibited under Section 125(a) of CA 2016. For example: a registered money lender, bank or finance company in the ordinary course of business lends money by way of loan, guarantee or the provision of security or otherwise for the purchase of any shares in the company. However, a loan deliberately made by a company (through a bank) for the direct purpose of financing a purchase of its shares may not be regarded as a loan made in the ordinary course of business. . Provision by a company in accordance with any scheme of money for the purchase of or subscription for fully-paid shares in the company or its holding company by trustees of, or for shares to be held by or for the benefit of employees, including any director holding a salaried employment or office (i.e., full time working director) in the company or its subsidiary, is not prohibited: Section 125(b) of CA 2016. For example, a trust fund for employees (including working director) of the company or a subsidiary to purchase shares in the company/its holding company in an employee share ownership scheme, may not be barred. The scheme may have different names, such as share option scheme, employee option scheme, employee's share option, or employee trust scheme.ii. Section 72(2) of CA 2016: Redeemable preference shares A company limited by shares, may issue redeemable preference shares, if so authorised by its constitution. Section 72(2) of CA 2016 expressly provides that such fully paid-up preference shares are liable to be redeemed on the terms provided by the company's constitution. Section 72(3) clarifies that such redemption of the preference shares shall not be taken as reducing the amount of share capital of the company. Further conditions for redemption of fully paid-up reference shares are: . Redemption should be out of profits available for dividend or out of the proceeds of a fresh issue of shares made for the purposes of redemption: Section 72(4)(a) and 72(4)(b).Section 123(1) states unless otherwise provided in this Act, a company shall not give any financial assistance, whether directly or indirectly and whether by means of a loan, guarantee or the provision of security or otherwise, for the purpose of or in connection with a purchase or subscription made or to be made by any person of or for: (a) any shares in the company; or (b) in the case where the company is a subsidiary, any shares in its holding company, or in any way purchase, deal in or lend money on its own shares

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts