Question: determining the zero rates from bond prices. We are given the prices of four bonds with maturities and coupons shown in Table 2. Determine the

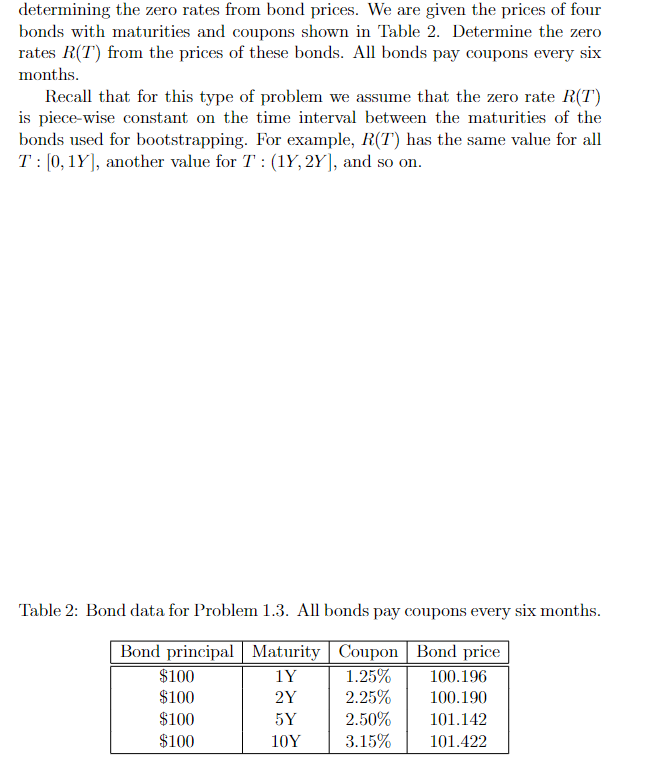

determining the zero rates from bond prices. We are given the prices of four bonds with maturities and coupons shown in Table 2. Determine the zero rates R(T) from the prices of these bonds. All bonds pay coupons every six months. Recall that for this type of problem we assume that the zero rate R(T) is piece-wise constant on the time interval between the maturities of the bonds used for bootstrapping. For example, R(T) has the same value for all T:[0,1Y], another value for T:(1Y,2Y], and so on. Table 2: Bond data for Problem 1.3. All bonds pay coupons every six months. determining the zero rates from bond prices. We are given the prices of four bonds with maturities and coupons shown in Table 2. Determine the zero rates R(T) from the prices of these bonds. All bonds pay coupons every six months. Recall that for this type of problem we assume that the zero rate R(T) is piece-wise constant on the time interval between the maturities of the bonds used for bootstrapping. For example, R(T) has the same value for all T:[0,1Y], another value for T:(1Y,2Y], and so on. Table 2: Bond data for Problem 1.3. All bonds pay coupons every six months

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts