Evaluate the performance of Community National Bank using the data in Exhibit 3.2, 3.4 and 3.6....

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

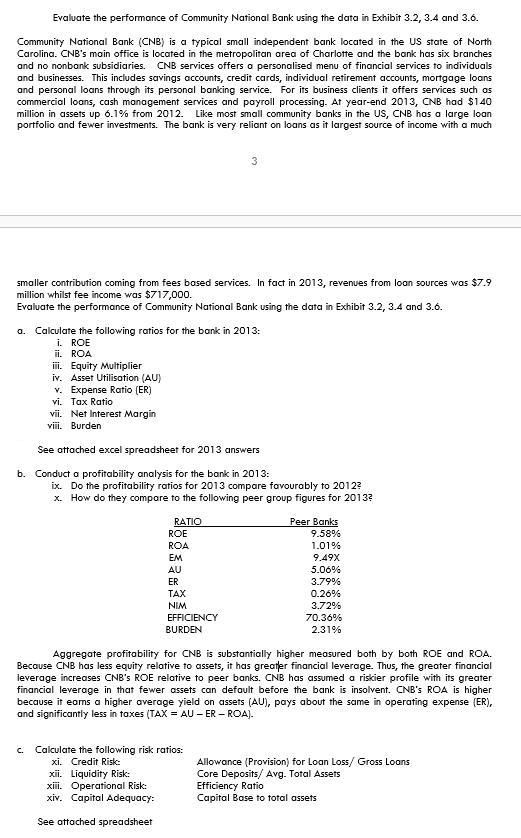

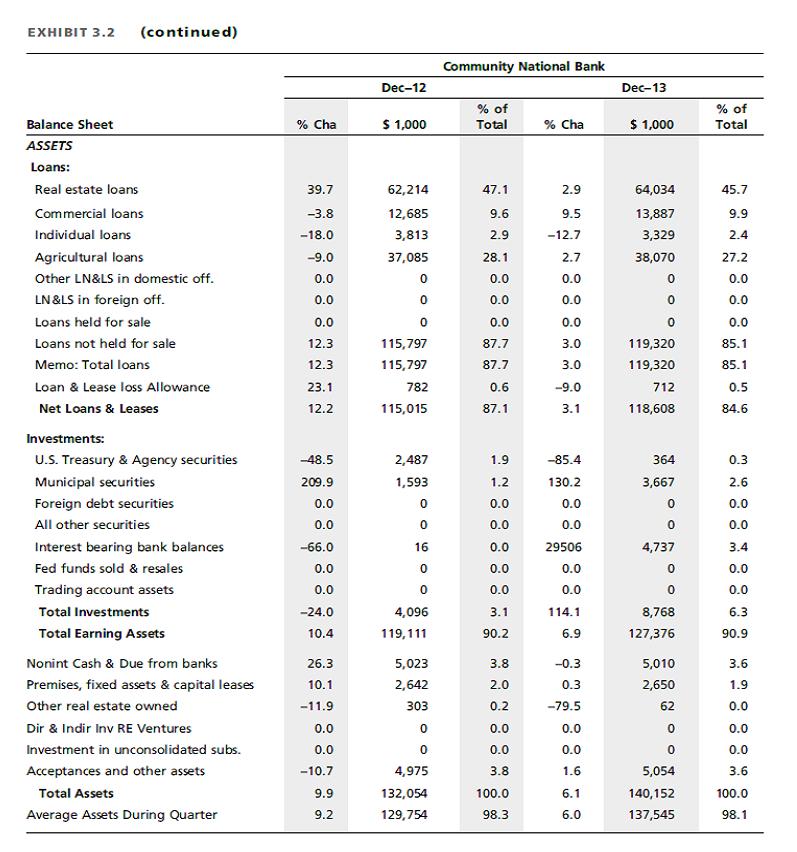

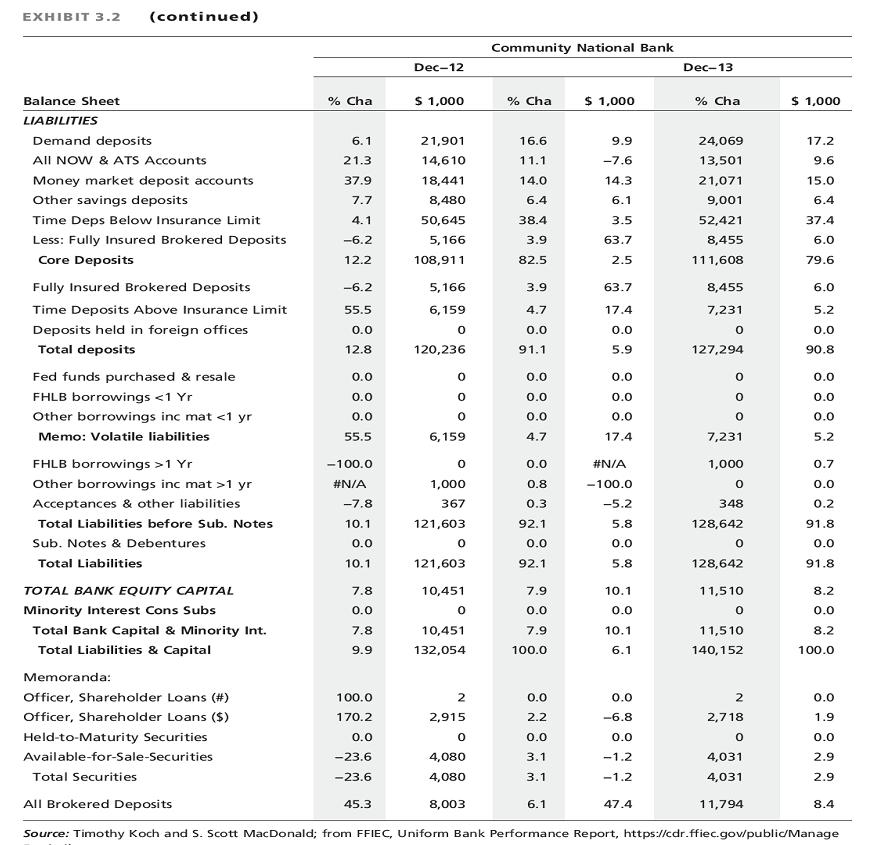

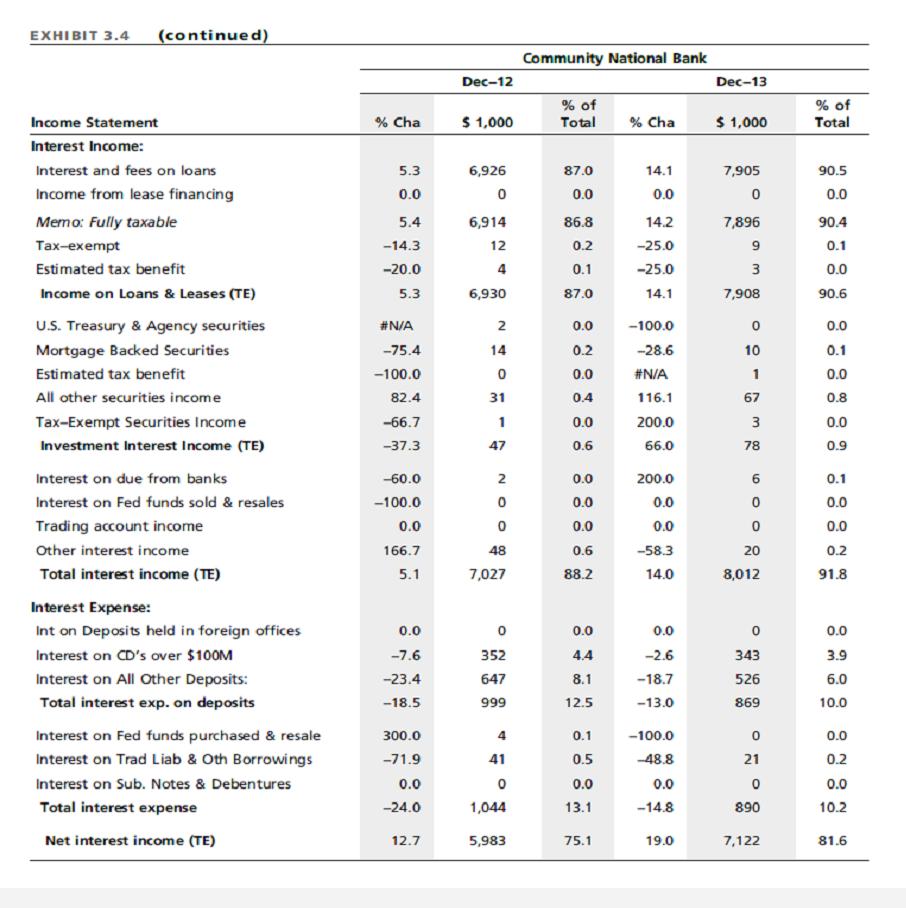

Evaluate the performance of Community National Bank using the data in Exhibit 3.2, 3.4 and 3.6. Community National Bank (CNB) is a typical small independent bank located in the US state of North Carolina. CNB's main office is located in the metropolitan area of Charlotte and the bank has six branches and no nonbank subsidiaries. CNB services offers a personalised menu of financial services to individuals and businesses. This includes savings accounts, credit cards, individual retirement accounts, mortgage loans and personal loans through its personal banking service. For its business clients it offers services such as commercial loans, cash management services and payroll processing. At year-end 2013, CNB had $140 million in assets up 6.1% from 2012. Like most small community banks in the US, CNB has a large loan portfolio and fewer investments. The bank is very reliant on loans as it largest source of income with a much smaller contribution coming from fees based services. In fact in 2013, revenues from loan sources was $7.9 million whilst fee income was $717,000. Evaluate the performance of Community National Bank using the data in Exhibit 3.2, 3.4 and 3.6. a. Calculate the following ratios for the bank in 2013: i. ROE ii. ROA iii. Equity Multiplier iv. Asset Utilisation (AU) v. Expense Ratio (ER) vi. Tax Ratio vii. Net Interest Margin viii. Burden See attached excel spreadsheet for 2013 answers b. Conduct a profitability analysis for the bank in 2013: ix. Do the profitability ratios for 2013 compare favourably to 2012? x. How do they compare to the following peer group figures for 2013? RATIO ROE ROA EM AU ER TAX NIM EFFICIENCY BURDEN xii. Liquidity Risk: xiii. Operational Risk: xiv. Capital Adequacy: See attached spreadsheet c. Calculate the following risk ratios: xi. Credit Risk: Peer Banks 9.58% Aggregate profitability for CNB is substantially higher measured both by both ROE and ROA. Because CNB has less equity relative to assets, it has greater financial leverage. Thus, the greater financial leverage increases CNB's ROE relative to peer banks. CNB has assumed a riskier profile with its greater financial leverage in that fewer assets can default before the bank is insolvent. CNB's ROA is higher because it eams a higher average yield on assets (AU), pays about the same in operating expense (ER), and significantly less in taxes (TAX = AU - ER-ROA). 1.01% 9.49X 5.06% 3.79% 0.26% 3.72% 70.36% 2.31% Allowance (Provision) for Loan Loss/Gross Loans Core Deposits/ Avg. Total Assets Efficiency Ratio Capital Base to total assets EXHIBIT 3.2 (continued) Balance Sheet ASSETS Loans: Real estate loans Commercial loans Individual loans Agricultural loans Other LN&LS in domestic off. LN&LS in foreign off. Loans held for sale Loans not held for sale Memo: Total loans Loan & Lease loss Allowance Net Loans & Leases Investments: U.S. Treasury & Agency securities Municipal securities Foreign debt securities All other securities Interest bearing bank balances Fed funds sold & resales Trading account assets Total Investments Total Earning Assets Nonint Cash & Due from banks Premises, fixed assets & capital leases Other real estate owned Dir & Indir Inv RE Ventures Investment in unconsolidated subs. Acceptances and other assets Total Assets Average Assets During Quarter % Cha 39.7 -3.8 -18.0 -9.0 0.0 0.0 0.0 12.3 12.3 23.1 12.2 -48.5 209.9 0.0 0.0 -66.0 0.0 0.0 -24.0 10.4 26.3 10.1 -11.9 0.0 0.0 -10.7 9.9 9.2 Dec-12 $ 1,000 62,214 12,685 3,813 37,085 0 0 115,797 115,797 782 115,015 2,487 1,593 0 0 16 0 0 4,096 119,111 5,023 2,642 303 0 0 4,975 132,054 129,754 Community National Bank % of Total 47.1 9.6 2.9 28.1 0.0 0.0 0.0 87.7 87.7 0.6 87.1 1.9 1.2 0.0 0.0 0.0 0.0 0.0 3.1 90.2 3.8 2.0 0.2 0.0 0.0 3.8 100.0 98.3 % Cha 2.9 9.5 -12.7 2.7 0.0 0.0 0.0 3.0 3.0 -9.0 3.1 -85.4 130.2 0.0 0.0 29506 0.0 0.0 114.1 6.9 -0.3 0.3 -79.5 0.0 0.0 1.6 6.1 6.0 Dec-13 $ 1,000 64,034 13,887 3,329 38,070 0 0 119,320 119,320 712 118,608 364 3,667 4,737 0 0 8,768 127,376 5,010 2,650 62 0 0 5,054 140,152 137,545 % of Total 45.7 9.9 2.4 27.2 0.0 0.0 0.0 85.1 85.1 0.5 84.6 0.3 2.6 0.0 0.0 3.4 0.0 0.0 6.3 90.9 3.6 1.9 0.0 0.0 0.0 3.6 100.0 98.1 EXHIBIT 3.2 (continued) Balance Sheet LIABILITIES Demand deposits All NOW & ATS Accounts Money market deposit accounts Other savings deposits Time Deps Below Insurance Limit Less: Fully Insured Brokered Deposits Core Deposits Fully Insured Brokered Deposits Time Deposits Above Insurance Limit Deposits held in foreign offices Total deposits Fed funds purchased & resale FHLB borrowings <1 Yr Other borrowings inc mat <1 yr Memo: Volatile liabilities FHLB borrowings >1 Yr Other borrowings inc mat >1 yr Acceptances & other liabilities Total Liabilities before Sub. Notes Sub. Notes & Debentures Total Liabilities TOTAL BANK EQUITY CAPITAL Minority Interest Cons Subs Total Bank Capital & Minority Int. Total Liabilities & Capital Memoranda: Officer, Shareholder Loans (#) Officer, Shareholder Loans ($) Held-to-Maturity Securities Available-for-Sale-Securities Total Securities % Cha 6.1 21.3 37.9 7.7 4.1 -6.2 12.2 -6.2 55.5 0.0 12.8 0.0 0.0 0.0 55.5 -100.0 #N/A -7.8 10.1 0.0 10.1 7.8 0.0 7.8 9.9 100.0 170.2 0.0 -23.6 -23.6 Dec-12 45.3 $ 1,000 21,901 14,610 18,441 8,480 50,645 5,166 108,911 5,166 6,159 0 120,236 0 0 0 6,159 0 1,000 367 121,603 0 121,603 10,451 0 10,451 132,054 2 2,915 0 4,080 4,080 8,003 Community National Bank % Cha 16.6 11.1 14.0 6.4 38.4 3.9 82.5 3.9 4.7 0.0 91.1 0.0 0.0 0.0 4.7 0.0 0.8 0.3 92.1 0.0 92.1 7.9 0.0 7.9 100.0 0.0 2.2 0.0 3.1 3.1 $ 1,000 6.1 9.9 -7.6 14.3 6.1 3.5 63.7 2.5 63.7 17.4 0.0 5.9 0.0 0.0 0.0 17.4 #N/A -100.0 -5.2 5.8 0.0 5.8 10.1 0.0 10.1 6.1 0.0 -6.8 0.0 -1.2 -1.2 47.4 Dec-13 % Cha 24,069 13,501 21,071 9,001 52,421 8,455 111,608 8,455 7,231 0 127,294 0 0 0 7,231 1,000 0 348 128,642 0 128,642 11,510 0 11,510 140,152 2 2,718 0 4,031 4,031 $ 1,000 11,794 17.2 9.6 15.0 6.4 37.4 6.0 79.6 6.0 5.2 0.0 90.8 0.0 0.0 0.0 5.2 0.7 0.0 0.2 91.8 0.0 91.8 All Brokered Deposits Source: Timothy Koch and S. Scott MacDonald; from FFIEC, Uniform Bank Performance Report, https://cdr.ffiec.gov/public/Manage 8.2 0.0 8.2 100.0 0.0 1.9 0.0 2.9 2.9 8.4 EXHIBIT 3.4 (continued) Income Statement Interest Income: Interest and fees on loans Income from lease financing Memo: Fully taxable Tax-exempt Estimated tax benefit Income on Loans & Leases (TE) U.S. Treasury & Agency securities Mortgage Backed Securities Estimated tax benefit All other securities income Tax-Exempt Securities Income Investment Interest Income (TE) Interest on due from banks Interest on Fed funds sold & resales Trading account income Other interest income Total interest income (TE) Interest Expense: Int on Deposits held in foreign offices Interest on CD's over $100M Interest on All Other Deposits: Total interest exp. on deposits Interest on Fed funds purchased & resale Interest on Trad Liab & Oth Borrowings Interest on Sub. Notes & Debentures Total interest expense Net interest income (TE) % Cha 5.3 0.0 5.4 -14.3 -20.0 5.3 #N/A -75.4 -100.0 82.4 -66.7 -37.3 -60.0 -100.0 0.0 166.7 5.1 0.0 -7.6 -23.4 -18.5 300.0 -71.9 0.0 -24.0 12.7 Dec-12 $ 1,000 6,926 0 6,914 12 4 6,930 2 14 0 31 1 47 2 0 0 48 7,027 0 352 647 999 4 41 0 1,044 5,983 Community National Bank % of Total 87.0 0.0 86.8 0.2 0.1 87.0 0.0 0.2 0.0 0.4 0.0 0.6 0.0 0.0 0.0 0.6 88.2 0.0 4.4 8.1 12.5 0.1 0.5 0.0 13.1 75.1 % Cha 14.1 0.0 14.2 -25.0 -25.0 14.1 -100.0 -28.6 #N/A 116.1 200.0 66.0 200.0 0.0 0.0 -58.3 14.0 0.0 -2.6 -18.7 -13.0 -100.0 -48.8 0.0 -14.8 19.0 Dec-13 $ 1,000 7,905 0 7,896 9 3 7,908 0 10 1 67 w 3 78 6 0 0 20 8,012 0 343 526 869 0 21 0 890 7,122 % of Total 90.5 0.0 90.4 0.1 0.0 90.6 0.0 0.1 0.0 0.8 0.0 0.9 0.1 0.0 0.0 0.2 91.8 0.0 3.9 6.0 10.0 0.0 0.2 0.0 10.2 81.6 EXHIBIT 3.4 (continued) Income Statement Noninterest Income: Fiduciary Activities Deposit service charges Trading rev, venture cap., securitize inc. Investment banking, advisory inc. Insurance commissions & fees Net servicing fees LN&LS net gains (losses) Other net gains (losses) Other noninterest income Total noninterest income Adjusted Operating Income (TE) Non-Interest Expenses: Personnel expense Occupancy expense Goodwill impairment Other Intangible Amortization Other Oper Exp (Incl intangibles) Total Noninterest Expenses Provision: Loan & Lease Losses Pretax Operating Income (TE) Realized G/L HId-to-Maturity Sec. Realized G/L Avail-for-Sale Sec. Pretax Net Operating Income (TE) Applicable Income Taxes Current Tax Equivalent Adjustment Other Tax Equivalent Adjustments Applicable Income Taxes (TE) Net Operating Income Net Extraordinary Items Net Inc Noncontrolling Minority Interests Net Income Cash Dividends Declared Retained Earnings % Cha 0.0 -13.5 0.0 0.0 #N/A 0.0 0.0 -53.1 -3.0 -5.8 9.7 18.8 1.4 0.0 0.0 5.5 12.0 -49.2 26.6 0.0 -105.8 20.8 0.0 -16.7 0.0 -16.7 21.0 0.0 0.0 21.0 72.6 -11.4 Dec-12 $ 1,000 0 660 0 0 3 6 0 (46) 318 941 6,924 2,901 567 0 0 1,763 5,231 254 1,439 0 (3) 1,436 0 5 0 5 1,431 0 0 1,431 787 644 Community National Bank % of Total 0.0 8.3 0.0 0.0 0.0 0.1 0.0 -0.6 4.0 11.8 86.9 36.4 7.1 0.0 0.0 22.1 65.7 3.2 18.1 0.0 0.0 18.0 0.0 0.1 0.0 0.1 18.0 0.0 0.0 18.0 9.9 8.1 0 % Cha 0.0 -19.1 0.0 0.0 -66.7 -16.7 0.0 132.6 -10.7 -23.8 13.2 11.9 29.1 0.0 0.0 -3.3 8.6 -58.7 42.7 0.0 -133.3 43.0 0.0 -20.0 0.0 -20.0 43.3 0.0 0.0 43.3 29.2 60.4 Dec-13 $ 1,000 0 534 0 0 1 5 0 (107) 284 717 7,839 3,245 732 0 0 1,704 5,681 105 2,053 0 1 2,054 0 4 0 4 2,050 0 0 2,050 1,017 1,033 % of Total 0.0 6.1 0.0 0.0 0.0 0.1 0.0 -1.2 3.3 8.2 89.8 37.2 8.4 0.0 0.0 19.5 65.1 1.2 23.5 0.0 0.0 23.5 0.0 0.0 0.0 0.0 23.5 0.0 0.0 23.5 11.6 11.8 Evaluate the performance of Community National Bank using the data in Exhibit 3.2, 3.4 and 3.6. Community National Bank (CNB) is a typical small independent bank located in the US state of North Carolina. CNB's main office is located in the metropolitan area of Charlotte and the bank has six branches and no nonbank subsidiaries. CNB services offers a personalised menu of financial services to individuals and businesses. This includes savings accounts, credit cards, individual retirement accounts, mortgage loans and personal loans through its personal banking service. For its business clients it offers services such as commercial loans, cash management services and payroll processing. At year-end 2013, CNB had $140 million in assets up 6.1% from 2012. Like most small community banks in the US, CNB has a large loan portfolio and fewer investments. The bank is very reliant on loans as it largest source of income with a much smaller contribution coming from fees based services. In fact in 2013, revenues from loan sources was $7.9 million whilst fee income was $717,000. Evaluate the performance of Community National Bank using the data in Exhibit 3.2, 3.4 and 3.6. a. Calculate the following ratios for the bank in 2013: i. ROE ii. ROA iii. Equity Multiplier iv. Asset Utilisation (AU) v. Expense Ratio (ER) vi. Tax Ratio vii. Net Interest Margin viii. Burden See attached excel spreadsheet for 2013 answers b. Conduct a profitability analysis for the bank in 2013: ix. Do the profitability ratios for 2013 compare favourably to 2012? x. How do they compare to the following peer group figures for 2013? RATIO ROE ROA EM AU ER TAX NIM EFFICIENCY BURDEN xii. Liquidity Risk: xiii. Operational Risk: xiv. Capital Adequacy: See attached spreadsheet c. Calculate the following risk ratios: xi. Credit Risk: Peer Banks 9.58% Aggregate profitability for CNB is substantially higher measured both by both ROE and ROA. Because CNB has less equity relative to assets, it has greater financial leverage. Thus, the greater financial leverage increases CNB's ROE relative to peer banks. CNB has assumed a riskier profile with its greater financial leverage in that fewer assets can default before the bank is insolvent. CNB's ROA is higher because it eams a higher average yield on assets (AU), pays about the same in operating expense (ER), and significantly less in taxes (TAX = AU - ER-ROA). 1.01% 9.49X 5.06% 3.79% 0.26% 3.72% 70.36% 2.31% Allowance (Provision) for Loan Loss/Gross Loans Core Deposits/ Avg. Total Assets Efficiency Ratio Capital Base to total assets EXHIBIT 3.2 (continued) Balance Sheet ASSETS Loans: Real estate loans Commercial loans Individual loans Agricultural loans Other LN&LS in domestic off. LN&LS in foreign off. Loans held for sale Loans not held for sale Memo: Total loans Loan & Lease loss Allowance Net Loans & Leases Investments: U.S. Treasury & Agency securities Municipal securities Foreign debt securities All other securities Interest bearing bank balances Fed funds sold & resales Trading account assets Total Investments Total Earning Assets Nonint Cash & Due from banks Premises, fixed assets & capital leases Other real estate owned Dir & Indir Inv RE Ventures Investment in unconsolidated subs. Acceptances and other assets Total Assets Average Assets During Quarter % Cha 39.7 -3.8 -18.0 -9.0 0.0 0.0 0.0 12.3 12.3 23.1 12.2 -48.5 209.9 0.0 0.0 -66.0 0.0 0.0 -24.0 10.4 26.3 10.1 -11.9 0.0 0.0 -10.7 9.9 9.2 Dec-12 $ 1,000 62,214 12,685 3,813 37,085 0 0 115,797 115,797 782 115,015 2,487 1,593 0 0 16 0 0 4,096 119,111 5,023 2,642 303 0 0 4,975 132,054 129,754 Community National Bank % of Total 47.1 9.6 2.9 28.1 0.0 0.0 0.0 87.7 87.7 0.6 87.1 1.9 1.2 0.0 0.0 0.0 0.0 0.0 3.1 90.2 3.8 2.0 0.2 0.0 0.0 3.8 100.0 98.3 % Cha 2.9 9.5 -12.7 2.7 0.0 0.0 0.0 3.0 3.0 -9.0 3.1 -85.4 130.2 0.0 0.0 29506 0.0 0.0 114.1 6.9 -0.3 0.3 -79.5 0.0 0.0 1.6 6.1 6.0 Dec-13 $ 1,000 64,034 13,887 3,329 38,070 0 0 119,320 119,320 712 118,608 364 3,667 4,737 0 0 8,768 127,376 5,010 2,650 62 0 0 5,054 140,152 137,545 % of Total 45.7 9.9 2.4 27.2 0.0 0.0 0.0 85.1 85.1 0.5 84.6 0.3 2.6 0.0 0.0 3.4 0.0 0.0 6.3 90.9 3.6 1.9 0.0 0.0 0.0 3.6 100.0 98.1 EXHIBIT 3.2 (continued) Balance Sheet LIABILITIES Demand deposits All NOW & ATS Accounts Money market deposit accounts Other savings deposits Time Deps Below Insurance Limit Less: Fully Insured Brokered Deposits Core Deposits Fully Insured Brokered Deposits Time Deposits Above Insurance Limit Deposits held in foreign offices Total deposits Fed funds purchased & resale FHLB borrowings <1 Yr Other borrowings inc mat <1 yr Memo: Volatile liabilities FHLB borrowings >1 Yr Other borrowings inc mat >1 yr Acceptances & other liabilities Total Liabilities before Sub. Notes Sub. Notes & Debentures Total Liabilities TOTAL BANK EQUITY CAPITAL Minority Interest Cons Subs Total Bank Capital & Minority Int. Total Liabilities & Capital Memoranda: Officer, Shareholder Loans (#) Officer, Shareholder Loans ($) Held-to-Maturity Securities Available-for-Sale-Securities Total Securities % Cha 6.1 21.3 37.9 7.7 4.1 -6.2 12.2 -6.2 55.5 0.0 12.8 0.0 0.0 0.0 55.5 -100.0 #N/A -7.8 10.1 0.0 10.1 7.8 0.0 7.8 9.9 100.0 170.2 0.0 -23.6 -23.6 Dec-12 45.3 $ 1,000 21,901 14,610 18,441 8,480 50,645 5,166 108,911 5,166 6,159 0 120,236 0 0 0 6,159 0 1,000 367 121,603 0 121,603 10,451 0 10,451 132,054 2 2,915 0 4,080 4,080 8,003 Community National Bank % Cha 16.6 11.1 14.0 6.4 38.4 3.9 82.5 3.9 4.7 0.0 91.1 0.0 0.0 0.0 4.7 0.0 0.8 0.3 92.1 0.0 92.1 7.9 0.0 7.9 100.0 0.0 2.2 0.0 3.1 3.1 $ 1,000 6.1 9.9 -7.6 14.3 6.1 3.5 63.7 2.5 63.7 17.4 0.0 5.9 0.0 0.0 0.0 17.4 #N/A -100.0 -5.2 5.8 0.0 5.8 10.1 0.0 10.1 6.1 0.0 -6.8 0.0 -1.2 -1.2 47.4 Dec-13 % Cha 24,069 13,501 21,071 9,001 52,421 8,455 111,608 8,455 7,231 0 127,294 0 0 0 7,231 1,000 0 348 128,642 0 128,642 11,510 0 11,510 140,152 2 2,718 0 4,031 4,031 $ 1,000 11,794 17.2 9.6 15.0 6.4 37.4 6.0 79.6 6.0 5.2 0.0 90.8 0.0 0.0 0.0 5.2 0.7 0.0 0.2 91.8 0.0 91.8 All Brokered Deposits Source: Timothy Koch and S. Scott MacDonald; from FFIEC, Uniform Bank Performance Report, https://cdr.ffiec.gov/public/Manage 8.2 0.0 8.2 100.0 0.0 1.9 0.0 2.9 2.9 8.4 EXHIBIT 3.4 (continued) Income Statement Interest Income: Interest and fees on loans Income from lease financing Memo: Fully taxable Tax-exempt Estimated tax benefit Income on Loans & Leases (TE) U.S. Treasury & Agency securities Mortgage Backed Securities Estimated tax benefit All other securities income Tax-Exempt Securities Income Investment Interest Income (TE) Interest on due from banks Interest on Fed funds sold & resales Trading account income Other interest income Total interest income (TE) Interest Expense: Int on Deposits held in foreign offices Interest on CD's over $100M Interest on All Other Deposits: Total interest exp. on deposits Interest on Fed funds purchased & resale Interest on Trad Liab & Oth Borrowings Interest on Sub. Notes & Debentures Total interest expense Net interest income (TE) % Cha 5.3 0.0 5.4 -14.3 -20.0 5.3 #N/A -75.4 -100.0 82.4 -66.7 -37.3 -60.0 -100.0 0.0 166.7 5.1 0.0 -7.6 -23.4 -18.5 300.0 -71.9 0.0 -24.0 12.7 Dec-12 $ 1,000 6,926 0 6,914 12 4 6,930 2 14 0 31 1 47 2 0 0 48 7,027 0 352 647 999 4 41 0 1,044 5,983 Community National Bank % of Total 87.0 0.0 86.8 0.2 0.1 87.0 0.0 0.2 0.0 0.4 0.0 0.6 0.0 0.0 0.0 0.6 88.2 0.0 4.4 8.1 12.5 0.1 0.5 0.0 13.1 75.1 % Cha 14.1 0.0 14.2 -25.0 -25.0 14.1 -100.0 -28.6 #N/A 116.1 200.0 66.0 200.0 0.0 0.0 -58.3 14.0 0.0 -2.6 -18.7 -13.0 -100.0 -48.8 0.0 -14.8 19.0 Dec-13 $ 1,000 7,905 0 7,896 9 3 7,908 0 10 1 67 w 3 78 6 0 0 20 8,012 0 343 526 869 0 21 0 890 7,122 % of Total 90.5 0.0 90.4 0.1 0.0 90.6 0.0 0.1 0.0 0.8 0.0 0.9 0.1 0.0 0.0 0.2 91.8 0.0 3.9 6.0 10.0 0.0 0.2 0.0 10.2 81.6 EXHIBIT 3.4 (continued) Income Statement Noninterest Income: Fiduciary Activities Deposit service charges Trading rev, venture cap., securitize inc. Investment banking, advisory inc. Insurance commissions & fees Net servicing fees LN&LS net gains (losses) Other net gains (losses) Other noninterest income Total noninterest income Adjusted Operating Income (TE) Non-Interest Expenses: Personnel expense Occupancy expense Goodwill impairment Other Intangible Amortization Other Oper Exp (Incl intangibles) Total Noninterest Expenses Provision: Loan & Lease Losses Pretax Operating Income (TE) Realized G/L HId-to-Maturity Sec. Realized G/L Avail-for-Sale Sec. Pretax Net Operating Income (TE) Applicable Income Taxes Current Tax Equivalent Adjustment Other Tax Equivalent Adjustments Applicable Income Taxes (TE) Net Operating Income Net Extraordinary Items Net Inc Noncontrolling Minority Interests Net Income Cash Dividends Declared Retained Earnings % Cha 0.0 -13.5 0.0 0.0 #N/A 0.0 0.0 -53.1 -3.0 -5.8 9.7 18.8 1.4 0.0 0.0 5.5 12.0 -49.2 26.6 0.0 -105.8 20.8 0.0 -16.7 0.0 -16.7 21.0 0.0 0.0 21.0 72.6 -11.4 Dec-12 $ 1,000 0 660 0 0 3 6 0 (46) 318 941 6,924 2,901 567 0 0 1,763 5,231 254 1,439 0 (3) 1,436 0 5 0 5 1,431 0 0 1,431 787 644 Community National Bank % of Total 0.0 8.3 0.0 0.0 0.0 0.1 0.0 -0.6 4.0 11.8 86.9 36.4 7.1 0.0 0.0 22.1 65.7 3.2 18.1 0.0 0.0 18.0 0.0 0.1 0.0 0.1 18.0 0.0 0.0 18.0 9.9 8.1 0 % Cha 0.0 -19.1 0.0 0.0 -66.7 -16.7 0.0 132.6 -10.7 -23.8 13.2 11.9 29.1 0.0 0.0 -3.3 8.6 -58.7 42.7 0.0 -133.3 43.0 0.0 -20.0 0.0 -20.0 43.3 0.0 0.0 43.3 29.2 60.4 Dec-13 $ 1,000 0 534 0 0 1 5 0 (107) 284 717 7,839 3,245 732 0 0 1,704 5,681 105 2,053 0 1 2,054 0 4 0 4 2,050 0 0 2,050 1,017 1,033 % of Total 0.0 6.1 0.0 0.0 0.0 0.1 0.0 -1.2 3.3 8.2 89.8 37.2 8.4 0.0 0.0 19.5 65.1 1.2 23.5 0.0 0.0 23.5 0.0 0.0 0.0 0.0 23.5 0.0 0.0 23.5 11.6 11.8

Expert Answer:

Answer rating: 100% (QA)

Based on the information provided here is an evaluation of Community National Banks performance using the given ratios a Calculating the ratios for the bank in 2013 I Return on Equity ROE ROE measures ... View the full answer

Related Book For

Posted Date:

Students also viewed these accounting questions

-

Evaluate the performance of Community National Bank using the data in Exhibit 3.2, 3.4 and 3.6. Community National Bank (CNB) is a typical small independent bank located in the US state of North...

-

Evaluate the performance of Community National Bank relative to peer banks using the data in Exhibits 3.2, 3.4, 3.7, 3.8, and 3.9. Did the bank perform above or below average in 2007? Did it operate...

-

Evaluate the performance of an organization or department. Identify an area that would significantly benefit from initiating a change. Include the following for a company: 1. Discuss the issues in...

-

How do items discussed in the critical audit matters section differ from items in an unqualified opinion with an emphasis-of-matter paragraph? Question 1: (20) A. On November 1, 2019. James Andersun...

-

A psychologist has to develop a new test of spatial perception, and she wants to estimate the mean score achieved by male pilots. How many people must she test if she wants the sample mean to be in...

-

According to www.fueleconomy.gov, a random sample of seven 2016 Subaru Forester AWD2.5 L, 4 cyl, automatic cars gave a mean of 26.4miles per gallon (MPG). Assume MPG for this vehicle follow a normal...

-

Why do we say that transport is a derived demand?

-

Satwinder deposited $145 at the end of each month for 15 years at 7.5% compounded monthly. After her last deposit she converted the balance into an ordinary annuity paying $1200 every 3 months for 12...

-

Identify the two modes of tax classifications and their respective tax systems in most open economies? Discuss the economic implications of the above (5a) tax systems in developing economies

-

a. How much cash does Patterson have on hand relative to its total assets? b. What proportion of Patterson's assets has the firm financed using short-term debt? Long-term debt? c. What percent of...

-

On their 20th birthday, twins Ann and Nancy receive a gift spaceship from their grandfather. While Nancy remains on Earth, Ann pilots her ship, "Dreamboat Annie", toward the 25-ly distant Klaatu...

-

Since its founding in 2010, the Chinese communications technology company Xiaomi has established itself as a true competitor among both global incumbents like Apple and Samsung and local niche...

-

Define and give an example of an immediate predecessor.

-

How do existing systems influence the architecture of new systems in the same organization?

-

Which criteria to pick a strategy do you consider most important? Why? Name one company that failed because it did not follow your Ee What should it have done instead?

-

Consider the automobile industry. Identify competitors to Ford SUVs and organize them in terms of their intensity of competition. Also organize them into strategic groups. What are the key success...

-

ABC Company bottles and distributes ABC Fizz, a flavoured wine beverage. $15.00 is the price the product is sold at to retailers. Management estimates the following revenues and costs at 100%...

-

Use of the contraceptive Depo Provera appears to triple women's risk of infection with chlamydia and gonorrhea , a study reports today. An estimated 20 million to 30 million women worldwide use Depo...

-

At December 31, 2017, the following data were available for a building owned by NU Company: Building cost ...........................................................................................

-

Fraternal Brothers provides consulting services on contract for a standard hourly rate of $100 per hour. The contracts allow the company to invoice the client evenly during the contract period. The...

-

Pronto Real Estate purchased a small warehouse in Winnipeg some years ago for $720,000. (The accompanying land was also purchased, but that information is not necessary for purposes of this...

-

In Problem 102, using an interest rate of 10 percent, what uniform series over the closed interval [1,8] is equivalent to the cash flow profile shown? Data from problem 102 Consider the following...

-

Consider the following cash flow profile: What is the present worth equivalent for the cash flow series with an interest rate of 12 percent? EOY Cash Flow EOY Cash Flow EOY Cash Flow 0 -$50,000 3...

-

In Problem 102, using an interest rate of 8 percent, what single sum of money occurring at the end of year 8 is equivalent to the cash flow profile shown? Data from problem 102 Consider the following...

Financial Accounting Essentials You Always Wanted To Know 3rd Edition - ISBN: 1946383678 - Free Book

Study smarter with the SolutionInn App