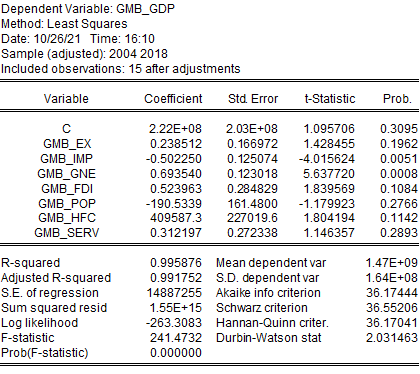

Question: Dependent Variable: GMB_GDP Method: Least Squares Date: 10/26/21 Time: 16:10 Sample (adjusted): 2004 2018 Included observations: 15 after adjustments Variable Coefficient Std. Error t-Statistic Prob.

Dependent Variable: GMB_GDP Method: Least Squares Date: 10/26/21 Time: 16:10 Sample (adjusted): 2004 2018 Included observations: 15 after adjustments Variable Coefficient Std. Error t-Statistic Prob. C 2.22E+08 2.03E+08 1.095706 0.3095 GMB EX 0.238512 0. 166972 1.428455 0.1962 GMB_IMP -0.502250 0. 125074 -4.015624 0.0051 GMB_GNE 0.693540 0. 123018 5.637720 0.0008 GMB FDI 0.523963 0.284829 1.839569 0.1084 GMB_POP -190.5339 161.4800 -1.179923 0.2766 GMB_HFC 409587.3 227019.6 1.804194 0.1142 GMB_SERV 0.312197 0.272338 1.146357 0.2893 R-squared 0.995876 Mean dependent var 1.478+09 Adjusted R-squared 0.991752 S.D. dependent var 1.64E+08 S.E. of regression 14887255 Akaike info criterion 36.17444 Sum squared resid 1.55E+15 Schwarz criterion 36.55206 Log likelihood -263.3083 Hannan-Quinn criter. 36.17041 F-statistic 241.4732 Durbin-Watson stat 2.031463 Prob(F-statistic) 0.000000

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts