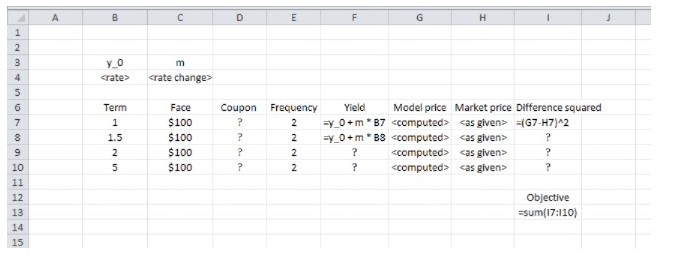

Question: Excel's Solver utility can also find an optimum solution involving more than one variable. We will use Solver to find the best fit of a

|

A B C D E F G H I yo m

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock