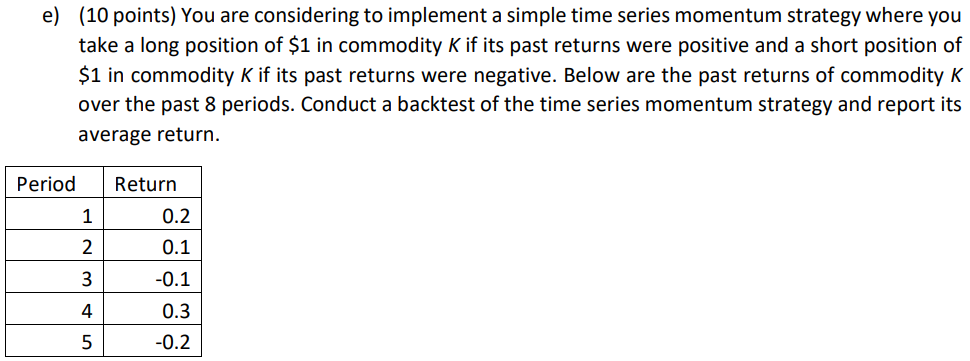

Question: e) (10 points) You are considering to implement a simple time series momentum strategy where you take a long position of $1 in commodity

e) (10 points) You are considering to implement a simple time series momentum strategy where you take a long position of $1 in commodity K if its past returns were positive and a short position of $1 in commodity K if its past returns were negative. Below are the past returns of commodity K over the past 8 periods. Conduct a backtest of the time series momentum strategy and report its average return. Period Return 1 0.2 2 0.1 3 -0.1 4 0.3 5 -0.2

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock