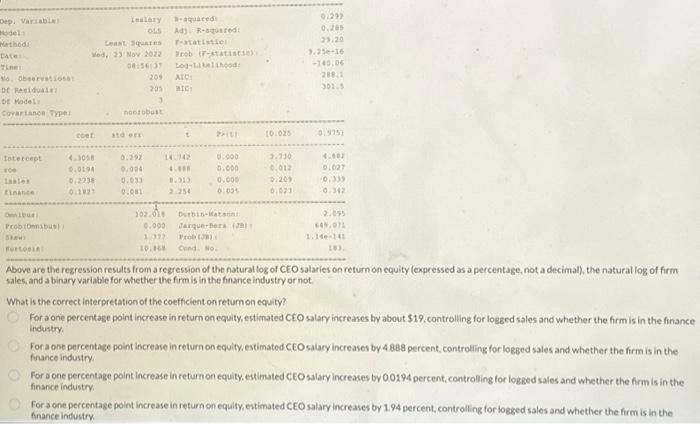

Question: Dep. Variable: Model: Method: Date: Time: No. Observations: Df Residuals: Df Model: Covariance Type: Intercept roe lsales. finance Omnibus: Prob (Omnibus): Skew: Kurtosis: Least Squares

Dep. Variable: Model: Method: Date: Time: No. Observations: Df Residuals: Df Model: Covariance Type: Intercept roe lsales. finance Omnibus: Prob (Omnibus): Skew: Kurtosis: Least Squares Wed, 23 Nov 2022 08:56:37 coef lsalary R-squared: OLS 4.3058 0.0194 0.2738 0.1827 nonrobust std err 209 205 3 0.292 0.004 0.033 0.081 Adj. R-squared: F-statistic: Prob (F-statistic): Log-Likelihood: AIC: BIC: 14.742 4.888 8.313 2.254 P>ltl 0.000 0.000 0.000 0.025 102.018 Durbin-Watson: 0.000 Jarque-Bera (JB): 1.777 10.868 Prob (JB): Cond. No. [0.025 3.730 0.012 0.209 0.023 0.299 0.289 29.20 9.25e-16 -140.06 288.1 301.5 0.975] 4.882 0.027 0.339 0.342 ======= 2.095 649.071 1.14e-141 183. Above are the regression results from a regression of the natural log of CEO salaries on return on equity (expressed as a percentage, not a decimal), the natural log of firm sales, and a binary variable for whether the firm is in the finance industry or not. What is the correct interpretation of the coefficient on return on equity? For a one percentage point increase in return on equity, estimated CEO salary increases by about $19, controlling for logged sales and whether the firm is in the finance industry, For a one percentage point increase in return on equity, estimated CEO salary increases by 4.888 percent, controlling for logged sales and whether the firm is in the finance industry. For a one percentage point increase in return on equity, estimated CEO salary increases by 0.0194 percent, controlling for logged sales and whether the firm is in the finance industry. For a one percentage point increase in return on equity, estimated CEO salary increases by 1.94 percent, controlling for logged sales and whether the firm is in the finance industry.

Above are the regression results from a regression of the natural log of CEO salaries on return on equity (oxpressed as a percentage, not a decimal), the natural log of firm thles, and a binary variable for whether the firm is in the finance industry or not. What is the correct interpretation of the coefficient on return on equity? For a one percentage point increase in return on equity, estimated CEO salary increases by about $19, controlling for logged sales and whether the firm is in the finance induitry. For a one percentage point increase in return on equify, estimated CEO salary increases by 4.888 percent, controlling for logged sales and whether the firm is in the finance industry. For sone percentage point increase in return on equity, estimated cEO salary increases by 00194 percent, controlling for lotged sales and whether the firm is in the finance industry. For s one percentage point increase in return on equity, estimated cEO salary increases by 1.94 percent, controlling for logged sales and whether the firm is in the finance industry