Question: equired for each specific balance-ruut assertion. (Hint: See Table 6-5 on p. 165.) 6-32 (OBJECTIVES 6-8, 6-9) The following are specific transaction-related audit objectives applied

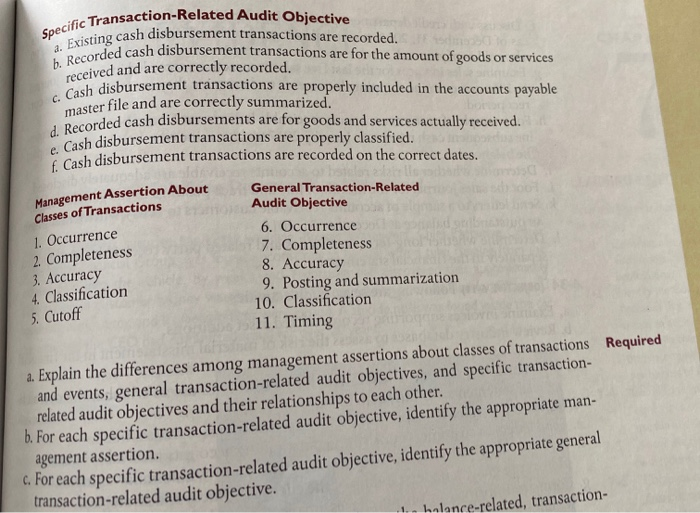

equired for each specific balance-ruut assertion. (Hint: See Table 6-5 on p. 165.) 6-32 (OBJECTIVES 6-8, 6-9) The following are specific transaction-related audit objectives applied to the audit of cash disbursement transactions (a through f.), management asser- tions about classes of transactions (1 through 5), and general transaction-related audit objectives (6 through 11). Specific Tran a. Existing cas b. Recorded cas c. Cash disbursement Gic Transaction-Related Audit Objective sisting cash disbursement transactions are recorded ded cash disbursement transactions are for the amount of goods or services received and are correctly recorded. disbursement transactions are properly included in the accounts payable master file and are correctly summarized. corded cash disbursements are for goods and services actually received. Cash disbursement transactions are properly classified Cosh disbursement transactions are recorded on the correct dates. Management Assertion About Classes of Transactions 1. Occurrence 2. Completeness 3. Accuracy 4. Classification 5. Cutoff General Transaction-Related Audit Objective 6. Occurrence 7. Completeness 8. Accuracy 9. Posting and summarization 10. Classification 11. Timing a. Explain the differences among management assertions about classes of transactions Required and events, general transaction-related audit objectives, and specific transaction- related audit objectives and their relationships to each other. b. For each specific transaction-related audit objective, identify the appropriate man- agement assertion. c. For each specific transaction-related audit objective, identify the appropriate general transaction-related audit objective. 1 moloted transaction

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts