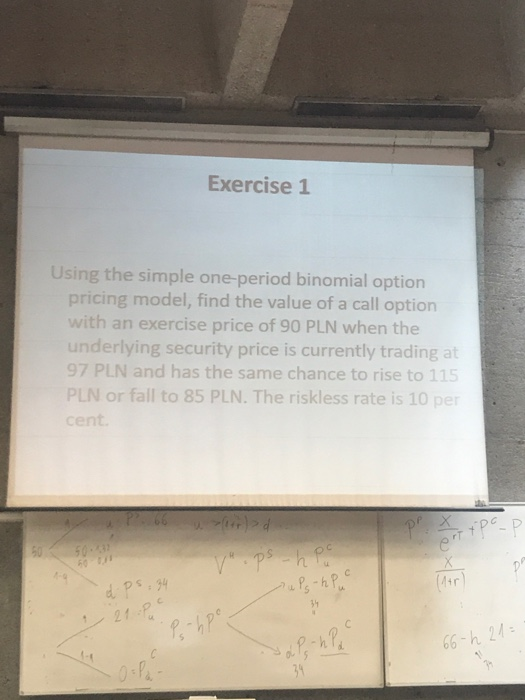

Question: Exercise 1 Using the simple one-period binomial option pricing model, find the value of a call option with an exercise price of 90 PLN when

Exercise 1 Using the simple one-period binomial option pricing model, find the value of a call option with an exercise price of 90 PLN when the underlying security price is currently trading at 97 PLN and has the same chance to rise to 115 PLN or fall to 85 PLN. The riskless rate is 10 per cent. +pe-P p. X 50-3 60 1AR 50 X (Ar 21-P 0 5 0-Ph 39

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock