Question: derive duration and simple margin +0.50% - B AR -1.00% Question 4 (2 marks): Given the following information about the floating rate note, derive it's

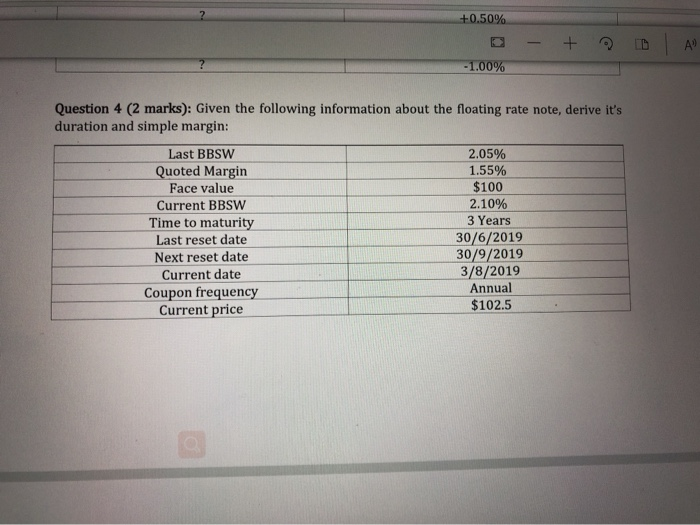

+0.50% - B AR -1.00% Question 4 (2 marks): Given the following information about the floating rate note, derive it's duration and simple margin: Last BBSW 2.05% Quoted Margin 1.55% Face value $100 Current BBSW 2.10% Time to maturity 3 Years Last reset date 30/6/2019 Next reset date 30/9/2019 Current date 3/8/2019 Annual Coupon frequency Current price $102.5 +0.50% - B AR -1.00% Question 4 (2 marks): Given the following information about the floating rate note, derive it's duration and simple margin: Last BBSW 2.05% Quoted Margin 1.55% Face value $100 Current BBSW 2.10% Time to maturity 3 Years Last reset date 30/6/2019 Next reset date 30/9/2019 Current date 3/8/2019 Annual Coupon frequency Current price $102.5

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts