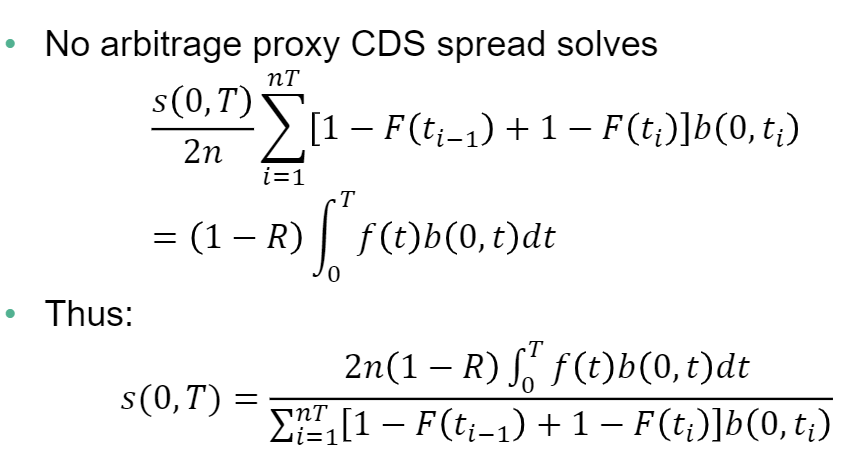

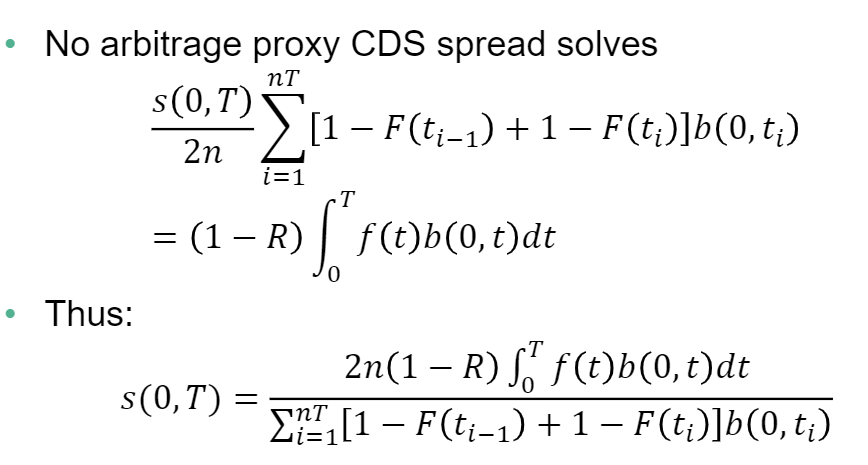

Question: Derive a formula for the no-arbitrage CDS spread with discrete payments per year when the hazard rate and interest rate are constant. You can use

Derive a formula for the no-arbitrage CDS spread with discrete payments per year when the hazard rate and interest rate are constant. You can use the proxy formula

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock