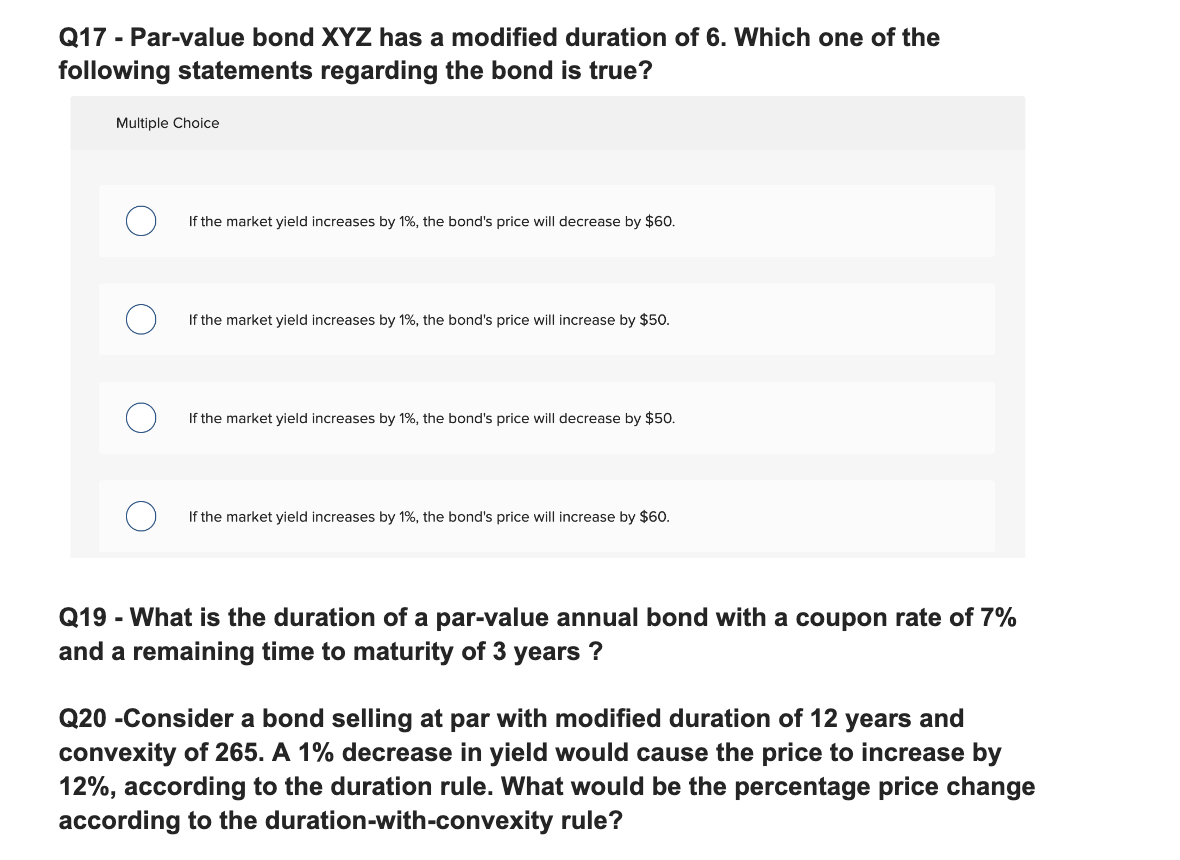

Question: Dear tutor , Please help to solve this problem. Please provide me the correct calculation. Best regards, Q17 - Par-value bond XYZ has a modified

Dear tutor ,

Please help to solve this problem. Please provide me the correct calculation.

Best regards,

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock