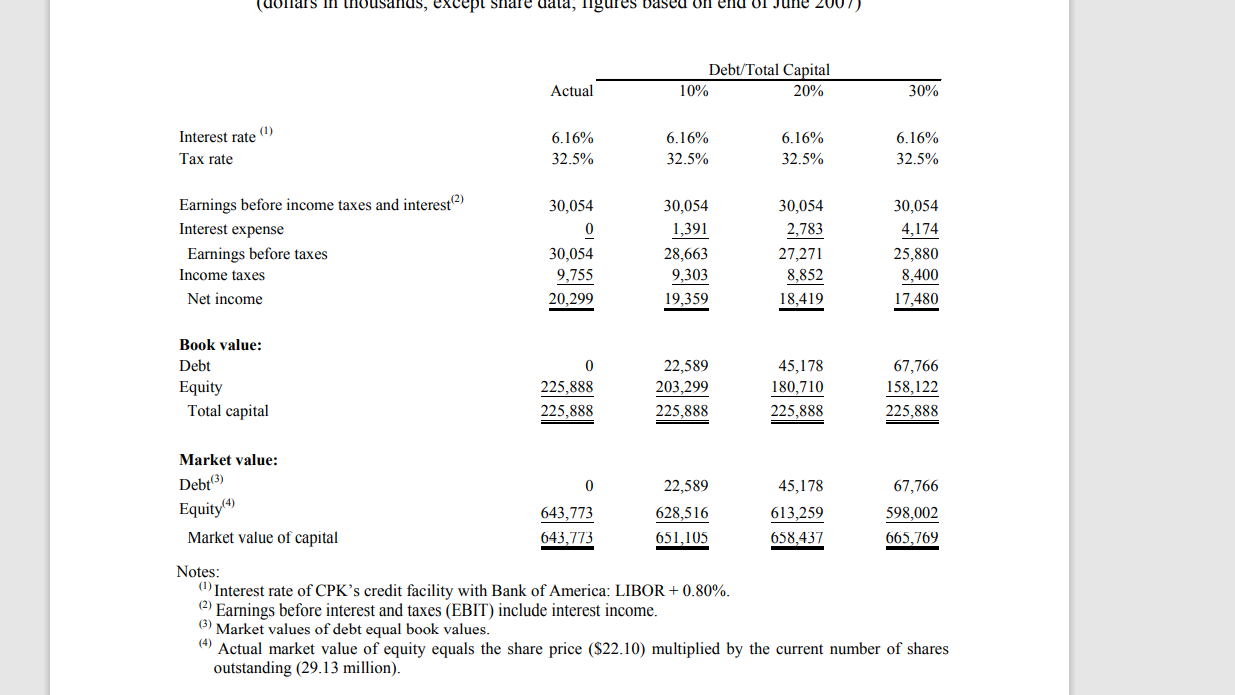

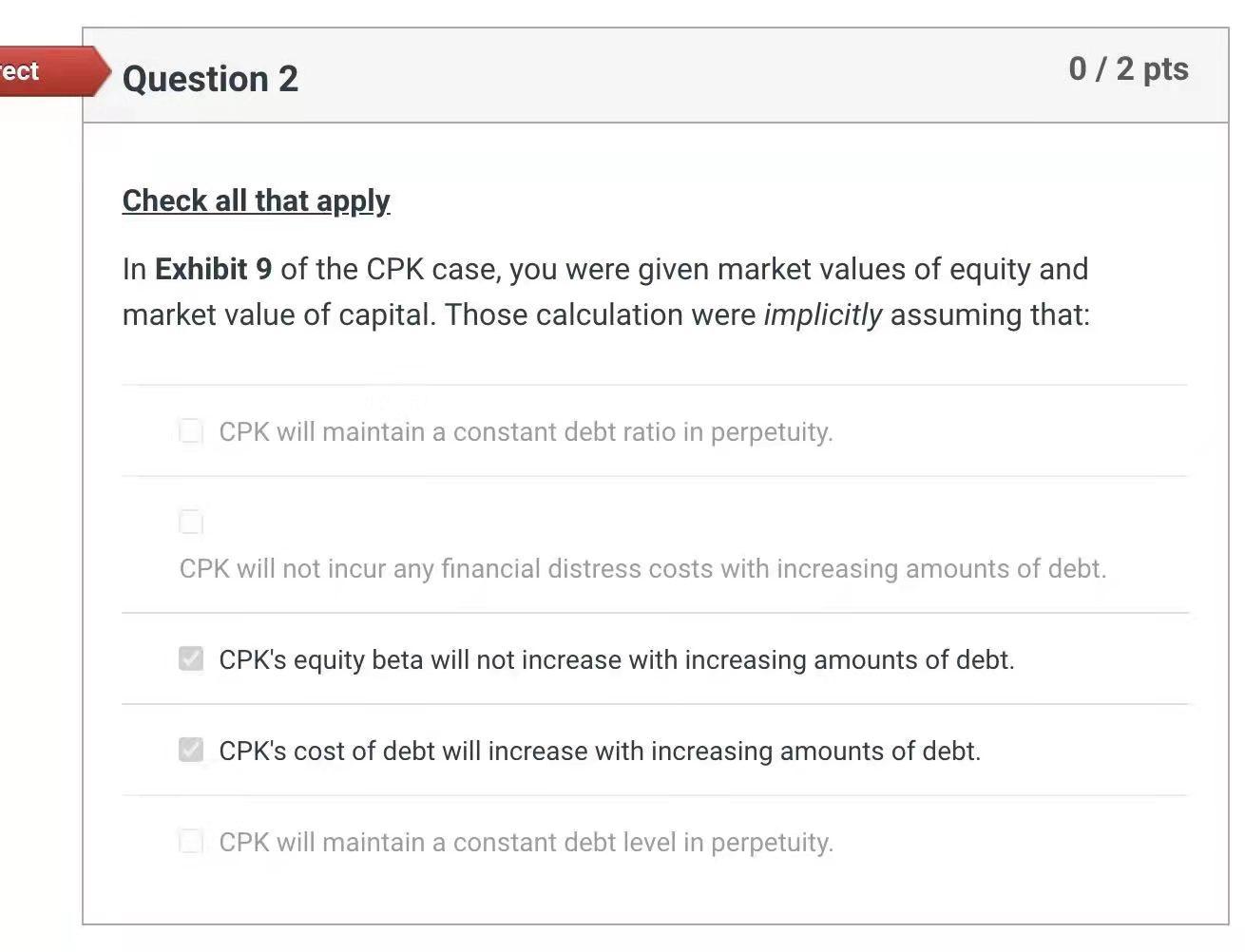

Question: (dollars in thousands, except Snare data, ligures based on end of June 2007) Debt/Total Capital 10% 20% Actual 30% (1) 6.16% Interest rate Tax rate

(dollars in thousands, except Snare data, ligures based on end of June 2007) Debt/Total Capital 10% 20% Actual 30% (1) 6.16% Interest rate Tax rate 6.16% 32.5% 6.16% 32.5% 6.16% 32.5% 32.5% 30,054 0 Earnings before income taxes and interest (2) Interest expense Earnings before taxes Income taxes 30,054 9,755 30,054 1,391 28,663 9,303 19,359 30,054 2,783 27,271 8,852 18,419 30,054 4,174 25,880 8,400 17,480 Net income 20,299 Book value: Debt Equity Total capital 225,888 225,888 22,589 203,299 225,888 45,178 180,710 225,888 67,766 158,122 225,888 Market value: 0 67,766 Debt(3) Equity(4) 643,773 643,773 22,589 628,516 651,105 45,178 613,259 658,437 598,002 665,769 Market value of capital Notes: (1) Interest rate of CPK's credit facility with Bank of America: LIBOR + 0.80%. 2) Earnings before interest and taxes (EBIT) include interest income. ) Market values of debt equal book values. Actual market value of equity equals the share price ($22.10) multiplied by the current number of shares outstanding (29.13 million). (4) Fect Question 2 0/2 pts Check all that apply. In Exhibit 9 of the CPK case, you were given market values of equity and market value of capital. Those calculation were implicitly assuming that: CPK will maintain a constant debt ratio in perpetuity. CPK will not incur any financial distress costs with increasing amounts of debt. CPK's equity beta will not increase with increasing amounts of debt. CPK's cost of debt will increase with increasing amounts of debt. CPK will maintain a constant debt level in perpetuity. (dollars in thousands, except Snare data, ligures based on end of June 2007) Debt/Total Capital 10% 20% Actual 30% (1) 6.16% Interest rate Tax rate 6.16% 32.5% 6.16% 32.5% 6.16% 32.5% 32.5% 30,054 0 Earnings before income taxes and interest (2) Interest expense Earnings before taxes Income taxes 30,054 9,755 30,054 1,391 28,663 9,303 19,359 30,054 2,783 27,271 8,852 18,419 30,054 4,174 25,880 8,400 17,480 Net income 20,299 Book value: Debt Equity Total capital 225,888 225,888 22,589 203,299 225,888 45,178 180,710 225,888 67,766 158,122 225,888 Market value: 0 67,766 Debt(3) Equity(4) 643,773 643,773 22,589 628,516 651,105 45,178 613,259 658,437 598,002 665,769 Market value of capital Notes: (1) Interest rate of CPK's credit facility with Bank of America: LIBOR + 0.80%. 2) Earnings before interest and taxes (EBIT) include interest income. ) Market values of debt equal book values. Actual market value of equity equals the share price ($22.10) multiplied by the current number of shares outstanding (29.13 million). (4) Fect Question 2 0/2 pts Check all that apply. In Exhibit 9 of the CPK case, you were given market values of equity and market value of capital. Those calculation were implicitly assuming that: CPK will maintain a constant debt ratio in perpetuity. CPK will not incur any financial distress costs with increasing amounts of debt. CPK's equity beta will not increase with increasing amounts of debt. CPK's cost of debt will increase with increasing amounts of debt. CPK will maintain a constant debt level in perpetuity

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts