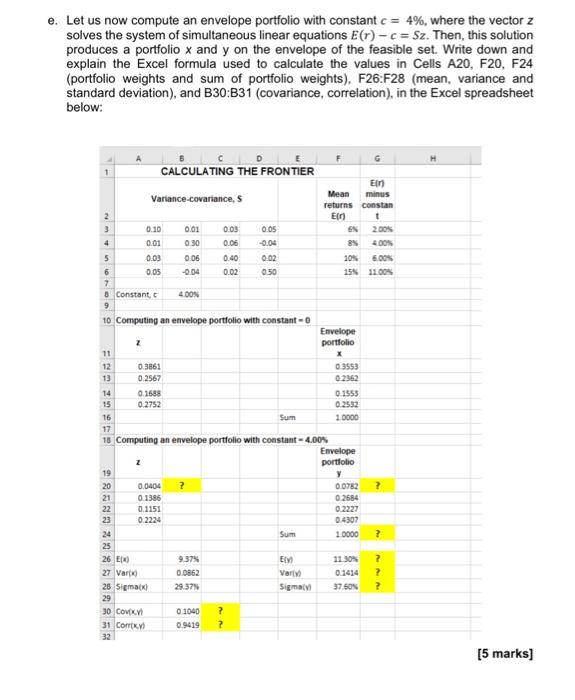

Question: e. Let us now compute an envelope portfolio with constant c = 4%, where the vector z solves the system of simultaneous linear equations E(r)

e. Let us now compute an envelope portfolio with constant c = 4%, where the vector z solves the system of simultaneous linear equations E(r) - c= Sz. Then, this solution produces a portfolio x and y on the envelope of the feasible set. Write down and explain the Excel formula used to calculate the values in Cells A20, F20, F24 (portfolio weights and sum of portfolio weights), F26:F28 (mean, variance and standard deviation), and B30:331 (covariance, correlation), in the Excel spreadsheet below: CALCULATING THE FRONTIER 1 Ein Variance covariance, S Mean minus returns constan 2 Er t 3 0.10 0.01 0.03 0.05 EN 2005 4 0.01 0.30 0.06 -0.04 84 400 5 0.00 0.06 0.40 0.02 109 6.00 6 0.05 -0.04 0.02 0.50 15% 100% 7 8 Constant, 4.00 9 10 Computing an envelope portfolio with constant - Envelope 2 portfolio 11 12 0.3861 03553 13 0.2567 0.2362 14 0.1588 0.1553 15 0.2752 0.2532 16 Sum 10000 17 18 Computing an envelope portfolio with constant - 4,00% Envelope Z portfolio 19 20 0,0404 ? 0.0782 ? 0.1386 0.2684 0.1151 0.2227 23 0.2224 0.4307 Sum 10000 ? SANA NA 26 27 Vart 28 Sigma 9.37 0.0862 29.37 EL Varli Sigma 11 30% 0.1434 37.50N ? ? ? 30 Cox 31 Com 01040 0.9419 ? ? (5 marks] e. Let us now compute an envelope portfolio with constant c = 4%, where the vector z solves the system of simultaneous linear equations E(r) - c= Sz. Then, this solution produces a portfolio x and y on the envelope of the feasible set. Write down and explain the Excel formula used to calculate the values in Cells A20, F20, F24 (portfolio weights and sum of portfolio weights), F26:F28 (mean, variance and standard deviation), and B30:331 (covariance, correlation), in the Excel spreadsheet below: CALCULATING THE FRONTIER 1 Ein Variance covariance, S Mean minus returns constan 2 Er t 3 0.10 0.01 0.03 0.05 EN 2005 4 0.01 0.30 0.06 -0.04 84 400 5 0.00 0.06 0.40 0.02 109 6.00 6 0.05 -0.04 0.02 0.50 15% 100% 7 8 Constant, 4.00 9 10 Computing an envelope portfolio with constant - Envelope 2 portfolio 11 12 0.3861 03553 13 0.2567 0.2362 14 0.1588 0.1553 15 0.2752 0.2532 16 Sum 10000 17 18 Computing an envelope portfolio with constant - 4,00% Envelope Z portfolio 19 20 0,0404 ? 0.0782 ? 0.1386 0.2684 0.1151 0.2227 23 0.2224 0.4307 Sum 10000 ? SANA NA 26 27 Vart 28 Sigma 9.37 0.0862 29.37 EL Varli Sigma 11 30% 0.1434 37.50N ? ? ? 30 Cox 31 Com 01040 0.9419 ? ? (5 marks]

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts