Suppose we form a portfolio invested in Mercedes and BMW stocks. The two stocks are equally weighted

Question:

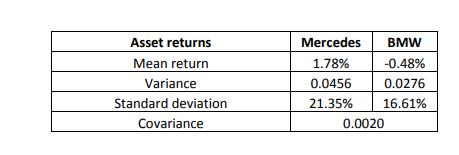

Suppose we form a portfolio invested in Mercedes and BMW stocks. The two stocks are equally weighted in the portfolio. The table below displays each stock’s mean return, variance, and standard deviation, as well as their covariance. Estimate the mean and variance of this portfolio, as well as its standard deviation. Show in detail your calculations.

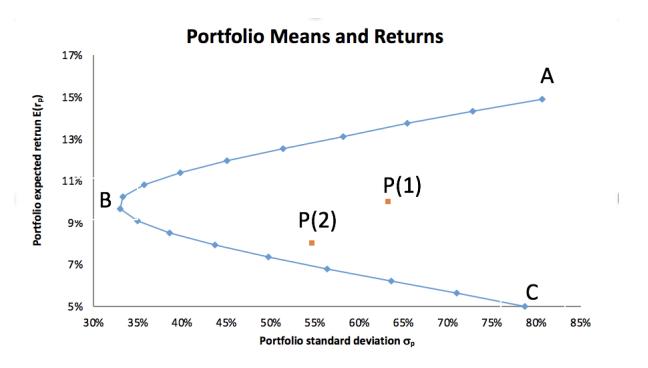

b. The graph below shows the envelope frontier. Based on the graph below do you agree with the statement “Portfolio P(1) and P(2) are two efficient portfolios”? Explain your answer.

c. Explain in detail all five propositions on envelope portfolios.

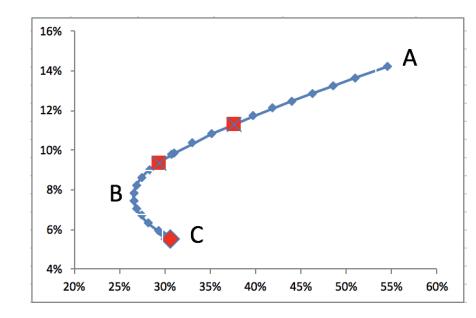

d. Consider two portfolios, x and y, whose convex combinations compose the envelope frontier in the graph below (curve ABC). Also marked, are other portfolios, some of which contain short positions of either x or y. Do you agree with the statement “Every convex combination of any two efficient portfolios is efficient”? Explain your answer.

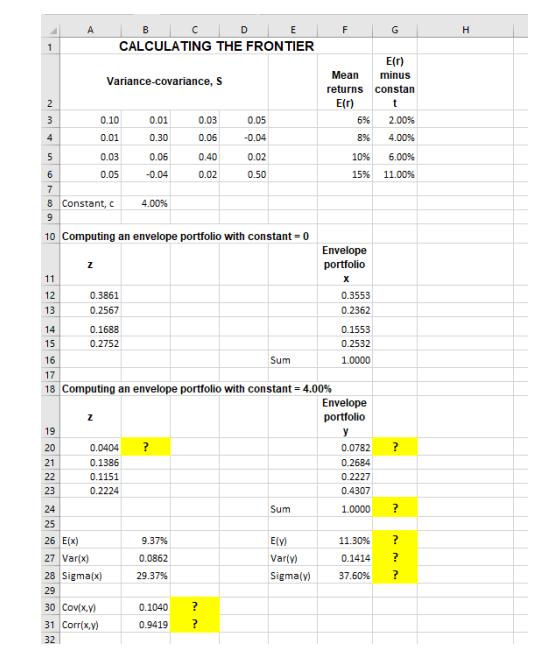

e. Let us now compute an envelope portfolio with constant ???? = 4%, where the vector z solves the system of simultaneous linear equations ????(????) − ???? = ????????. Then, this solution produces a portfolio x and y on the envelope of the feasible set. Write down and explain the Excel formula used to calculate the values in Cells A20, F20, F24 (portfolio weights and sum of portfolio weights), F26:F28 (mean, variance and standard deviation), and B30:B31 (covariance, correlation), in the Excel spreadsheet below:

Expert Answer:

Probability and Random Processes With Applications to Signal Processing and Communications

ISBN: 978-0123869814

2nd edition

Authors: Scott Miller, Donald Childers