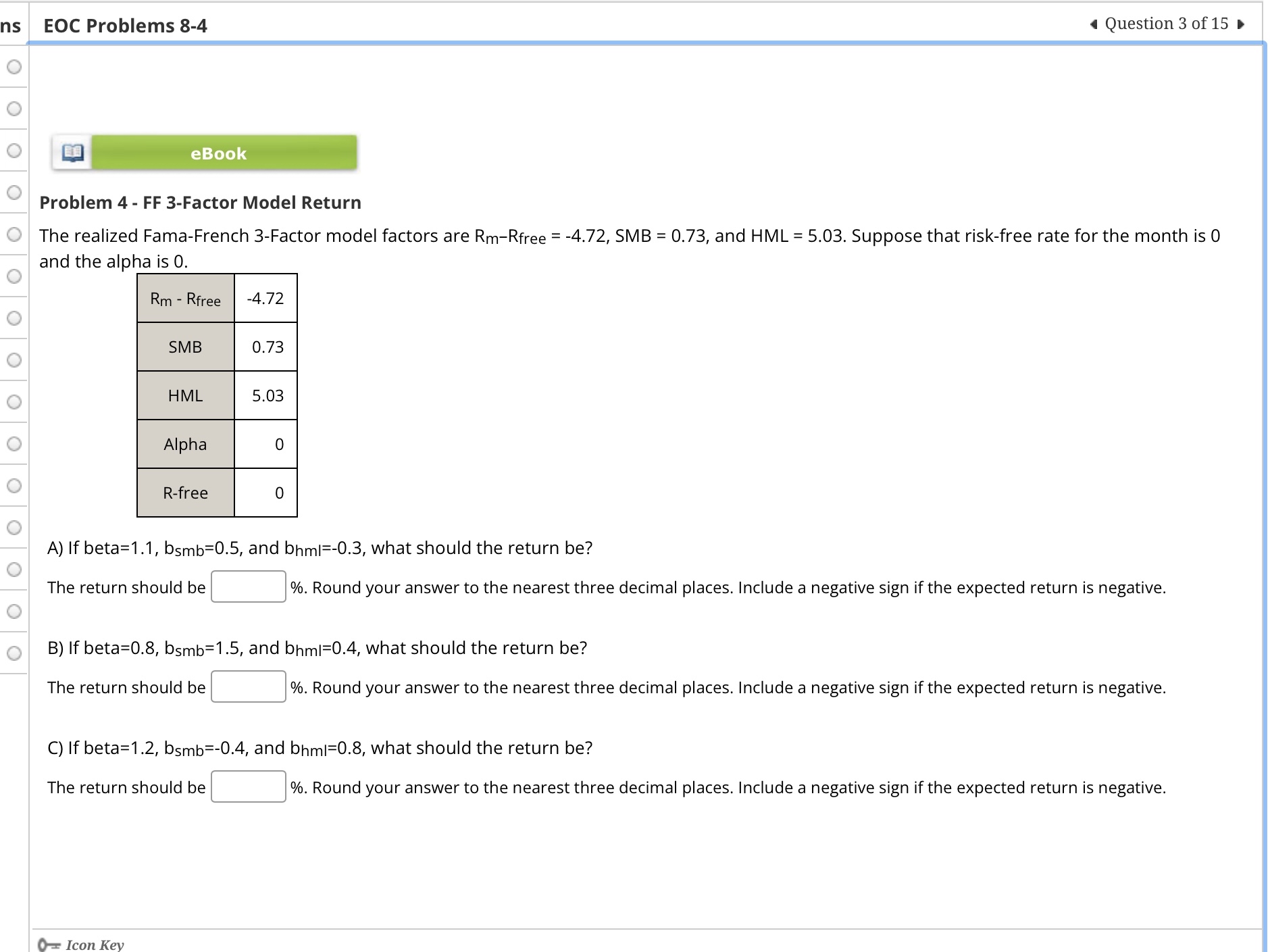

Question: EOC Problems 8 - 4 Question 3 of 1 5 eBook Problem 4 - FF 3 - Factor Model Return The realized Fama - French

EOC Problems

Question of

eBook

Problem FF Factor Model Return

The realized FamaFrench Factor model factors are and Suppose that riskfree rate for the month is and the alpha is

table Rfree,HMLAlphaRfree,

A If beta and what should the return be

The return should be Round your answer to the nearest three decimal places. Include a negative sign if the expected return is negative.

B If beta and what should the return be

The return should be

Round your answer to the nearest three decimal places. Include a negative sign if the expected return is negative.

C If beta and what should the return be

The return should be

Round your answer to the nearest three decimal places. Include a negative sign if the expected return is negative.

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock