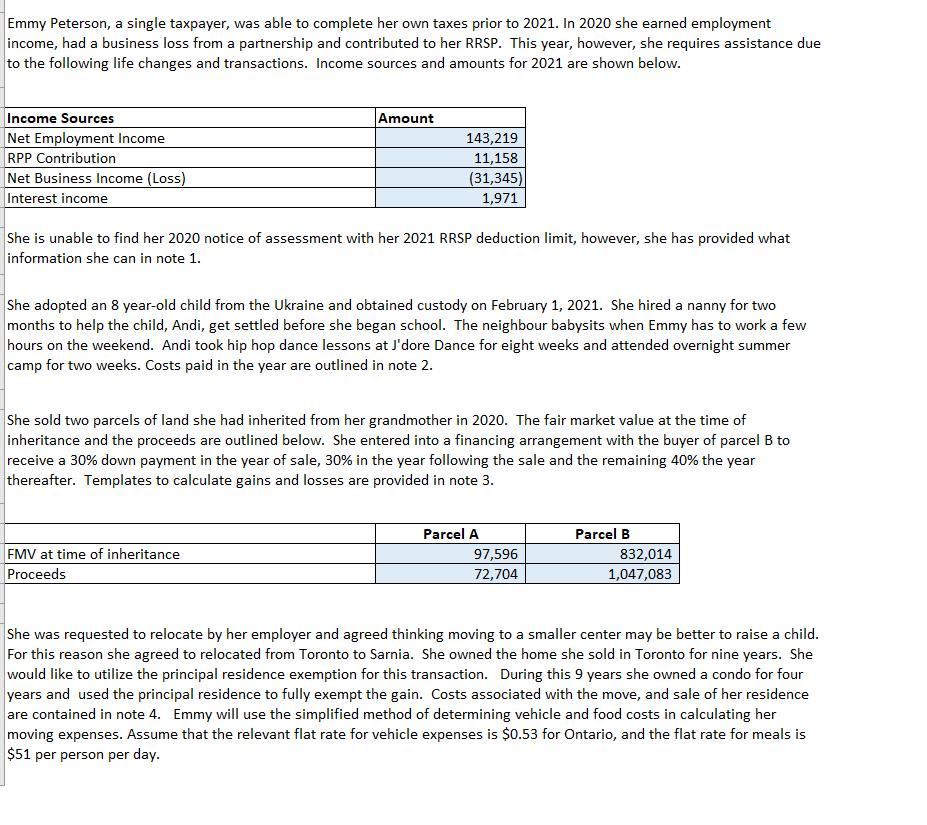

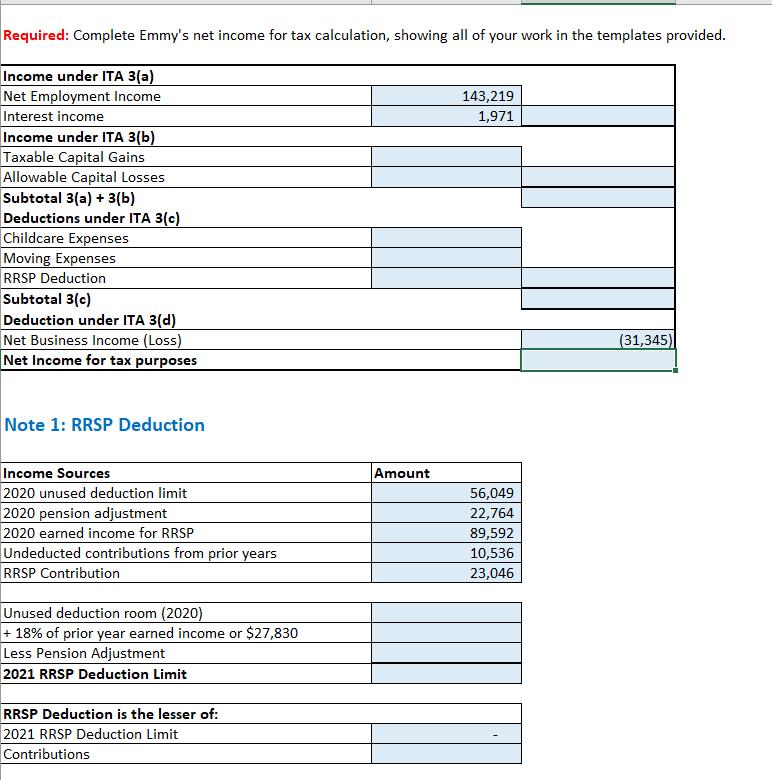

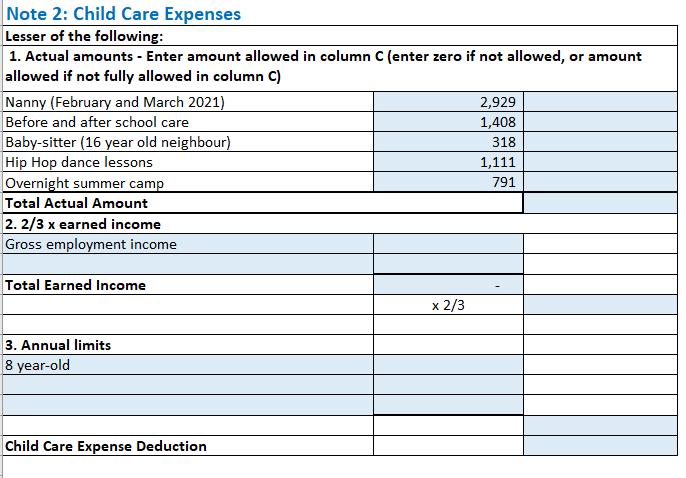

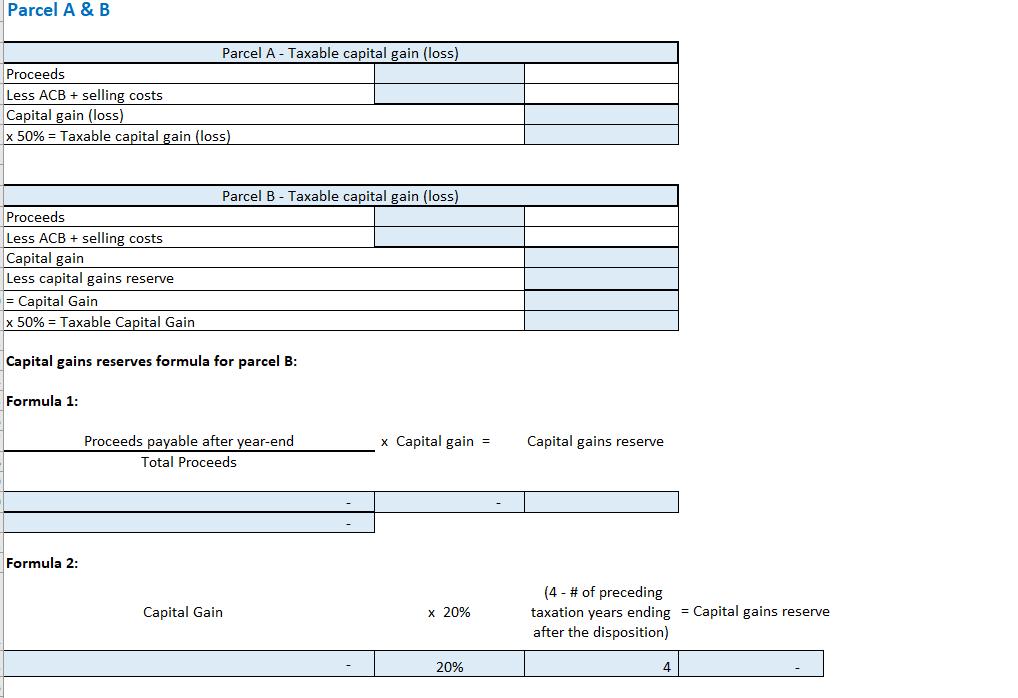

Emmy Peterson, a single taxpayer, was able to complete her own taxes prior to 2021. In...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

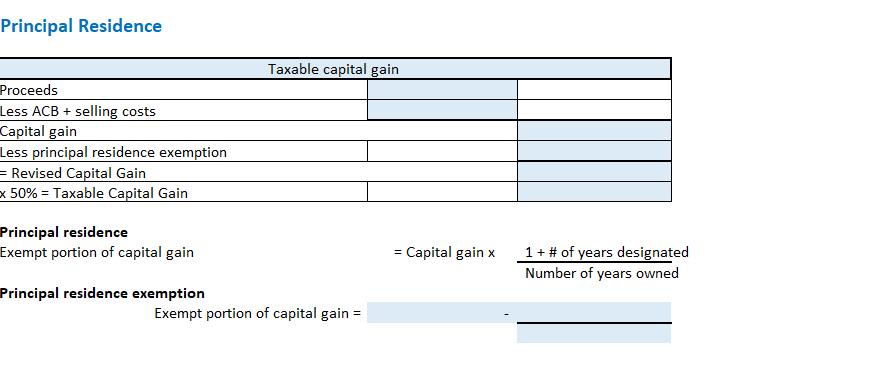

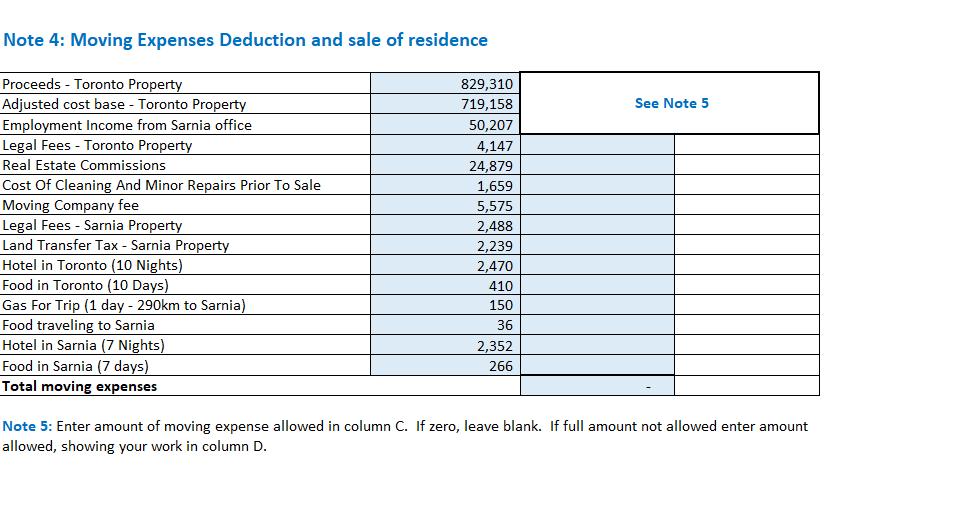

Emmy Peterson, a single taxpayer, was able to complete her own taxes prior to 2021. In 2020 she earned employment income, had a business loss from a partnership and contributed to her RRSP. This year, however, she requires assistance due to the following life changes and transactions. Income sources and amounts for 2021 are shown below. Income Sources Net Employment Income RPP Contribution Net Business Income (Loss) Interest income Amount 143,219 11,158 (31,345) 1,971 She is unable to find her 2020 notice of assessment with her 2021 RRSP deduction limit, however, she has provided what information she can in note 1. She adopted an 8 year-old child from the Ukraine and obtained custody on February 1, 2021. She hired a nanny for two months to help the child, Andi, get settled before she began school. The neighbour babysits when Emmy has to work a few hours on the weekend. Andi took hip hop dance lessons at J'dore Dance for eight weeks and attended overnight summer camp for two weeks. Costs paid in the year are outlined in note 2. FMV at time of inheritance Proceeds She sold two parcels of land she had inherited from her grandmother in 2020. The fair market value at the time of inheritance and the proceeds are outlined below. She entered into a financing arrangement with the buyer of parcel B to receive a 30% down payment in the year of sale, 30% in the year following the sale and the remaining 40% the year thereafter. Templates to calculate gains and losses are provided in note 3. Parcel A 97,596 72,704 Parcel B 832,014 1,047,083 She was requested to relocate by her employer and agreed thinking moving to a smaller center may be better to raise a child. For this reason she agreed to relocated from Toronto to Sarnia. She owned the home she sold in Toronto for nine years. She would like to utilize the principal residence exemption for this transaction. During this 9 years she owned a condo for four years and used the principal residence to fully exempt the gain. Costs associated with the move, and sale of her residence are contained in note 4. Emmy will use the simplified method of determining vehicle and food costs in calculating her moving expenses. Assume that the relevant flat rate for vehicle expenses is $0.53 for Ontario, and the flat rate for meals is $51 per person per day. Required: Complete Emmy's net income for tax calculation, showing all of your work in the templates provided. Income under ITA 3(a) Net Employment Income Interest income Income under ITA 3(b) Taxable Capital Gains Allowable Capital Losses Subtotal 3(a) + 3(b) Deductions under ITA 3(c) Childcare Expenses Moving Expenses RRSP Deduction Subtotal 3(c) Deduction under ITA 3(d) Net Business Income (Loss) Net Income for tax purposes Note 1: RRSP Deduction Income Sources 2020 unused deduction limit 2020 pension adjustment 2020 earned income for RRSP Undeducted contributions from prior years RRSP Contribution Unused deduction room (2020) + 18% of prior year earned income or $27,830 Less Pension Adjustment 2021 RRSP Deduction Limit RRSP Deduction is the lesser of: 2021 RRSP Deduction Limit Contributions Amount 143,219 1,971 56,049 22,764 89,592 10,536 23,046 (31,345) Note 2: Child Care Expenses Lesser of the following: 1. Actual amounts - Enter amount allowed in column C (enter zero if not allowed, or amount allowed if not fully allowed in column C) Nanny (February and March 2021) Before and after school care Baby-sitter (16 year old neighbour) Hip Hop dance lessons Overnight summer camp Total Actual Amount 2. 2/3 x earned income Gross employment income Total Earned Income 3. Annual limits 8 year-old Child Care Expense Deduction x 2/3 2,929 1,408 318 1,111 791 Parcel A & B Proceeds Less ACB + selling costs Capital gain (loss) x 50% = Taxable capital gain (loss) Proceeds Less ACB + selling costs Capital gain Less capital gains reserve Parcel A - Taxable capital gain (loss) Formula 2: Parcel B Taxable capital gain (loss) = Capital Gain x 50%= Taxable Capital Gain Capital gains reserves formula for parcel B: Formula 1: Proceeds payable after year-end Total Proceeds Capital Gain x Capital gain = x 20% 20% Capital gains reserve (4- # of preceding taxation years ending = Capital gains reserve after the disposition) 4 Principal Residence Proceeds Less ACB + selling costs Capital gain Less principal residence exemption = Revised Capital Gain x 50% Taxable Capital Gain Principal residence Exempt portion of capital gain Principal residence exemption Taxable capital gain Exempt portion of capital gain = = = Capital gain x 1 + # of years designated Number of years owned Note 4: Moving Expenses Deduction and sale of residence Proceeds - Toronto Property Adjusted cost base - Toronto Property Employment Income from Sarnia office Legal Fees - Toronto Property Real Estate Commissions Cost Of Cleaning And Minor Repairs Prior To Sale Moving Company fee Legal Fees - Sarnia Property Land Transfer Tax - Sarnia Property Hotel in Toronto (10 Nights) Food in Toronto (10 Days) Gas For Trip (1 day - 290km to Sarnia) Food traveling to Sarnia Hotel in Sarnia (7 Nights) Food in Sarnia (7 days) Total moving expenses 829,310 719,158 50,207 4,147 24,879 1,659 5,575 2,488 2,239 2,470 410 150 36 2,352 266 See Note 5 Note 5: Enter amount of moving expense allowed in column C. If zero, leave blank. If full amount not allowed enter amount allowed, showing your work in column D. Emmy has reviewed your calculation of net income for tax purposes and has the following questions. 1. Since this is Emmy's first year claiming the childcare expense deduction is wondering if you can explain the amount of deducted. (3 marks) 2. Emmy thought the capital gain on the sale of the parcel B land was a lot larger then what was included in income. She is wondering if you can explain why the entire capital gain was not included in income? (3 marks) 3. Emmy is curious as to how you determined the number of years she designated her Toronto home, and why the capital gain isn't fully exempt like her condo was. (3 marks) 4. Emmy is wondering if you made changes to the list of moving expenses she provided? She is wondering if you can explain these to her. (3 marks) Emmy Peterson, a single taxpayer, was able to complete her own taxes prior to 2021. In 2020 she earned employment income, had a business loss from a partnership and contributed to her RRSP. This year, however, she requires assistance due to the following life changes and transactions. Income sources and amounts for 2021 are shown below. Income Sources Net Employment Income RPP Contribution Net Business Income (Loss) Interest income Amount 143,219 11,158 (31,345) 1,971 She is unable to find her 2020 notice of assessment with her 2021 RRSP deduction limit, however, she has provided what information she can in note 1. She adopted an 8 year-old child from the Ukraine and obtained custody on February 1, 2021. She hired a nanny for two months to help the child, Andi, get settled before she began school. The neighbour babysits when Emmy has to work a few hours on the weekend. Andi took hip hop dance lessons at J'dore Dance for eight weeks and attended overnight summer camp for two weeks. Costs paid in the year are outlined in note 2. FMV at time of inheritance Proceeds She sold two parcels of land she had inherited from her grandmother in 2020. The fair market value at the time of inheritance and the proceeds are outlined below. She entered into a financing arrangement with the buyer of parcel B to receive a 30% down payment in the year of sale, 30% in the year following the sale and the remaining 40% the year thereafter. Templates to calculate gains and losses are provided in note 3. Parcel A 97,596 72,704 Parcel B 832,014 1,047,083 She was requested to relocate by her employer and agreed thinking moving to a smaller center may be better to raise a child. For this reason she agreed to relocated from Toronto to Sarnia. She owned the home she sold in Toronto for nine years. She would like to utilize the principal residence exemption for this transaction. During this 9 years she owned a condo for four years and used the principal residence to fully exempt the gain. Costs associated with the move, and sale of her residence are contained in note 4. Emmy will use the simplified method of determining vehicle and food costs in calculating her moving expenses. Assume that the relevant flat rate for vehicle expenses is $0.53 for Ontario, and the flat rate for meals is $51 per person per day. Required: Complete Emmy's net income for tax calculation, showing all of your work in the templates provided. Income under ITA 3(a) Net Employment Income Interest income Income under ITA 3(b) Taxable Capital Gains Allowable Capital Losses Subtotal 3(a) + 3(b) Deductions under ITA 3(c) Childcare Expenses Moving Expenses RRSP Deduction Subtotal 3(c) Deduction under ITA 3(d) Net Business Income (Loss) Net Income for tax purposes Note 1: RRSP Deduction Income Sources 2020 unused deduction limit 2020 pension adjustment 2020 earned income for RRSP Undeducted contributions from prior years RRSP Contribution Unused deduction room (2020) + 18% of prior year earned income or $27,830 Less Pension Adjustment 2021 RRSP Deduction Limit RRSP Deduction is the lesser of: 2021 RRSP Deduction Limit Contributions Amount 143,219 1,971 56,049 22,764 89,592 10,536 23,046 (31,345) Note 2: Child Care Expenses Lesser of the following: 1. Actual amounts - Enter amount allowed in column C (enter zero if not allowed, or amount allowed if not fully allowed in column C) Nanny (February and March 2021) Before and after school care Baby-sitter (16 year old neighbour) Hip Hop dance lessons Overnight summer camp Total Actual Amount 2. 2/3 x earned income Gross employment income Total Earned Income 3. Annual limits 8 year-old Child Care Expense Deduction x 2/3 2,929 1,408 318 1,111 791 Parcel A & B Proceeds Less ACB + selling costs Capital gain (loss) x 50% = Taxable capital gain (loss) Proceeds Less ACB + selling costs Capital gain Less capital gains reserve Parcel A - Taxable capital gain (loss) Formula 2: Parcel B Taxable capital gain (loss) = Capital Gain x 50%= Taxable Capital Gain Capital gains reserves formula for parcel B: Formula 1: Proceeds payable after year-end Total Proceeds Capital Gain x Capital gain = x 20% 20% Capital gains reserve (4- # of preceding taxation years ending = Capital gains reserve after the disposition) 4 Principal Residence Proceeds Less ACB + selling costs Capital gain Less principal residence exemption = Revised Capital Gain x 50% Taxable Capital Gain Principal residence Exempt portion of capital gain Principal residence exemption Taxable capital gain Exempt portion of capital gain = = = Capital gain x 1 + # of years designated Number of years owned Note 4: Moving Expenses Deduction and sale of residence Proceeds - Toronto Property Adjusted cost base - Toronto Property Employment Income from Sarnia office Legal Fees - Toronto Property Real Estate Commissions Cost Of Cleaning And Minor Repairs Prior To Sale Moving Company fee Legal Fees - Sarnia Property Land Transfer Tax - Sarnia Property Hotel in Toronto (10 Nights) Food in Toronto (10 Days) Gas For Trip (1 day - 290km to Sarnia) Food traveling to Sarnia Hotel in Sarnia (7 Nights) Food in Sarnia (7 days) Total moving expenses 829,310 719,158 50,207 4,147 24,879 1,659 5,575 2,488 2,239 2,470 410 150 36 2,352 266 See Note 5 Note 5: Enter amount of moving expense allowed in column C. If zero, leave blank. If full amount not allowed enter amount allowed, showing your work in column D. Emmy has reviewed your calculation of net income for tax purposes and has the following questions. 1. Since this is Emmy's first year claiming the childcare expense deduction is wondering if you can explain the amount of deducted. (3 marks) 2. Emmy thought the capital gain on the sale of the parcel B land was a lot larger then what was included in income. She is wondering if you can explain why the entire capital gain was not included in income? (3 marks) 3. Emmy is curious as to how you determined the number of years she designated her Toronto home, and why the capital gain isn't fully exempt like her condo was. (3 marks) 4. Emmy is wondering if you made changes to the list of moving expenses she provided? She is wondering if you can explain these to her. (3 marks) Emmy Peterson, a single taxpayer, was able to complete her own taxes prior to 2021. In 2020 she earned employment income, had a business loss from a partnership and contributed to her RRSP. This year, however, she requires assistance due to the following life changes and transactions. Income sources and amounts for 2021 are shown below. Income Sources Net Employment Income RPP Contribution Net Business Income (Loss) Interest income Amount 143,219 11,158 (31,345) 1,971 She is unable to find her 2020 notice of assessment with her 2021 RRSP deduction limit, however, she has provided what information she can in note 1. She adopted an 8 year-old child from the Ukraine and obtained custody on February 1, 2021. She hired a nanny for two months to help the child, Andi, get settled before she began school. The neighbour babysits when Emmy has to work a few hours on the weekend. Andi took hip hop dance lessons at J'dore Dance for eight weeks and attended overnight summer camp for two weeks. Costs paid in the year are outlined in note 2. FMV at time of inheritance Proceeds She sold two parcels of land she had inherited from her grandmother in 2020. The fair market value at the time of inheritance and the proceeds are outlined below. She entered into a financing arrangement with the buyer of parcel B to receive a 30% down payment in the year of sale, 30% in the year following the sale and the remaining 40% the year thereafter. Templates to calculate gains and losses are provided in note 3. Parcel A 97,596 72,704 Parcel B 832,014 1,047,083 She was requested to relocate by her employer and agreed thinking moving to a smaller center may be better to raise a child. For this reason she agreed to relocated from Toronto to Sarnia. She owned the home she sold in Toronto for nine years. She would like to utilize the principal residence exemption for this transaction. During this 9 years she owned a condo for four years and used the principal residence to fully exempt the gain. Costs associated with the move, and sale of her residence are contained in note 4. Emmy will use the simplified method of determining vehicle and food costs in calculating her moving expenses. Assume that the relevant flat rate for vehicle expenses is $0.53 for Ontario, and the flat rate for meals is $51 per person per day. Required: Complete Emmy's net income for tax calculation, showing all of your work in the templates provided. Income under ITA 3(a) Net Employment Income Interest income Income under ITA 3(b) Taxable Capital Gains Allowable Capital Losses Subtotal 3(a) + 3(b) Deductions under ITA 3(c) Childcare Expenses Moving Expenses RRSP Deduction Subtotal 3(c) Deduction under ITA 3(d) Net Business Income (Loss) Net Income for tax purposes Note 1: RRSP Deduction Income Sources 2020 unused deduction limit 2020 pension adjustment 2020 earned income for RRSP Undeducted contributions from prior years RRSP Contribution Unused deduction room (2020) + 18% of prior year earned income or $27,830 Less Pension Adjustment 2021 RRSP Deduction Limit RRSP Deduction is the lesser of: 2021 RRSP Deduction Limit Contributions Amount 143,219 1,971 56,049 22,764 89,592 10,536 23,046 (31,345) Note 2: Child Care Expenses Lesser of the following: 1. Actual amounts - Enter amount allowed in column C (enter zero if not allowed, or amount allowed if not fully allowed in column C) Nanny (February and March 2021) Before and after school care Baby-sitter (16 year old neighbour) Hip Hop dance lessons Overnight summer camp Total Actual Amount 2. 2/3 x earned income Gross employment income Total Earned Income 3. Annual limits 8 year-old Child Care Expense Deduction x 2/3 2,929 1,408 318 1,111 791 Parcel A & B Proceeds Less ACB + selling costs Capital gain (loss) x 50% = Taxable capital gain (loss) Proceeds Less ACB + selling costs Capital gain Less capital gains reserve Parcel A - Taxable capital gain (loss) Formula 2: Parcel B Taxable capital gain (loss) = Capital Gain x 50%= Taxable Capital Gain Capital gains reserves formula for parcel B: Formula 1: Proceeds payable after year-end Total Proceeds Capital Gain x Capital gain = x 20% 20% Capital gains reserve (4- # of preceding taxation years ending = Capital gains reserve after the disposition) 4 Principal Residence Proceeds Less ACB + selling costs Capital gain Less principal residence exemption = Revised Capital Gain x 50% Taxable Capital Gain Principal residence Exempt portion of capital gain Principal residence exemption Taxable capital gain Exempt portion of capital gain = = = Capital gain x 1 + # of years designated Number of years owned Note 4: Moving Expenses Deduction and sale of residence Proceeds - Toronto Property Adjusted cost base - Toronto Property Employment Income from Sarnia office Legal Fees - Toronto Property Real Estate Commissions Cost Of Cleaning And Minor Repairs Prior To Sale Moving Company fee Legal Fees - Sarnia Property Land Transfer Tax - Sarnia Property Hotel in Toronto (10 Nights) Food in Toronto (10 Days) Gas For Trip (1 day - 290km to Sarnia) Food traveling to Sarnia Hotel in Sarnia (7 Nights) Food in Sarnia (7 days) Total moving expenses 829,310 719,158 50,207 4,147 24,879 1,659 5,575 2,488 2,239 2,470 410 150 36 2,352 266 See Note 5 Note 5: Enter amount of moving expense allowed in column C. If zero, leave blank. If full amount not allowed enter amount allowed, showing your work in column D. Emmy has reviewed your calculation of net income for tax purposes and has the following questions. 1. Since this is Emmy's first year claiming the childcare expense deduction is wondering if you can explain the amount of deducted. (3 marks) 2. Emmy thought the capital gain on the sale of the parcel B land was a lot larger then what was included in income. She is wondering if you can explain why the entire capital gain was not included in income? (3 marks) 3. Emmy is curious as to how you determined the number of years she designated her Toronto home, and why the capital gain isn't fully exempt like her condo was. (3 marks) 4. Emmy is wondering if you made changes to the list of moving expenses she provided? She is wondering if you can explain these to her. (3 marks) Emmy Peterson, a single taxpayer, was able to complete her own taxes prior to 2021. In 2020 she earned employment income, had a business loss from a partnership and contributed to her RRSP. This year, however, she requires assistance due to the following life changes and transactions. Income sources and amounts for 2021 are shown below. Income Sources Net Employment Income RPP Contribution Net Business Income (Loss) Interest income Amount 143,219 11,158 (31,345) 1,971 She is unable to find her 2020 notice of assessment with her 2021 RRSP deduction limit, however, she has provided what information she can in note 1. She adopted an 8 year-old child from the Ukraine and obtained custody on February 1, 2021. She hired a nanny for two months to help the child, Andi, get settled before she began school. The neighbour babysits when Emmy has to work a few hours on the weekend. Andi took hip hop dance lessons at J'dore Dance for eight weeks and attended overnight summer camp for two weeks. Costs paid in the year are outlined in note 2. FMV at time of inheritance Proceeds She sold two parcels of land she had inherited from her grandmother in 2020. The fair market value at the time of inheritance and the proceeds are outlined below. She entered into a financing arrangement with the buyer of parcel B to receive a 30% down payment in the year of sale, 30% in the year following the sale and the remaining 40% the year thereafter. Templates to calculate gains and losses are provided in note 3. Parcel A 97,596 72,704 Parcel B 832,014 1,047,083 She was requested to relocate by her employer and agreed thinking moving to a smaller center may be better to raise a child. For this reason she agreed to relocated from Toronto to Sarnia. She owned the home she sold in Toronto for nine years. She would like to utilize the principal residence exemption for this transaction. During this 9 years she owned a condo for four years and used the principal residence to fully exempt the gain. Costs associated with the move, and sale of her residence are contained in note 4. Emmy will use the simplified method of determining vehicle and food costs in calculating her moving expenses. Assume that the relevant flat rate for vehicle expenses is $0.53 for Ontario, and the flat rate for meals is $51 per person per day. Required: Complete Emmy's net income for tax calculation, showing all of your work in the templates provided. Income under ITA 3(a) Net Employment Income Interest income Income under ITA 3(b) Taxable Capital Gains Allowable Capital Losses Subtotal 3(a) + 3(b) Deductions under ITA 3(c) Childcare Expenses Moving Expenses RRSP Deduction Subtotal 3(c) Deduction under ITA 3(d) Net Business Income (Loss) Net Income for tax purposes Note 1: RRSP Deduction Income Sources 2020 unused deduction limit 2020 pension adjustment 2020 earned income for RRSP Undeducted contributions from prior years RRSP Contribution Unused deduction room (2020) + 18% of prior year earned income or $27,830 Less Pension Adjustment 2021 RRSP Deduction Limit RRSP Deduction is the lesser of: 2021 RRSP Deduction Limit Contributions Amount 143,219 1,971 56,049 22,764 89,592 10,536 23,046 (31,345) Note 2: Child Care Expenses Lesser of the following: 1. Actual amounts - Enter amount allowed in column C (enter zero if not allowed, or amount allowed if not fully allowed in column C) Nanny (February and March 2021) Before and after school care Baby-sitter (16 year old neighbour) Hip Hop dance lessons Overnight summer camp Total Actual Amount 2. 2/3 x earned income Gross employment income Total Earned Income 3. Annual limits 8 year-old Child Care Expense Deduction x 2/3 2,929 1,408 318 1,111 791 Parcel A & B Proceeds Less ACB + selling costs Capital gain (loss) x 50% = Taxable capital gain (loss) Proceeds Less ACB + selling costs Capital gain Less capital gains reserve Parcel A - Taxable capital gain (loss) Formula 2: Parcel B Taxable capital gain (loss) = Capital Gain x 50%= Taxable Capital Gain Capital gains reserves formula for parcel B: Formula 1: Proceeds payable after year-end Total Proceeds Capital Gain x Capital gain = x 20% 20% Capital gains reserve (4- # of preceding taxation years ending = Capital gains reserve after the disposition) 4 Principal Residence Proceeds Less ACB + selling costs Capital gain Less principal residence exemption = Revised Capital Gain x 50% Taxable Capital Gain Principal residence Exempt portion of capital gain Principal residence exemption Taxable capital gain Exempt portion of capital gain = = = Capital gain x 1 + # of years designated Number of years owned Note 4: Moving Expenses Deduction and sale of residence Proceeds - Toronto Property Adjusted cost base - Toronto Property Employment Income from Sarnia office Legal Fees - Toronto Property Real Estate Commissions Cost Of Cleaning And Minor Repairs Prior To Sale Moving Company fee Legal Fees - Sarnia Property Land Transfer Tax - Sarnia Property Hotel in Toronto (10 Nights) Food in Toronto (10 Days) Gas For Trip (1 day - 290km to Sarnia) Food traveling to Sarnia Hotel in Sarnia (7 Nights) Food in Sarnia (7 days) Total moving expenses 829,310 719,158 50,207 4,147 24,879 1,659 5,575 2,488 2,239 2,470 410 150 36 2,352 266 See Note 5 Note 5: Enter amount of moving expense allowed in column C. If zero, leave blank. If full amount not allowed enter amount allowed, showing your work in column D. Emmy has reviewed your calculation of net income for tax purposes and has the following questions. 1. Since this is Emmy's first year claiming the childcare expense deduction is wondering if you can explain the amount of deducted. (3 marks) 2. Emmy thought the capital gain on the sale of the parcel B land was a lot larger then what was included in income. She is wondering if you can explain why the entire capital gain was not included in income? (3 marks) 3. Emmy is curious as to how you determined the number of years she designated her Toronto home, and why the capital gain isn't fully exempt like her condo was. (3 marks) 4. Emmy is wondering if you made changes to the list of moving expenses she provided? She is wondering if you can explain these to her. (3 marks)

Expert Answer:

Answer rating: 100% (QA)

1 Childcare Expense Deduction Emmys Childcare Expense Deduction is determined based on the lesser of the following three amounts 1 Actual Amounts Nann... View the full answer

Related Book For

Income Tax Fundamentals 2013

ISBN: 9781285586618

31st Edition

Authors: Gerald E. Whittenburg, Martha Altus Buller, Steven L Gill

Posted Date:

Students also viewed these accounting questions

-

The Crazy Eddie fraud may appear smaller and gentler than the massive billion-dollar frauds exposed in recent times, such as Bernie Madoffs Ponzi scheme, frauds in the subprime mortgage market, the...

-

1. What evidence is there that Michelle lacks contentment? 2. Inwhat ways is Michelle exhibiting ambivalence toward her finances? 3. What financial idols does Michelle have in her life? 4. What goals...

-

The following additional information is available for the Dr. Ivan and Irene Incisor family from Chapters 1-5. Ivan's grandfather died and left a portfolio of municipal bonds. In 2012, they pay Ivan...

-

Question: If you were a consultant and for the below M&A case, what questions would you ask as a consultant of the acquiring company of the mine and in order to complete the valuation: A firm is...

-

A contractor agreed to build a skating rink for the plaintiff at a price of $180,000. The rink was to be completed by December 1 and was designed to replace a similar but older rink that the...

-

Mohamed cannot understand why the carrying amount of accounts receivable does not change when an uncollectible account is written off under the allowance method. Clarify this for Mohamed.

-

Williams-Sonoma, Inc., is a specialty retailer of products for the home. The retail segment of the companys business sells products through its retail concepts: Williams-Sonoma, Pottery Barn, Pottery...

-

Establishing materiality and allocation of materiality to individual accounts requires considerable judgment. Access Microsofts 2009 financial statements at www.microsoft.com (use the investor...

-

High Time Tours leased rock-climbing equipment from Adventures Leasing on January 1, 2024. High Time has the option to renew the lease at the end of two years for an additional three years for $8,900...

-

Singh and Rajamani [25] provide data for a local wood manufacturer that wants to decrease material handling by changing from a process layout to a GT layout. It is considering installing a conveyor...

-

Communication helps us express our ideas and better understand others. In fact, delivering clear messages through oral and written communication are critical aspects of our daily lives. Take a second...

-

Kara, Incorporated, imposes a payback cutoff of three years for its international investment projects. Assume the company has the following two projects available. Year Cash Flow (A) Cash Flow (B) ...

-

What is contribution margin? How is it calculated? How is it useful in the cost-volume-profit analysis and/or sales mix decisions?

-

On January 28, 1986, the Space Shuttle Challenger broke apart 73 seconds into its flight, killing all seven crew members aboard. The spacecraft disintegrated 46,000 feet (14 km) above the Atlantic Oce

-

Question 6 a)Explain briefly why it is prudent for investors to create Investment Policy Statement (IPS) when working with a financial advisor (2 marks) b)Describe the strategic asset allocation you...

-

The actual production volume is usually larger than the budged production volume. Please explain how the conservative estimate affects financial statements (i.e., the profit statement and balance...

-

Sabre Company buys tiles and prints different designs on them for souvenir and gift stores. The company keeps on hand a stock equal to 25% of the next month's sales. The tiles cost $3 and are...

-

Several months have passed and the Managing Partner approved and properly filed the Complaint and properly submitted the Request for Production of Documents that you drafted. In fact, it has been 75...

-

During 2012, William purchases the following capital assets for use in his catering business: New passenger automobile (September 30)........................$21,500 Baking equipment (June 30)...

-

Leslie and Leon Lazo are married and file a joint return for 2012. Leslie's Social Security number is 466-47-3311 and Leon's is 467-74-4451. They live at 143 Snapdragon Drive, Reno, NV 82102. For...

-

Mike purchases a heavy-duty truck (5-year class recovery property) for his delivery service on April 30, 2012. The truck is not considered a passenger automobile for purposes of the listed property...

-

Describe how monopoly regulation influences output, price, economic profit, and efficiency.

-

Describe and explain the inefficiencies of monopoly.

-

Why is pure monopoly rare?

Study smarter with the SolutionInn App