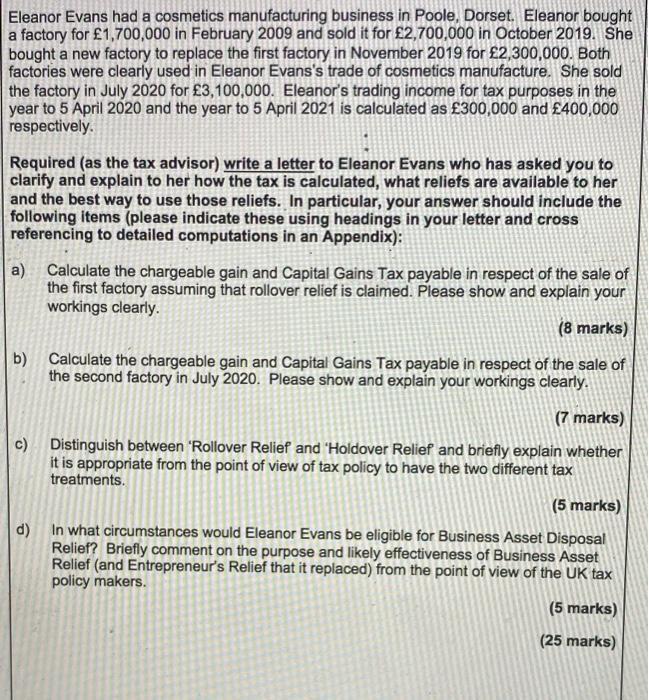

Eleanor Evans had a cosmetics manufacturing business in Poole, Dorset. Eleanor bought factory for 1,700,000 in...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

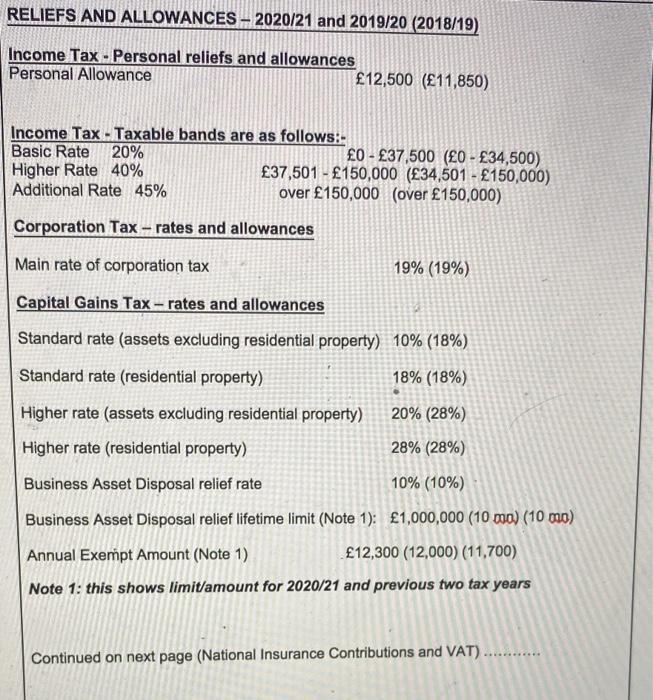

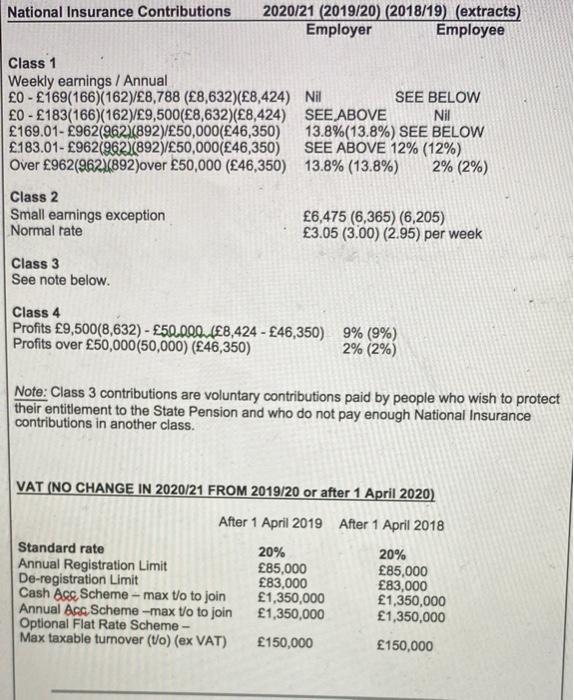

Eleanor Evans had a cosmetics manufacturing business in Poole, Dorset. Eleanor bought factory for £1,700,000 in February 2009 and sold it for £2,700,000 in October 2019. She bought a new factory to replace the first factory in November 2019 for £2,300,000. Both factories were clearly used in Eleanor Evans's trade of cosmetics manufacture. She sold the factory in July 2020 for £3,100,000. Eleanor's trading income for tax purposes in the year to 5 April 2020 and the year to 5 April 2021 is calculated as £300,000 and £400,000 respectively. Required (as the tax advisor) write a letter to Eleanor Evans who has asked you to clarify and explain to her how the tax is calculated, what reliefs are available to her and the best way to use those reliefs. In particular, your answer should include the following items (please indicate these using headings in your letter and cros referencing to detailed computations in an Appendix): a) Calculate the chargeable gain and Capital Gains Tax payable in respect of the sale of the first factory assuming that rollover relief is claimed. Please show and explain your workings clearly. (8 marks) b) Calculate the chargeable gain and Capital Gains Tax payable in respect of the sale of the second factory in July 2020. Please show and explain your workings clearly. (7 marks) c) Distinguish between 'Rollover Relief and "Holdover Relief and briefly explain whether it is appropriate from the point of view of tax policy to have the two different tax treatments. (5 marks) d) In what circumstances would Eleanor Evans be eligible for Business Asset Disposal Relief? Briefly comment on the purpose and likely effectiveness of Business Asset Relief (and Entrepreneur's Relief that it replaced) from the point of view of the UK tax policy makers. (5 marks) (25 marks) RELIEFS AND ALLOWANCES – 2020/21 and 2019/20 (2018/19) Income Tax - Personal reliefs and allowances Personal Allowance £12,500 (£11,850) Income Tax -Taxable bands are as follows:- Basic Rate Higher Rate 40% Additional Rate 45% 20% £0 - £37,500 (£O - £34,500) £37,501 - £150,000 (£34,501 - £150,000) over £150,000 (over £150,000) Corporation Tax- rates and allowances Main rate of corporation tax 19% (19%) Capital Gains Tax-rates and allowances Standard rate (assets excluding residential property) 10% (18%) Standard rate (residential property) 18% (18%) Higher rate (assets excluding residential property) 20% (28%) Higher rate (residential property) 28% (28%) Business Asset Disposal relief rate 10% (10%) Business Asset Disposal relief lifetime limit (Note 1): £1,000,000 (10 mo) (10 mo) Annual Exempt Amount (Note 1) £12,300 (12,000) (11,700) Note 1: this shows limit/amount for 2020/21 and previous two tax years Continued on next page (National Insurance Contributions and VAT) 2020/21 (2019/20) (2018/19) (extracts) Employer National Insurance Contributions Employee Class 1 Weekly earnings / Annual £0 - £169(166)(162)/£8,788 (£8,632)(£8,424) Nil £0 - £183(166)(162)/£9,500(£8,632)(£8,424) SEE ABOVE £169.01- £962(962)(892)/£50,000(£46,350) £183.01- £962(962)(892)/£50,000(£46,350) Over £962(962892)over £50,000 (£46,350) 13.8% (13.8%) SEE BELOW Nil 13.8%(13.8%) SEE BELOW SEE ABOVE 12% (12%) 2% (2%) Class 2 Small earnings exception Normal rate £6,475 (6,365) (6,205) £3.05 (3.00) (2.95) per week Class 3 See note below. Class 4 Profits £9,500(8,632) - £50.000 (£8,424 - £46,350) 9% (9%) Profits over £50,000(50,000) (£46,350) 2% (2%) Note: Class 3 contributions are voluntary contributions paid by people who wish to protect their entitlement to the State Pension and who do not pay enough National Insurance contributions in another class. VAT (NO CHANGE IN 2020/21 FROM 2019/20 or after 1 April 2020) After 1 April 2019 After 1 April 2018 Standard rate Annual Registration Limit De-registration Limit Cash Acc Scheme - max t/o to join Annual Acc Scheme -max t/o to join Optional Flat Rate Scheme - Max taxable turnover (/o) (ex VAT) 20% £85,000 £83,000 £1,350,000 £1,350,000 20% £85,000 £83,000 £1,350,000 £1,350,000 £150,000 £150,000 Eleanor Evans had a cosmetics manufacturing business in Poole, Dorset. Eleanor bought factory for £1,700,000 in February 2009 and sold it for £2,700,000 in October 2019. She bought a new factory to replace the first factory in November 2019 for £2,300,000. Both factories were clearly used in Eleanor Evans's trade of cosmetics manufacture. She sold the factory in July 2020 for £3,100,000. Eleanor's trading income for tax purposes in the year to 5 April 2020 and the year to 5 April 2021 is calculated as £300,000 and £400,000 respectively. Required (as the tax advisor) write a letter to Eleanor Evans who has asked you to clarify and explain to her how the tax is calculated, what reliefs are available to her and the best way to use those reliefs. In particular, your answer should include the following items (please indicate these using headings in your letter and cros referencing to detailed computations in an Appendix): a) Calculate the chargeable gain and Capital Gains Tax payable in respect of the sale of the first factory assuming that rollover relief is claimed. Please show and explain your workings clearly. (8 marks) b) Calculate the chargeable gain and Capital Gains Tax payable in respect of the sale of the second factory in July 2020. Please show and explain your workings clearly. (7 marks) c) Distinguish between 'Rollover Relief and "Holdover Relief and briefly explain whether it is appropriate from the point of view of tax policy to have the two different tax treatments. (5 marks) d) In what circumstances would Eleanor Evans be eligible for Business Asset Disposal Relief? Briefly comment on the purpose and likely effectiveness of Business Asset Relief (and Entrepreneur's Relief that it replaced) from the point of view of the UK tax policy makers. (5 marks) (25 marks) RELIEFS AND ALLOWANCES – 2020/21 and 2019/20 (2018/19) Income Tax - Personal reliefs and allowances Personal Allowance £12,500 (£11,850) Income Tax -Taxable bands are as follows:- Basic Rate Higher Rate 40% Additional Rate 45% 20% £0 - £37,500 (£O - £34,500) £37,501 - £150,000 (£34,501 - £150,000) over £150,000 (over £150,000) Corporation Tax- rates and allowances Main rate of corporation tax 19% (19%) Capital Gains Tax-rates and allowances Standard rate (assets excluding residential property) 10% (18%) Standard rate (residential property) 18% (18%) Higher rate (assets excluding residential property) 20% (28%) Higher rate (residential property) 28% (28%) Business Asset Disposal relief rate 10% (10%) Business Asset Disposal relief lifetime limit (Note 1): £1,000,000 (10 mo) (10 mo) Annual Exempt Amount (Note 1) £12,300 (12,000) (11,700) Note 1: this shows limit/amount for 2020/21 and previous two tax years Continued on next page (National Insurance Contributions and VAT) 2020/21 (2019/20) (2018/19) (extracts) Employer National Insurance Contributions Employee Class 1 Weekly earnings / Annual £0 - £169(166)(162)/£8,788 (£8,632)(£8,424) Nil £0 - £183(166)(162)/£9,500(£8,632)(£8,424) SEE ABOVE £169.01- £962(962)(892)/£50,000(£46,350) £183.01- £962(962)(892)/£50,000(£46,350) Over £962(962892)over £50,000 (£46,350) 13.8% (13.8%) SEE BELOW Nil 13.8%(13.8%) SEE BELOW SEE ABOVE 12% (12%) 2% (2%) Class 2 Small earnings exception Normal rate £6,475 (6,365) (6,205) £3.05 (3.00) (2.95) per week Class 3 See note below. Class 4 Profits £9,500(8,632) - £50.000 (£8,424 - £46,350) 9% (9%) Profits over £50,000(50,000) (£46,350) 2% (2%) Note: Class 3 contributions are voluntary contributions paid by people who wish to protect their entitlement to the State Pension and who do not pay enough National Insurance contributions in another class. VAT (NO CHANGE IN 2020/21 FROM 2019/20 or after 1 April 2020) After 1 April 2019 After 1 April 2018 Standard rate Annual Registration Limit De-registration Limit Cash Acc Scheme - max t/o to join Annual Acc Scheme -max t/o to join Optional Flat Rate Scheme - Max taxable turnover (/o) (ex VAT) 20% £85,000 £83,000 £1,350,000 £1,350,000 20% £85,000 £83,000 £1,350,000 £1,350,000 £150,000 £150,000

Expert Answer:

Answer rating: 100% (QA)

aCALCULATION OF CHARGEABLE GAIN PROCEEDS ON SALE OF FIRST FACTORYA POUND 2700000 COST OF FIRST FACTO... View the full answer

Related Book For

Posted Date:

Students also viewed these organizational behavior questions

-

The proposal should include the following items : - A little background on the situation - The purpose of the model and its objective function - The kinds of data needed as model input (you don't...

-

For 2020 an individual had net income for tax purposes of $196,000 and Division C deductions of $18,000. During 2020 the individual had medical expenses of $7,900 and made charitable donations of...

-

3 1 point Assume that 1 ton of greenhouse gas emissions does $100 of damage 30 years from now. If society has a discount rate of 1 per cent, what is the cost of that damage in today's terms? Give...

-

Exercises 11-16: For the measured quantity, state the set of numbers that most appropriately describes it. Choose from the natural numbers, integers, and rational numbers. Explain your answer....

-

Quinton Corporation produces and sells two types of chili: 1-Alarm and 5-Alarm. Operating performance for the most recent quarter is: Management is puzzled by these results because they spent $...

-

Is charging lower prices for matinees than for evening movies price discriminationcharging different customers different prices for the same goodor are matinees and evening movie viewings different...

-

The helium-filled balloon shown in Fig P9.81 is to be used as a wind-speed indicator. The specific weight of the helium is \(y=0.011 \mathrm{lb} / \mathrm{ft}^{3}\), the weight of the balloon...

-

The balance sheet of MacMillan Management Consulting, Inc., at December 31, 2011, reported the following stockholders' equity: During 2012, MacMillan completed the following selected transactions:...

-

Given a system of 4 processes with a set of constraints described by the following precedence relation: {(P1, P3), (P1, P4), (P2, P4)} The processes access memory locations according to the following...

-

Founded in 1972, the German software business SAP (Systems, Applications, and Products in Data Processing) is known as one of the world leaders in enterprise resource planning software, employing...

-

Environmental laws for vinyl upholstery companies in India and Brazil? Intellectual property laws relating for vinyl upholstery companies in India and Brazil?

-

True Or False A defendant must actively participate in the prosecution for there to be a malicious prosecution case.

-

How does intentional misrepresentation differ from negligent and innocent misrepresentation?

-

What do plaintiffs have to prove in terms of causation?

-

True Or False Wrongful institution of civil proceedings cannot arise out of administrative or bankruptcy proceedings.

-

True Or False A plaintiff is most likely to recover for negligent misrepresentation when the defendant has a pecuniary interest in or makes false statements during a business transaction.

-

In which of these situations does it make sense to say economics predicts people will not internalize an externality, like pollution? (1 point) A. When the transaction costs of trading in rights to...

-

(a) Given a mean free path = 0.4 nm and a mean speed vav = 1.17 105 m/s for the current flow in copper at a temperature of 300 K, calculate the classical value for the resistivity of copper. (b)...

-

Time, cost and quality measured at project completion have been widely used as performance measures for projects. When might this be useful and how is this a limited approach?

-

1. Was the A380 development a project or a programmed? 2. Using the notation of Figure 3.5, how has the development been managed? 3. Suggest what the challenges to the management of this development...

-

Why is there a tendency for individual rather than group projects in particular to spend 90 per cent of their time 90 per cent complete.

-

Describe the steps in attaining state licensure for nurses.

-

How do medical billing and coding specialists keep up-to-date with changes in ICD and CPT?

-

Define and give examples (other than from the table in the text) of fixed, variable, and semivariable costs, along with examples of ways to control the costs in your examples.

Study smarter with the SolutionInn App