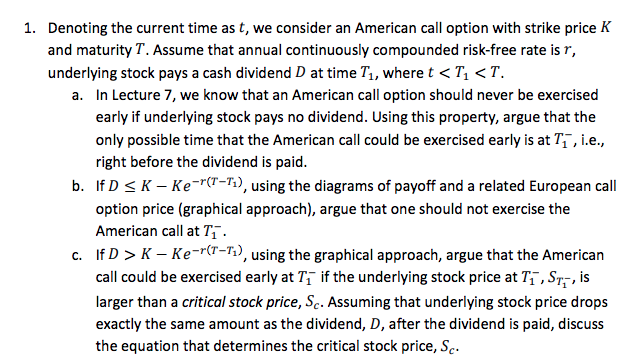

Question: Derivatives: Model-free relationships between Option Prices Denoting the current time as t, we consider an American call option with strike price K and maturity T.

Derivatives: Model-free relationships between Option Prices

Denoting the current time as t, we consider an American call option with strike price K and maturity T. Assume that annual continuously compounded risk-free rate is r, underlying stock pays a cash dividend D at time T1, where t K - Ke-(r-Ti), using the graphical approach, argue that the American call could be exercised early at T1 if the underlying stock price at Ti,STz, i:s larger than a critical stock price, Sc. Assuming that underlying stock price drops exactly the same amount as the dividend, D, after the dividend is paid, discuss the equation that determines the critical stock price, Sc. Denoting the current time as t, we consider an American call option with strike price K and maturity T. Assume that annual continuously compounded risk-free rate is r, underlying stock pays a cash dividend D at time T1, where t K - Ke-(r-Ti), using the graphical approach, argue that the American call could be exercised early at T1 if the underlying stock price at Ti,STz, i:s larger than a critical stock price, Sc. Assuming that underlying stock price drops exactly the same amount as the dividend, D, after the dividend is paid, discuss the equation that determines the critical stock price, Sc

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts