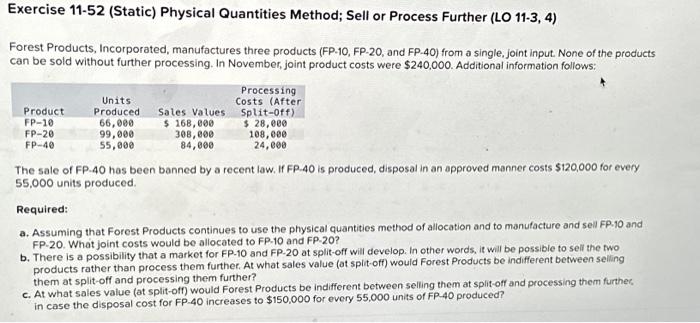

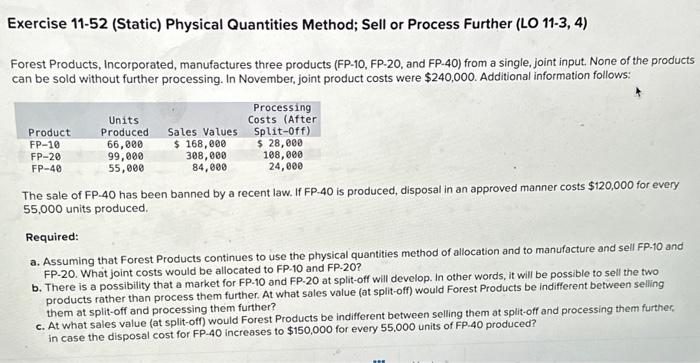

Question: Exercise 11-52 (Static) Physical Quantities Method; Sell or Process Further (LO 11-3, 4) Forest Products, Incorporated, manufactures three products (FP-10, FP-20, and FP-40) from a

Exercise 11-52 (Static) Physical Quantities Method; Sell or Process Further (LO 11-3, 4) Forest Products, Incorporated, manufactures three products (FP-10, FP-20, and FP-40) from a single, joint input. None of the products can be sold without further processing. In November, joint product costs were $240,000. Additional information follows: The sale of FP. 40 has been banned by a recent law. If FP. 40 is produced, disposal in an approved manner costs $120,000 for every 55,000 units produced. Required: a. Assuming that Forest Products continues to use the physical quantities method of allocation and to manufacture and sell FP. 10 and FP.20. What joint costs would be allocated to FP.10 and FP-20? b. There is a possibility that a market for FP-10 and FP-20 at split-off will develop. In other words, it will be possible to sell the two products rather than process them further. At what sales value (at split-off) would Forest Products be indifferent between selling them at split-off and processing them further? c. At what sales value (at split-off) would Forest Products be indifferent between selling them at split-off and processing them further in case the disposal cost for FP-40 increases to $150,000 for every 55,000 units of FP-40 produced? Exercise 11-52 (Static) Physical Quantities Method; Sell or Process Further (LO 11-3, 4) Forest Products, Incorporated, manufactures three products (FP-10, FP-20, and FP-40) from a single, joint input. None of the products can be sold without further processing. In November, joint product costs were $240,000. Additional information follows: The sale of FP- 40 has been banned by a recent law. If FP-40 is produced, disposal in an approved manner costs $120,000 for every 55,000 units produced. Required: a. Assuming that Forest Products continues to use the physical quantities method of allocation and to manufacture and sell FP.10 and FP-20. What joint costs would be allocated to FP-10 and FP-20? b. There is a possibility that a market for FP-10 and FP-20 at split-off will develop. In other words, it will be possible to sell the two products rather than process them further. At what sales value (at split-off) would Forest Products be indifferent between selling them at split-off and processing them further? c. At what sales value (at split-off) would Forest Products be indifferent between selling them at split-off and processing them further, in case the disposal cost for FP-40 increases to $150,000 for every 55,000 units of FP.40 produced

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts