Question: Down Payment: This is the $ amount you will put - down at the time you purchase the building. The bank recommends paying between 1

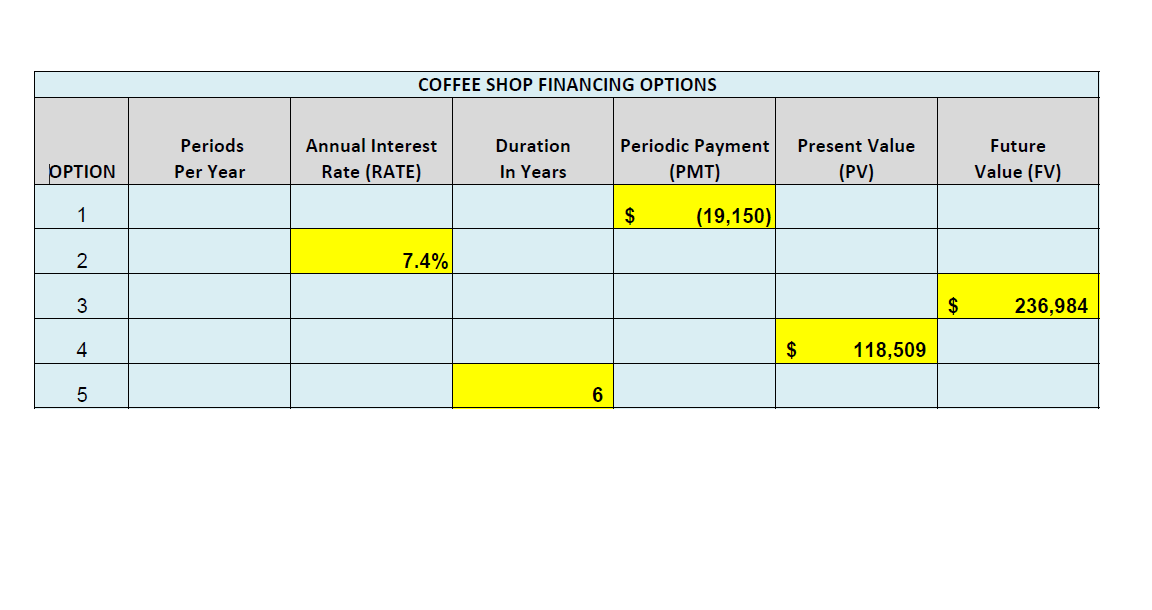

Down Payment: This is the $ amount you will putdown at the time you purchase the building. The bank recommends paying between and up to up front to help keep the pay back amount lower. The difference between the building purchase price and the down payment is the Loan Value Face Value of the loan or the amount you have to pay back to the bank Points: These are the additional bank charges on a loan depending on the customers intent to own the building longterm more than five years or shortterm less than five years Longterm loans will have more points which will lower the interest rate. For reference, onepoint equals of a loan value. So one point, or of a $ loan is $ The worksheet has Points in Column E recorded as regular numbers. You can use Column Es number values to calculate points in another column without changing any of Column Es raw data. Example: E is a value of but when you use it to calculate the points paid to the bank for the loan, you just put a sign after the cell reference of E or E E is but if you use a percentage sign like this: E then becomes Fees: The additional amounts banks sometimes charge the customer for a loan. These amounts vary by bank and loan type. Typical charges include application fees, appraisal fees, credit report fees, etc. Download and save Excel Assignment Raw Data.xlsx as YourLastNameExcel Assignment In the Loan Value column, calculate the Face Value of this loan. The purchase price of the new building is in Cell E In the Monthly Payment column, calculate the monthly payment for this loan amount based on the loan value you just calculated. Use the corresponding loan duration, and nominal interest rate indicated. Assume that the loan is completely paid off at the end of this duration. The number of compounding periods per year is given in cell E In the Actual Amount Borrowed column, calculate the actual amount you will borrow, subtracting the points and fees from the loan value. When banks charge interest which is in most cases it is called the APR of the loanthe annual percentage rate of interest. However, different banks calculate APR in different ways, including or excluding different fees. You will calculate the APR based on the actual amount borrowed Instruction # Use this amount as the present value of the loan, the monthly payment you calculated, and the corresponding loan duration to calculate an actual annual interest rate APR In the Payment with Balloon column, use Column C nominal interest rate, and loan value column G to determine the monthly loan payment if you altered the loan to include an $ balloon payment at the end of the loan. You must put enter the $ balloon payment in Cell Ehint: this is a balloon payment value so its use in the payment function does matter! Periods Per yearAnnual Interest Rate RATEDuration in Years NPERPeriodic Payment PMTPresent Value PVFuture Value FVbegintabularlllllll

hline multicolumncCOFFEE SHOP FINANCING OPTIONS

hline OPTION & Periods Per Year & Annual Interest Rate RATE & Duration In Years & Periodic Payment PMT & Present Value PV & Future Value FV

hline & & & & $ & &

hline & & & & & &

hline & & & & & & $

hline & & & & & $ &

hline & & & & & &

hline

endtabular

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock