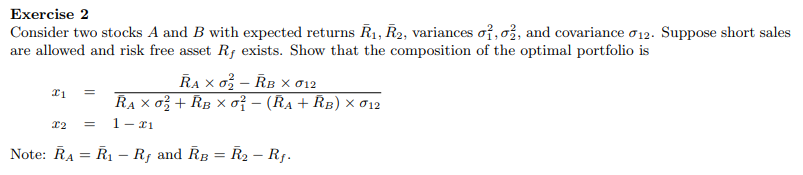

Question: Exercise 2 Consider two stocks A and B with expected returns Ri R2 variances ? ? and covariance ?12-Suppose short sales are allowed and risk

Exercise 2 Consider two stocks A and B with expected returns Ri R2 variances ? ? and covariance ?12-Suppose short sales are allowed and risk free asset Ry exists. Show that the composition of the optimal portfolio is C1- Note: Ra=R,-R, and RB=R2-Ry

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock