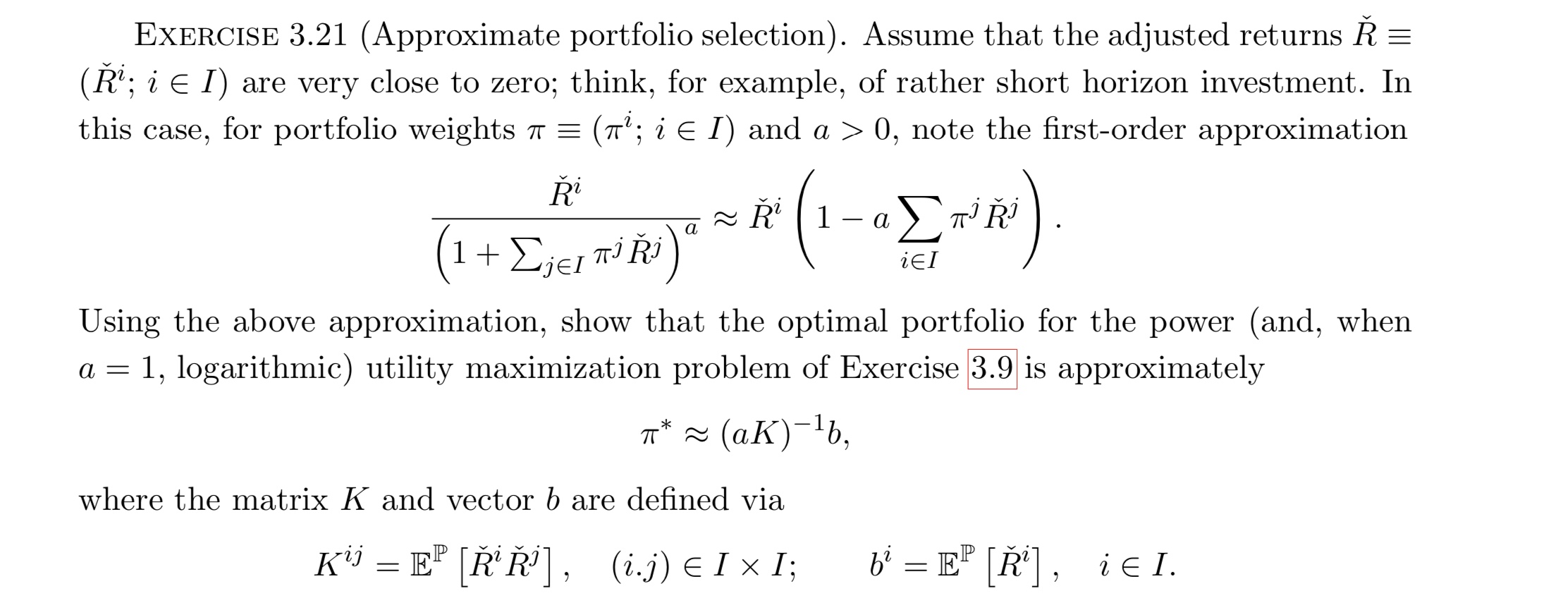

Question: EXERCISE 3.21 (Approximate portfolio selection). Assume that the adjusted returns R = (R'; i E I) are very close to zero; think, for example, of

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock