Question: Example: Interest rate model You are using the following 3-states Markov model: You are given the following constant forces of transition: (i) 01=0.05 (ii) 10=0.02

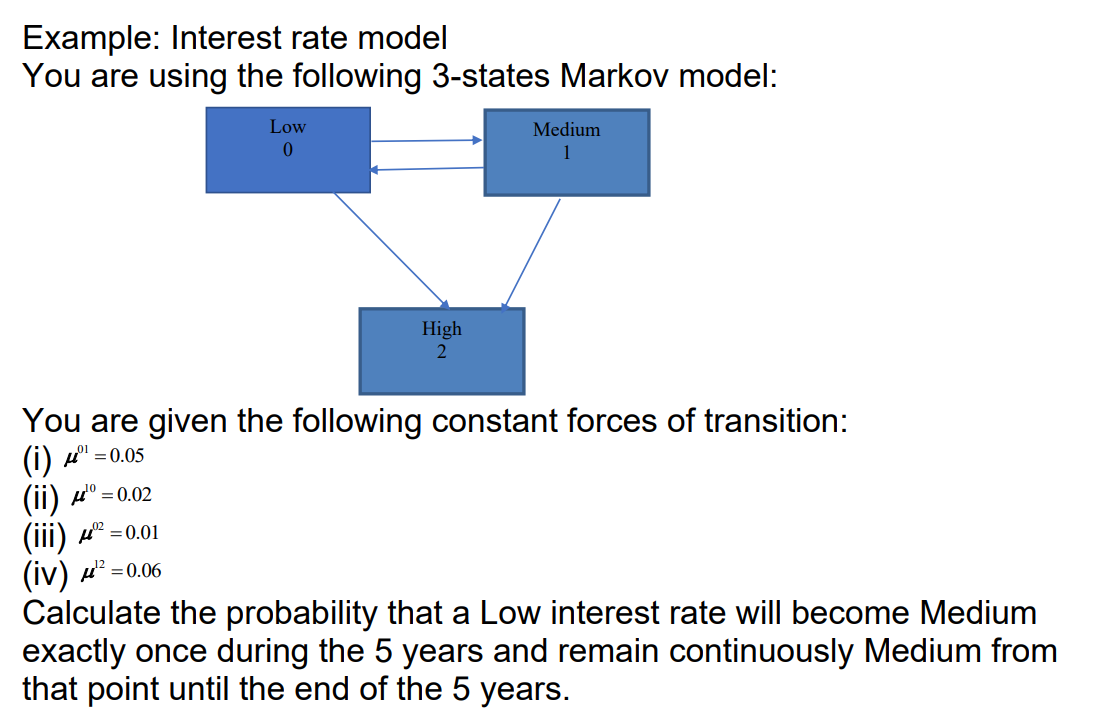

Example: Interest rate model You are using the following 3-states Markov model: You are given the following constant forces of transition: (i) 01=0.05 (ii) 10=0.02 (iii) 02=0.01 (iv) 12=0.06 Calculate the probability that a Low interest rate will become Medium exactly once during the 5 years and remain continuously Medium from that point until the end of the 5 years

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock