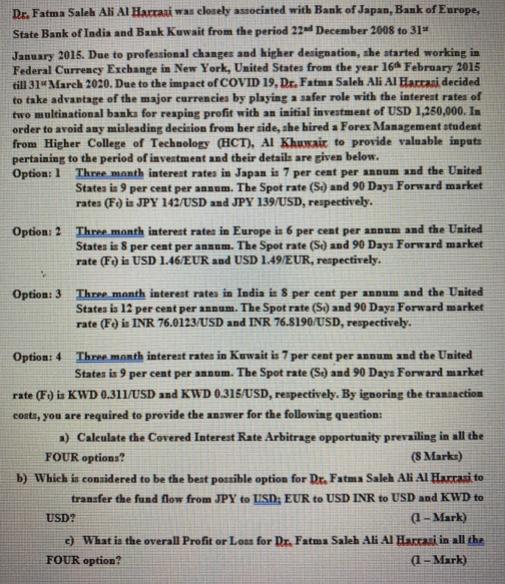

Dr. Fatma Saleh Ali Al Harrai was closely associated with Bank of Japan, Bank of Europe,...

Fantastic news! We've Found the answer you've been seeking!

Question:

Expert Answer:

Related Book For

Posted Date: