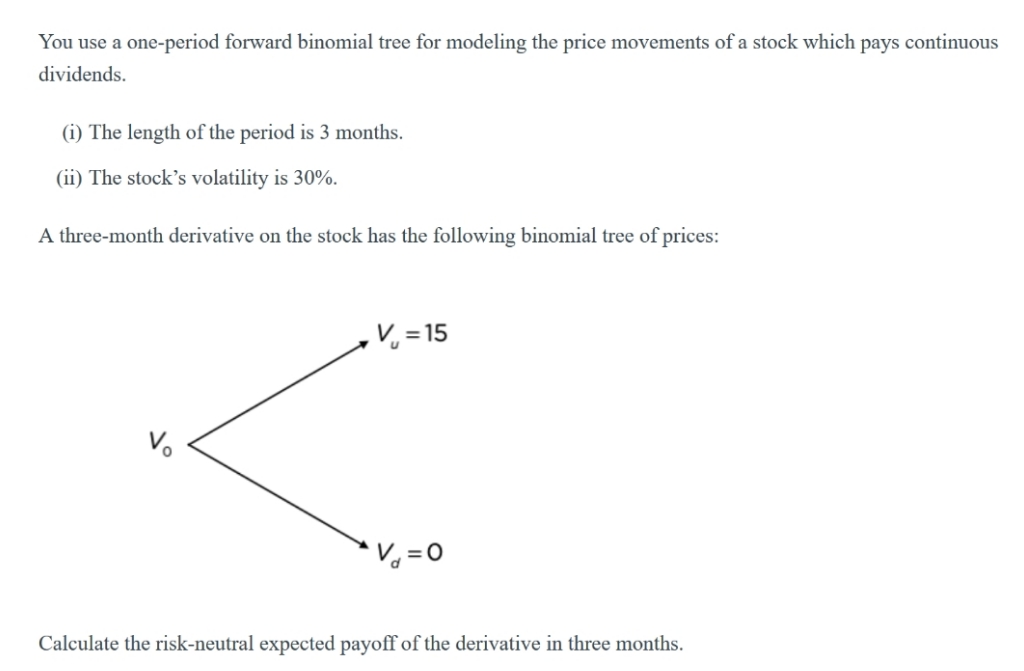

Question: do it fast You use a one-period forward binomial tree for modeling the price movements of a stock which pays continuous dividends. (i) The length

do it fast

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock