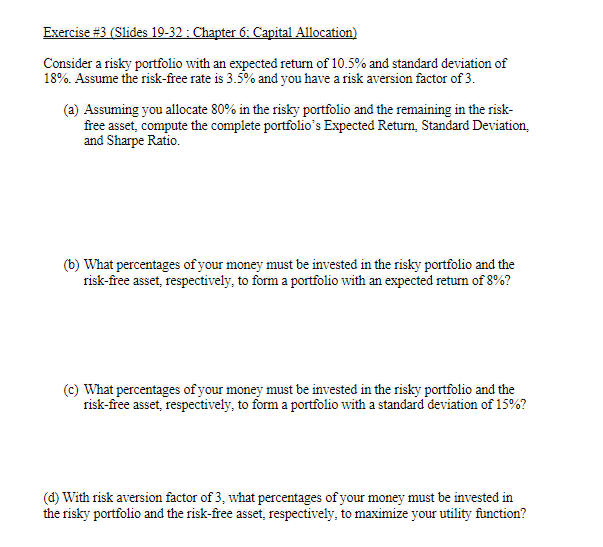

Question: Exercise # 3 ( Slides 1 9 - 3 2 : Chapter 6 : Capital Allocation ) Consider a risky portfolio with an expected

Exercise #Slides : Chapter : Capital Allocation

Consider a risky portfolio with an expected return of and standard deviation of Assume the riskfree rate is and you have a risk aversion factor of

a Assuming you allocate in the risky portfolio and the remaining in the riskfree asset, compute the complete portfolio's Expected Return, Standard Deviation, and Sharpe Ratio.

b What percentages of your money must be invested in the risky portfolio and the riskfree asset, respectively, to form a portfolio with an expected return of

c What percentages of your money must be invested in the risky portfolio and the riskfree asset, respectively, to form a portfolio with a standard deviation of

d With risk aversion factor of what percentages of your money must be invested in the risky portfolio and the riskfree asset, respectively, to maximize your utility function?

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock